OK so someone DM'd me this question: 'Alex, I just bought a brand new Tesla Model Y and I'm shopping for insurance - what are the most common mistakes people make when it comes to gap insurance for electric cars?' Well, let me tell you, I've seen some crazy stuff in my 5 years of dealing with EV insurance. People end up paying thousands of dollars more than they need to, simply because they don't understand how gap insurance works. Sound familiar?

OK So Here's the Deal With Gap Insurance

Gap insurance for electric cars is a must-have, especially if you're financing or leasing your vehicle. It covers the difference between the actual cash value of your car and the amount you still owe on your loan or lease. For example, let's say you buy a BMW iX for $80,000 and it gets totaled in an accident. If the insurance company says the car is only worth $60,000, but you still owe $70,000 on your loan, gap insurance will cover that extra $10,000. That's a big deal, right? I mean, who wants to be stuck paying off a loan for a car that's no longer drivable?

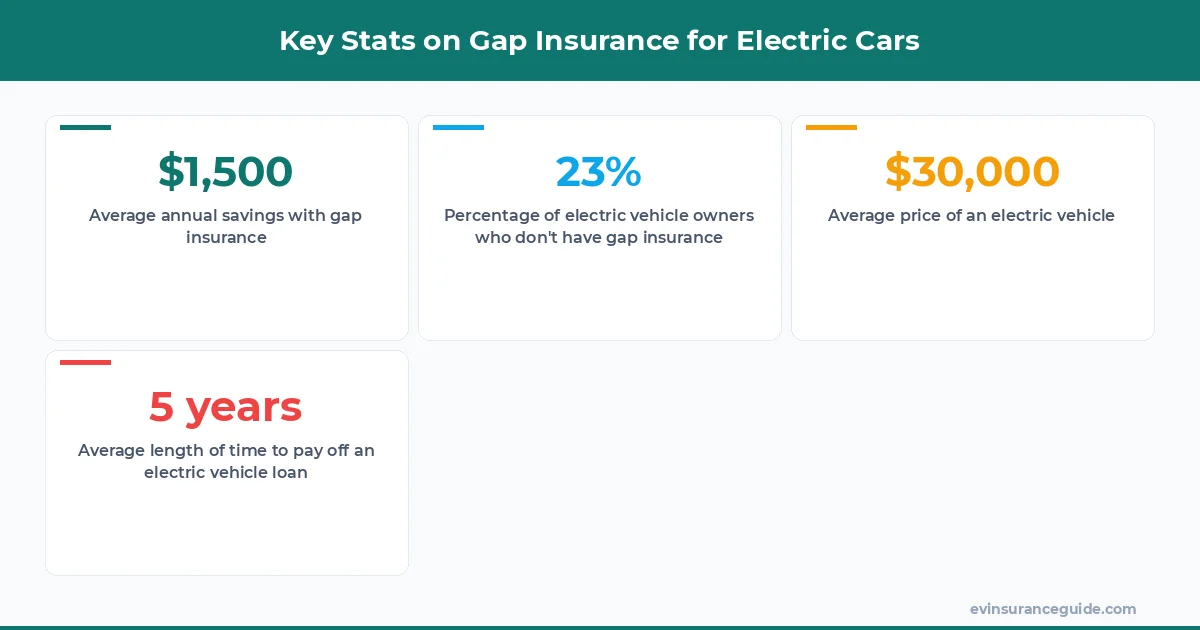

But, and this is a big but, a lot of people don't realize that gap insurance is not always included in their standard insurance policy. You gotta ask for it, and sometimes it's an extra cost. Now, I know what you're thinking - 'How much is this gonna set me back?' Well, the cost of gap insurance can vary depending on the insurance company and the state you live in, but on average, it's around $20-$30 per year. Not bad, considering it could save you thousands in the long run.

And, let me tell you, I've seen some insurance companies try to sneak in extra fees for gap insurance. Like, I had a client who was quoted $500 per year for gap insurance by a certain company (won't name names, but it starts with an 'S' and ends with an 'urance'). I mean, that's just ridiculous. We ended up finding a better deal with another company for $25 per year. That's a $475 difference, folks!

Beware of the Fine Print: Hidden Costs in Gap Insurance Policies

Now, I'm gonna warn you about something - some insurance companies have hidden costs and exclusions in their gap insurance policies that can leave you hanging when you need it most. For example, some policies might not cover certain types of accidents, like floods or wildfires. Or, they might have a deductible that's way higher than you expected. Know what the kicker is? These exclusions are often buried deep in the fine print, so you gotta really read the policy carefully to catch them. Don't be like me, I once missed a deductible clause that ended up costing me $1,000 out of pocket. That one stung.

So, how do you avoid these hidden costs? Well, first of all, make sure you read the policy carefully before signing. And, don't be afraid to ask questions - if something doesn't make sense, ask the insurance company to explain it to you. I mean, it's your money on the line, right? Also, shop around and compare policies from different companies. Some companies, like GEICO, offer more comprehensive gap insurance policies with fewer exclusions.

And, let's talk about the Rivian R1T for a second. I mean, that's a beautiful truck, but it's also a pricey one. If you're financing or leasing an R1T, you're gonna want to make sure you have gap insurance that covers its full value. I've seen some insurance companies try to lowball the value of electric vehicles, so make sure you get an insurance company that understands the true value of your EV.

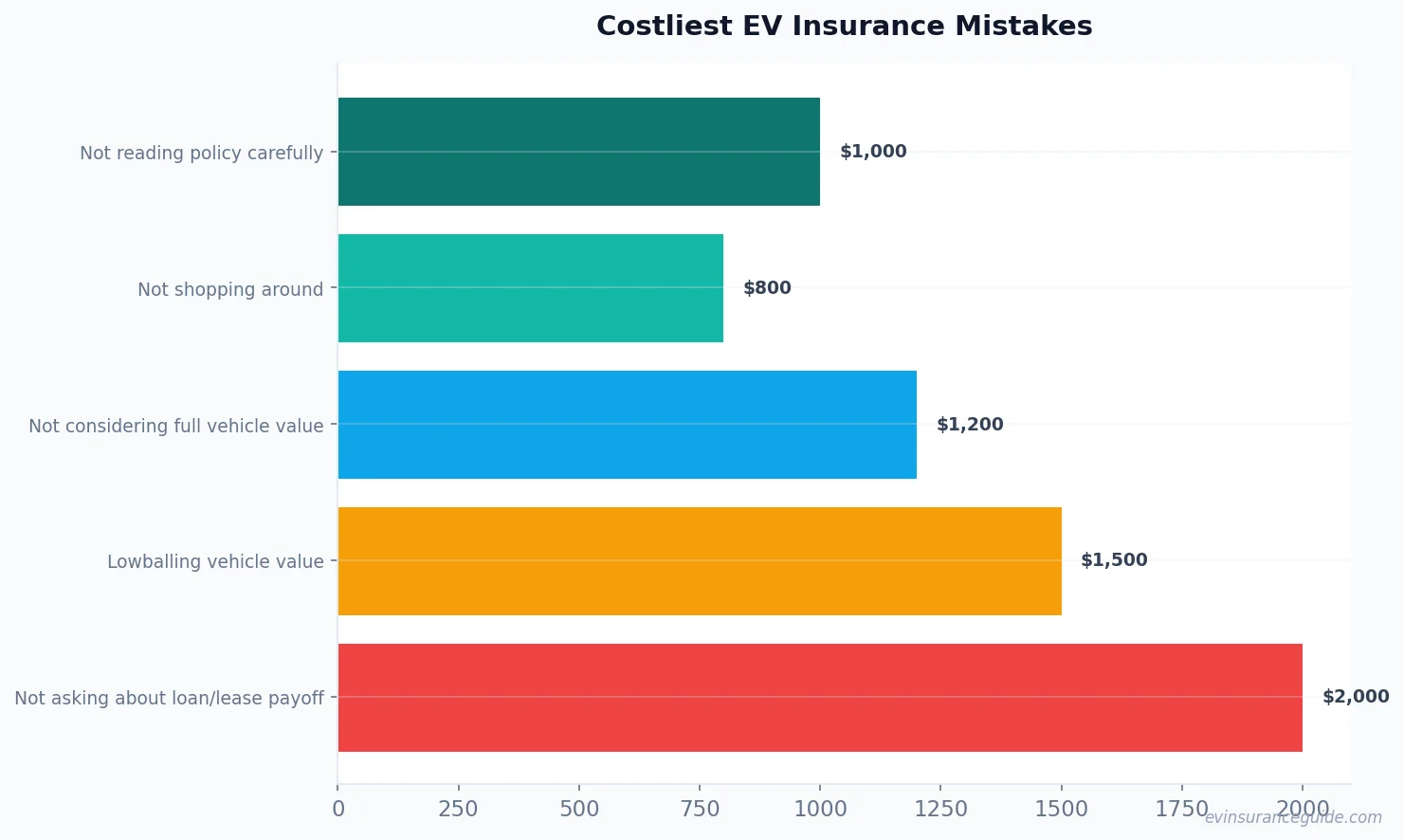

3 Common Mistakes People Make When Buying Gap Insurance for Electric Cars

So, here are 3 common mistakes people make when buying gap insurance for electric cars:

- 1. Not reading the policy carefully - like I said, those exclusions and hidden costs can be sneaky.

- 2. Not shopping around - you might be able to find a better deal with another company.

- 3. Not considering the full value of your vehicle - if you have a luxury EV like a Tesla Model S, you're gonna want to make sure your gap insurance policy covers its full value.

And, let me tell you, I've seen people make some crazy mistakes when it comes to gap insurance. Like, I had a client who bought a Hyundai Ioniq 5 without realizing that the insurance company was only covering 80% of its value. I mean, that's a $10,000 difference, folks!

Pro tip: Always ask about the 'loan/lease payoff' option when buying gap insurance. This ensures that your insurance company will pay off the full amount of your loan or lease, even if the actual cash value of your car is lower.

Busting the Myth: Gap Insurance is Only for Luxury Electric Vehicles

Now, I know some people think that gap insurance is only necessary for luxury electric vehicles, like the Tesla Model S or the BMW iX. But, that's just not true. Gap insurance is essential for any electric vehicle, regardless of its price tag. I mean, think about it - if you're financing or leasing a vehicle, you're still at risk of owing more on your loan or lease than the vehicle is worth. And, that's where gap insurance comes in.

For example, let's say you buy a Nissan Leaf for $30,000 and it gets totaled in an accident. If the insurance company says the car is only worth $20,000, but you still owe $25,000 on your loan, gap insurance will cover that extra $5,000. That's a big deal, right? I mean, who wants to be stuck paying off a loan for a car that's no longer drivable?

And, let's talk about the cost of gap insurance for electric cars. I mean, it's not as expensive as you might think. On average, gap insurance costs around $20-$30 per year, depending on the insurance company and the state you live in. That's a small price to pay for the peace of mind that comes with knowing you're protected in case something happens to your vehicle.

Comparing Gap Insurance Policies: How to Get the Best Deal

So, how do you get the best deal on gap insurance for your electric vehicle? Well, first of all, you gotta shop around. Compare policies from different companies, like GEICO, State Farm, and Allstate. And, don't be afraid to negotiate - if you find a better deal with another company, ask your current insurance company to match it. I mean, it's your money on the line, right?

For example, let's say you're financing a Rivian R1T and you need gap insurance to cover its full value. You might find that one company offers a better deal than another, simply because they understand the true value of your EV. So, don't be afraid to shop around and compare policies.

And, let's talk about the Hyundai Ioniq 5 for a second. I mean, that's a great car, but it's also a pricey one. If you're financing or leasing an Ioniq 5, you're gonna want to make sure you have gap insurance that covers its full value. I've seen some insurance companies try to lowball the value of electric vehicles, so make sure you get an insurance company that understands the true value of your EV.

FAQs

#### What is gap insurance for electric cars?

Gap insurance for electric cars is a type of insurance that covers the difference between the actual cash value of your vehicle and the amount you still owe on your loan or lease. It's essential for anyone who is financing or leasing an electric vehicle.

#### How much does gap insurance cost?

The cost of gap insurance can vary depending on the insurance company and the state you live in, but on average, it's around $20-$30 per year.

#### Do I need gap insurance if I'm buying an electric vehicle outright?

No, you don't need gap insurance if you're buying an electric vehicle outright. But, if you're financing or leasing, it's a good idea to get gap insurance to protect yourself in case something happens to your vehicle.

#### Can I get gap insurance from my car dealer?

Yes, you can get gap insurance from your car dealer, but it's often more expensive than buying it from an insurance company. So, make sure you shop around and compare prices before making a decision.

#### How do I know if I have gap insurance?

You can check your insurance policy to see if you have gap insurance. If you're not sure, you can always contact your insurance company to ask.

#### What's the difference between gap insurance and comprehensive insurance?

Gap insurance covers the difference between the actual cash value of your vehicle and the amount you still owe on your loan or lease, while comprehensive insurance covers damage to your vehicle that's not related to an accident, like theft or vandalism.

Go get yourself a better quote. You deserve it.

— Alex