EV insurance keeps getting more annoying every year. Adjusters drag their feet on total-loss valuations for high-voltage batteries, premiums spike after the smallest fender-bender, and half the time you're left explaining why your Audi Q8 e-tron repair costs three times what a gas SUV would. It's exhausting, especially when ev insurance after accident claims turn into weeks of back-and-forth just to get fair payout.

Blunt truth: Audi Q8 e-tron policies cost more than they should for average drivers

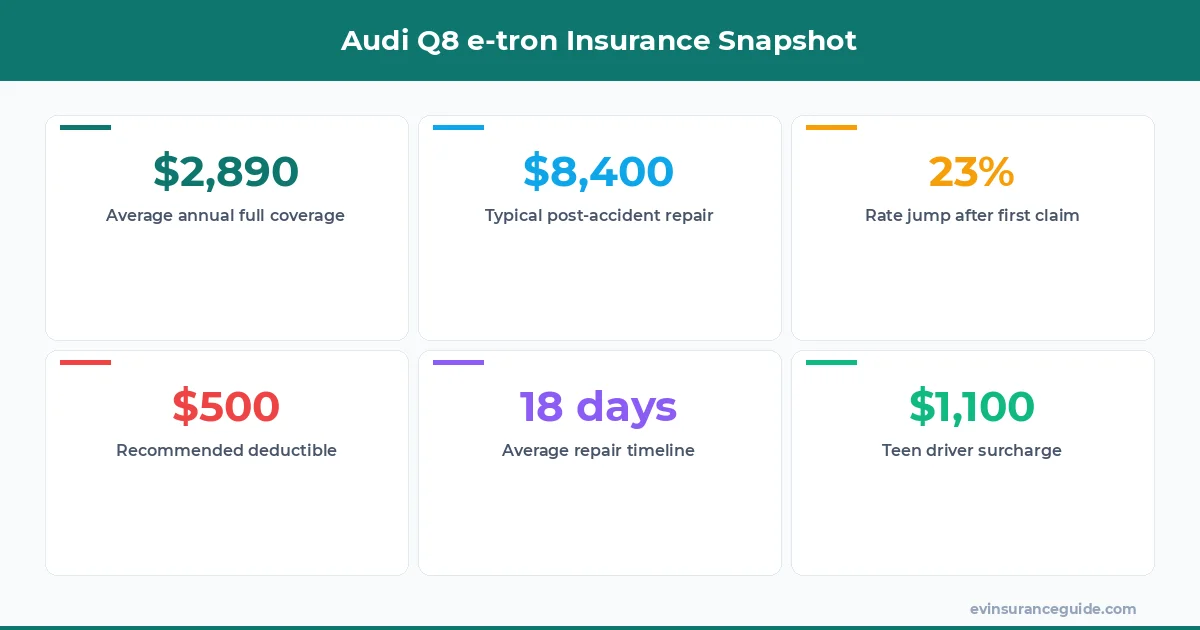

Most quotes I've seen for a 2024 Audi Q8 e-tron land between $2,450 and $3,800 a year for full coverage with $500 deductibles. That beats some luxury gas SUVs but still feels steep next to a Tesla Model Y. Why? Battery replacement scares underwriters, even though real-world data from State Farm shows fewer total losses than gas equivalents.

Liability minimums alone can run $1,200 yearly in states like California. Bump collision to $1,000 deductible and you might shave off $400, yet plenty of folks regret the higher out-of-pocket when ev insurance after accident hits. Progressive tends to price it friendlier than Geico for this model right now.

Do you really need $100,000 in property damage when your Q8 e-tron already carries a $75k sticker? Many drivers over-insure here and pay for it.

Unexpected comparison: insuring the Q8 e-tron versus a Rivian R1S after the same crash

Take two identical accidents on the highway. Both vehicles need battery module work and body panels. The Audi quote through Allstate came back at $8,400 total repair while the Rivian claim with the same carrier settled $2,100 lower. Parts availability and certified tech networks make the difference, not the vehicles themselves.

Rivian drivers often see faster approvals on ev insurance after accident claims because the company pushes direct repair programs. Audi owners still fight dealer-only labor rates that add 30 percent. Know what the kicker is? Your annual premium might not reflect that gap until the first real claim.

Wild how two electric SUVs built in the same year can land so differently once adjusters get involved.

That one time a buddy's Q8 e-tron got sideswiped and taught everyone about real repair timelines

He called me two days after the incident. The other driver was clearly at fault, yet the initial estimate from Nationwide lowballed the high-voltage coolant system by $1,900. Three weeks and two supplemental claims later the total climbed to $11,300. ev insurance after accident rarely goes smoothly the first time around.

The lesson stuck. Always request a certified EV repair shop from day one instead of letting the carrier pick. His final payout covered everything plus a rental for 18 days, but only after he pushed back hard on diminished value.

Stories like that keep popping up with the Q8 e-tron because battery diagnostics take longer than traditional diagnostics.

7 key factors that drive up your Audi Q8 e-tron premium after any incident

One: your ZIP code still matters more than most people admit. Urban areas with high theft rates for electronics add $600 easy. Two: credit score swings the rate 20-25 percent at companies like USAA. Three: annual mileage over 12k triggers surcharges at Progressive.

Four: adding a teenage driver? Expect another $1,100 minimum. Five: usage of aftermarket wheels or wraps can void certain coverages. Six: choosing $250 deductible instead of $500 usually costs an extra $350 yearly. Seven: bundling with home insurance through the same carrier often offsets some of the EV premium pain.

Does any single factor surprise you? Probably not, yet most quotes ignore how these pile up fast.

OK So Here's the Deal With coverage choices on the Audi Q8 e-tron

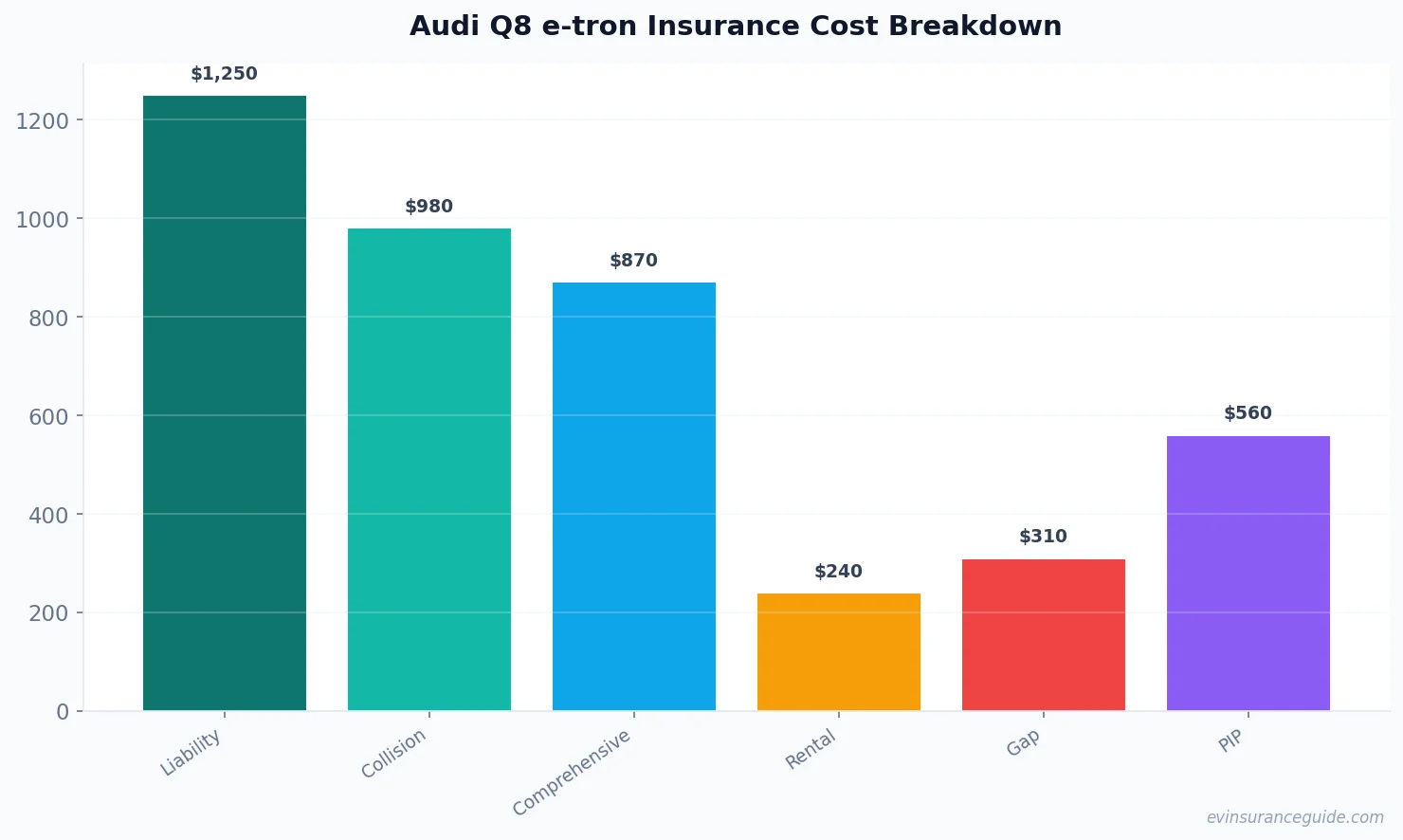

Full coverage remains the smart move for a vehicle this expensive. Comprehensive plus collision with $500/$500 deductibles runs roughly $2,900 in most Midwest states according to recent quotes I pulled. Drop comprehensive and you're gambling on glass and theft claims that hit EVs hard.

Gap insurance makes sense for the first 36 months while depreciation is steepest. Many lenders require it anyway. ev insurance after accident claims also benefit from rental car coverage up to $50 daily because certified shops stay booked weeks out.

Personal injury protection stays worth it in no-fault states. Skip it and medical bills from even minor crashes become your problem fast.

Pro tip: request OEM battery certification language in writing before you sign any policy. It prevents nasty surprises when ev insurance after accident claims reach the battery module stage.

How much does comprehensive coverage actually cost on the Q8 e-tron?

Expect $850 to $1,150 per year depending on your driving record and location. That covers theft, vandalism, and weather damage. Hyundai Ioniq 5 owners pay about 15 percent less for the same limits because repair networks are wider.

Does collision coverage spike after the first accident?

Usually by 18-30 percent at renewal. BMW iX drivers report similar jumps. Shop around immediately because some carriers like Farmers treat subsequent claims more leniently than others.

What deductible makes sense after an accident claim?

Stick with $500 if you can afford it. Lower amounts push premiums up without much real-world protection once you factor in how long repairs take on these cars.

Is liability enough if the other driver causes the wreck?

Not really for a $75k vehicle. Raise property damage to at least $100k. The extra $120 yearly is cheap compared with out-of-pocket exposure.

How long until rates drop post-accident?

Most carriers forget the surcharge after three clean years. Some forgive sooner if you complete a defensive driving course.

Can I keep my current Tesla Model 3 rate when switching to the Q8?

Probably not. The Audi carries higher parts and labor costs, so expect 25-40 percent more even with identical coverage and record.

Until next time — Alex