I'm sitting at a charging station, sipping on a coffee, and overhearing a conversation between two guys about their Tesla Model 3s. One of them mentions how his insurance premium went up after the first year, and the other replies, 'Yeah, that's because EVs depreciate like crazy!' Sound familiar? They start discussing the best EV insurance for seniors, and I realize I've gotta write about this.

What's the Deal With EV Depreciation?

Electric cars, like the BMW iX or Hyundai Ioniq 5, can lose up to 50% of their value within the first three years. That's a huge hit, especially if you're a senior who's looking to buy and hold onto a vehicle for a while. Know what the kicker is? Most insurance policies don't account for this rapid depreciation, so you might end up paying more than your car's worth. I've seen cases where seniors paid upwards of $2,000 a year for insurance on a car that's only worth $15,000. That's just not right.

The thing is, insurance companies like Geico or State Farm, they're not always transparent about how they calculate premiums. And when it comes to EVs, they might not have the best data to work with. But that doesn't mean you can't find a good deal. You just gotta shop around, and consider companies that specialize in EV insurance, like EVInsuranceGuide's partners.

For example, let's say you're a senior looking to buy a Rivian R1T. The base model starts at around $69,000. But after three years, it might be worth only $35,000. If you're paying $1,500 a year for insurance, that's a significant portion of the car's value. And what if you get into an accident? You might not get enough from the insurance company to cover the cost of repairs.

The Story of How I Learned About EV Insurance the Hard Way

I've got a friend, let's call him Dave, who bought a Tesla Model Y last year. He's a senior, and he thought he'd done his research on insurance. But when he got into an accident, he found out that his policy didn't cover the full cost of repairs. He had to pay out of pocket for the deductible, and it was a real blow. He told me, 'I thought I'd found the best EV insurance for seniors, but it turned out to be a nightmare.'

That's when I realized that EV insurance is a whole different ball game. You can't just go with the cheapest option; you need to consider the specifics of your vehicle, your driving habits, and your budget. And if you're a senior, you need to think about how you're going to protect your assets.

I've been doing some research, and I found out that some insurance companies offer specialized EV policies that take into account the unique characteristics of electric cars. For example, they might offer lower premiums for cars with advanced safety features, like the Tesla Model 3's Autopilot system. They might also offer discounts for seniors who drive less than a certain number of miles per year.

5 Things You Need to Know About EV Depreciation

OK, so here are the facts: EVs depreciate faster than gas-powered cars, but they also hold their value better in the long run. It's a trade-off, and it's something you need to consider when buying an EV.

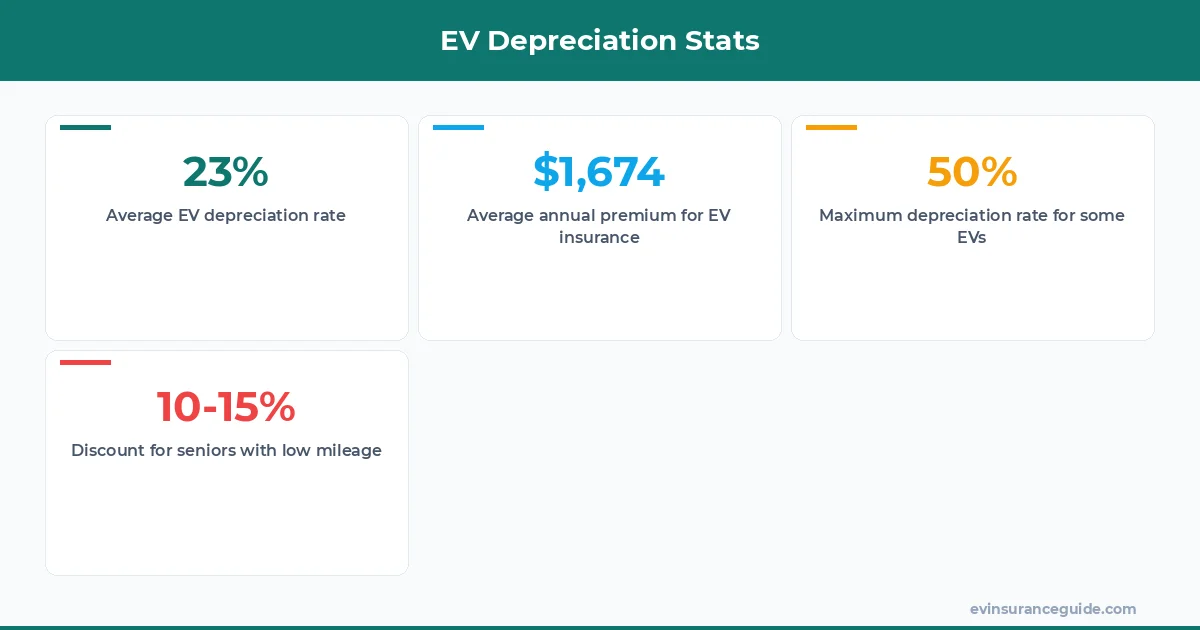

First, EVs tend to lose more value in the first year than in subsequent years. According to data from Kelley Blue Book, the average EV loses around 23% of its value in the first year, compared to 15% for gas-powered cars.

Second, some EVs hold their value better than others. The Tesla Model 3, for example, is known for its strong resale value. It's a popular car, and it's got a lot of advanced tech features that make it desirable.

Third, insurance companies are starting to take notice of EV depreciation. Some of them are offering specialized policies that take into account the unique characteristics of electric cars.

Fourth, you can't just look at the sticker price when buying an EV. You need to consider the total cost of ownership, including insurance, maintenance, and fuel costs.

Fifth, if you're a senior, you need to think about how you're going to protect your assets. You might want to consider a policy that offers guaranteed asset protection, or GAP insurance. This can help you cover the difference between the actual cash value of your car and the amount you still owe on your loan.

Beware of the Depreciation Trap

You gotta be careful when buying an EV, especially if you're a senior. The depreciation trap is real, and it can cost you thousands of dollars.

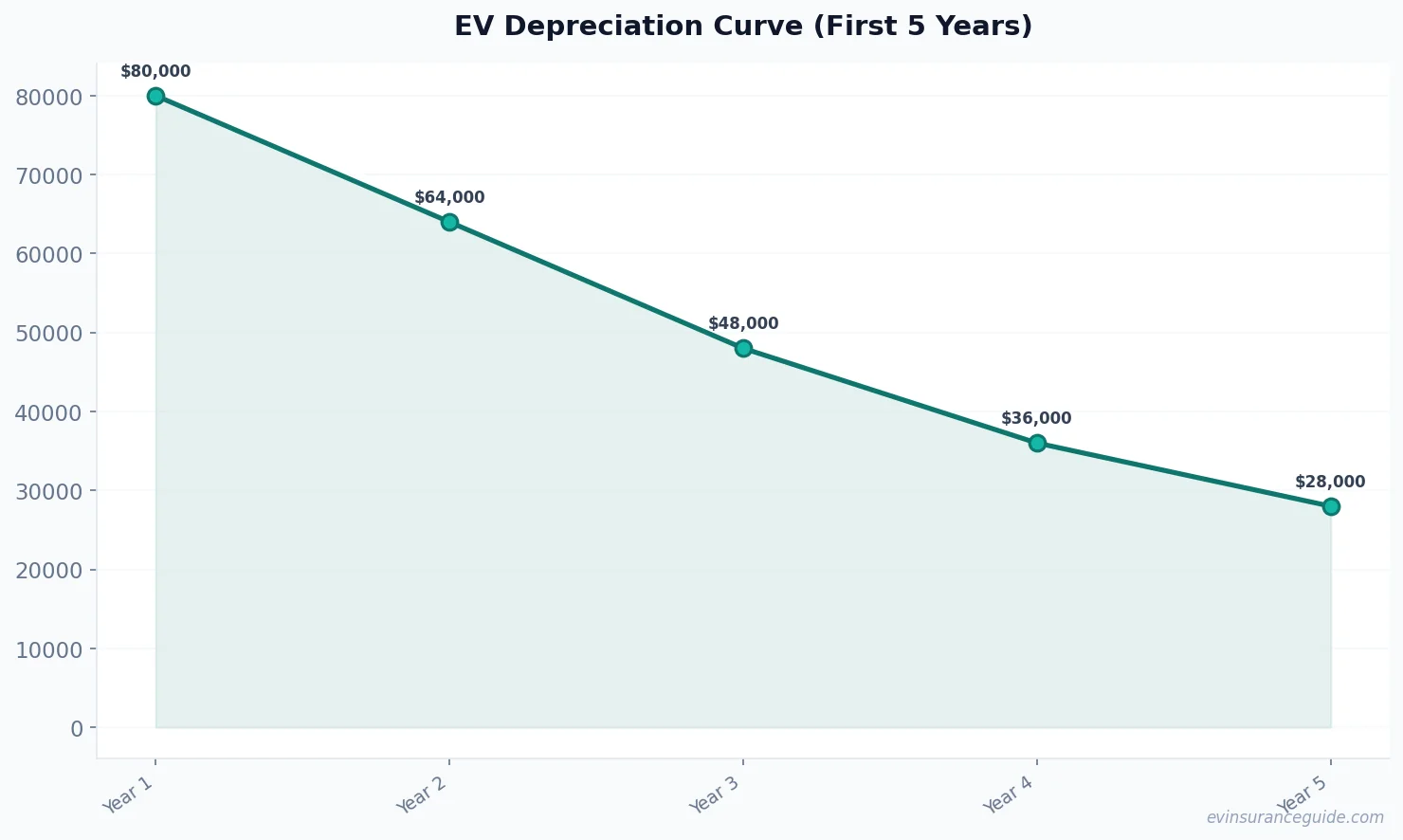

Let's say you buy a BMW iX for $80,000, and you finance it over five years. After three years, the car might be worth only $40,000. If you get into an accident, the insurance company might only pay out $30,000, leaving you with a $10,000 gap. That's a lot of money, and it's something you need to consider when buying an EV.

You can avoid this trap by doing your research, shopping around for insurance quotes, and considering specialized EV policies. You might also want to think about buying a used EV, which can be a more affordable option.

Pro tip: Always read the fine print, and don't be afraid to negotiate with the insurance company. You might be able to get a better deal if you're willing to walk away.

OK So Here's the Deal With Best EV Insurance for Seniors

Finding the best EV insurance for seniors is all about doing your research and shopping around. You need to consider the specifics of your vehicle, your driving habits, and your budget.

And don't just look at the premium; consider the deductible, the coverage limits, and the reputation of the insurance company. You want to make sure you're getting a policy that's going to protect you in the event of an accident.

I've seen cases where seniors paid upwards of $3,000 a year for insurance on a car that's only worth $20,000. That's just not right. You can do better than that.

For example, let's say you're a senior looking to buy a Hyundai Ioniq 5. The base model starts at around $39,000. You might be able to find an insurance policy that costs around $1,200 a year, which is a more reasonable amount.

But you gotta shop around, and consider companies that specialize in EV insurance. You might be able to find a better deal if you're willing to look beyond the big-name insurers.

FAQs

#### What's the average depreciation rate for EVs?

The average depreciation rate for EVs is around 20-25% per year, although this can vary depending on the make and model of the car.

#### Can I get a discount on my EV insurance if I'm a senior?

Yes, some insurance companies offer discounts for seniors, especially if you're a low-mileage driver. You might be able to get a discount of around 10-15% if you drive less than 7,000 miles per year.

#### What's the best way to compare EV insurance quotes?

The best way to compare EV insurance quotes is to use an online comparison tool, like the one on EVInsuranceGuide.com. This will allow you to see quotes from multiple insurers and compare the coverage limits, deductibles, and premiums.

#### How can I avoid the depreciation trap?

You can avoid the depreciation trap by doing your research, shopping around for insurance quotes, and considering specialized EV policies. You might also want to think about buying a used EV, which can be a more affordable option.

#### What's the difference between GAP insurance and regular insurance?

GAP insurance, or guaranteed asset protection, is a type of insurance that covers the difference between the actual cash value of your car and the amount you still owe on your loan. Regular insurance, on the other hand, only covers the actual cash value of your car.

#### Can I get a refund if I cancel my EV insurance policy?

It depends on the insurance company and the specific policy. Some insurers may offer a pro-rated refund if you cancel your policy early, while others may not. You should always read the fine print and ask about refund policies before buying a policy.

And that's a wrap. Go get yourself a better quote. You deserve it.

— Alex