Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. He'd just turned 65, and his insurer said it was due to his 'new' risk profile. Sound familiar? Yeah, I've seen this before — insurers love to hike premiums on seniors, citing 'higher risk'... but what about the role of telematics data in all this? That's what we're gonna explore.

Comparing Apples and Oranges: Traditional Insurance vs Telematics-Based

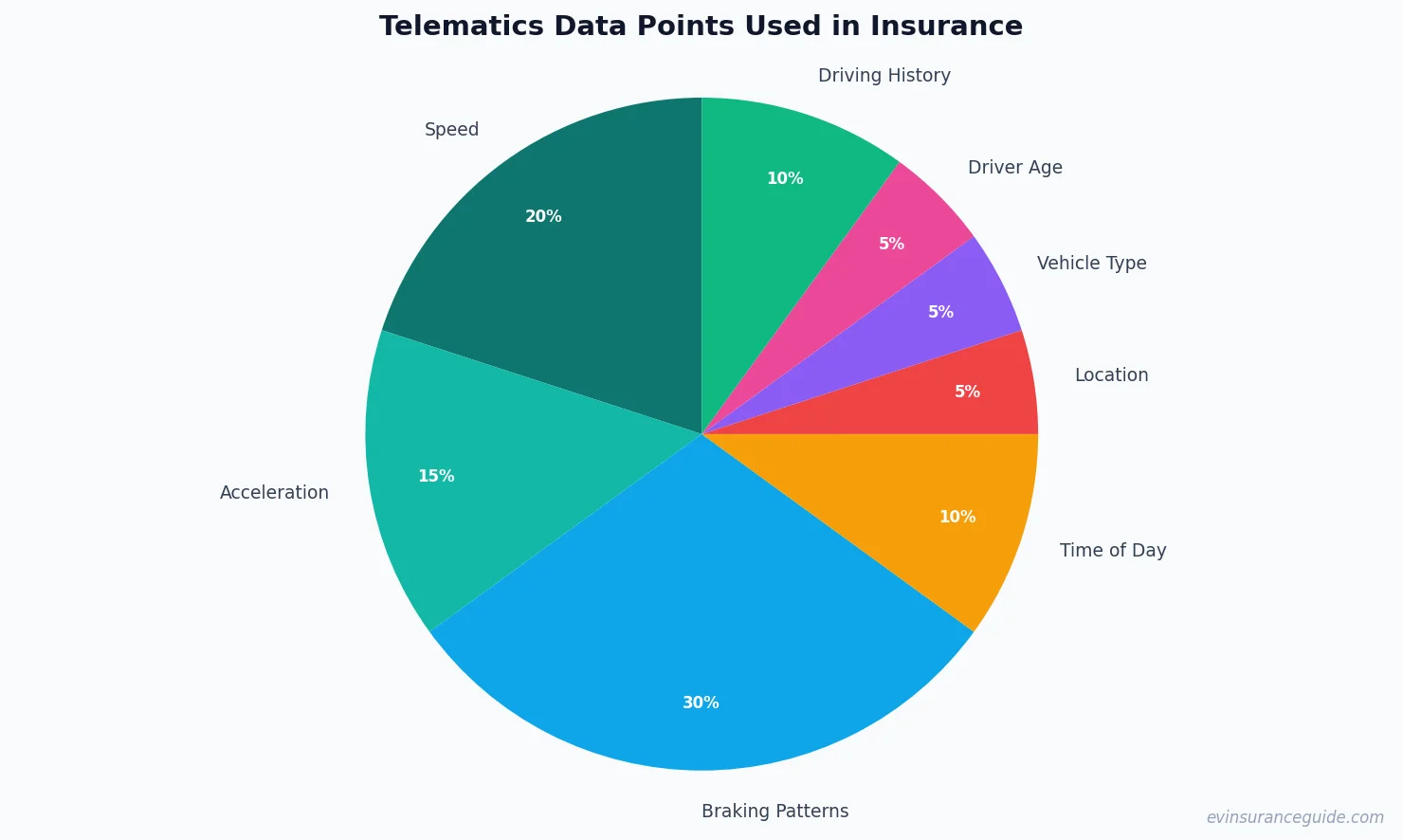

Traditional insurance pricing is kinda like throwing darts blindfolded — you might hit the target, but it's mostly luck. Insurers use broad demographics like age, location, and driving history to estimate your risk. But telematics data is like having a GPS tracker on your EV — it shows exactly how you drive, where you drive, and when. For instance, a Tesla Model 3 owner who drives 10,000 miles per year will likely pay less than a similar driver who only drives 5,000 miles, due to the lower risk of accidents. Know what the kicker is? This data can actually help seniors like Marcus get better rates, if they're willing to share it.

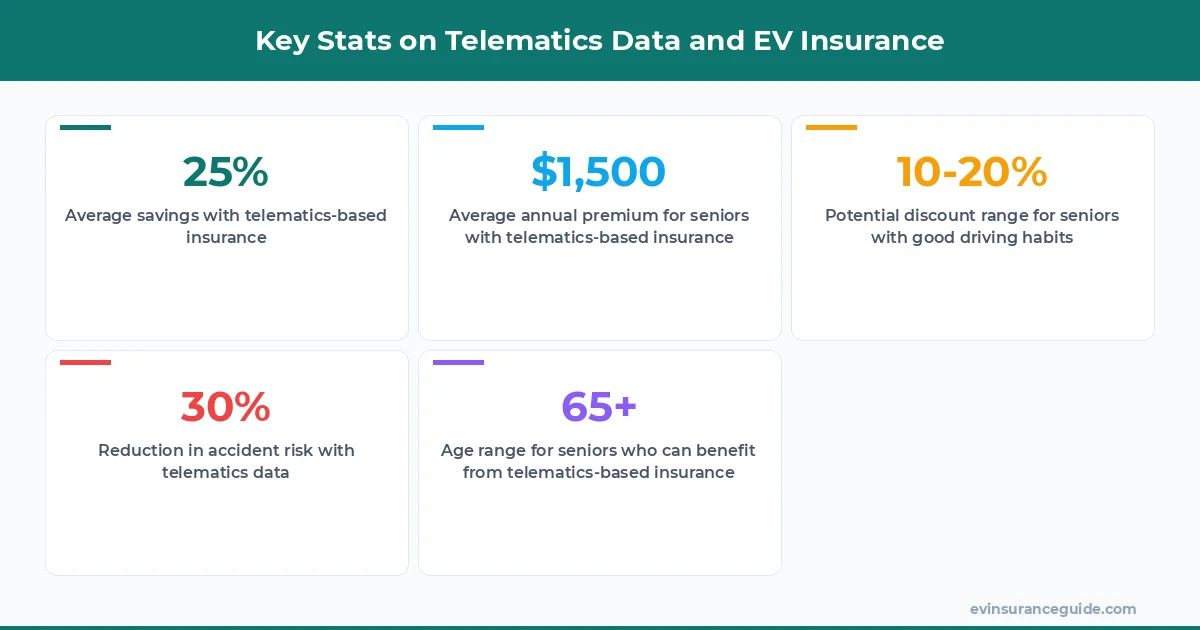

Take the Hyundai Ioniq 5, for example. Its built-in telematics system can track everything from acceleration to braking patterns. If you're a safe driver, this data can be used to lower your premiums. In fact, some insurers offer discounts of up to 20% for drivers who opt-in to telematics tracking. That's a significant savings, especially for seniors who might be on a fixed income.

But, here's the thing: not all telematics systems are created equal. Some, like the one in the BMW iX, are more advanced and can provide real-time feedback to drivers. Others, like those in older EV models, might be more basic. So, when shopping for the best EV insurance for seniors, it's crucial to consider the type of telematics system in your vehicle.

Can You Really Trust Telematics Data to Determine Your Insurance Rate?

Can you really trust an algorithm to accurately assess your driving skills? I mean, we've all seen those viral videos of Tesla Autopilot going rogue... what if your telematics data gets misinterpreted? That one stung, right? Well, actually, most insurers use a combination of human review and machine learning to evaluate telematics data. It's not just about the numbers; they also consider context, like road conditions and weather.

For instance, a study by the National Highway Traffic Safety Administration found that telematics data can reduce the risk of accidents by up to 30%. That's a significant statistic, especially for seniors who might be more vulnerable to injuries. And, with the rise of EVs like the Rivian, which comes with advanced safety features like automatic emergency braking, the potential for telematics data to impact insurance rates is huge.

But, there's still a lot of uncertainty surrounding telematics data and its impact on insurance pricing. As a senior, you might be wondering: will my rates go up or down if I opt-in to telematics tracking? The answer is, it depends. If you're a safe driver, you'll likely see savings. But, if you're a more aggressive driver, your rates might increase.

Pro tip: When shopping for the best EV insurance for seniors, look for insurers that offer telematics-based discounts and have a clear, transparent evaluation process. Don't be afraid to ask questions about how they use your data.

Warning: Don't Fall for the 'Discount' Trap — Read the Fine Print

We've all seen those ads promising 'up to 30% off' your insurance premiums, but what's the catch? Often, it's a limited-time offer or only applies to certain drivers. Don't fall for the hype; make sure you understand the terms and conditions. For example, some insurers might offer a discount for telematics tracking, but only if you meet certain criteria, like driving less than 7,500 miles per year.

And, let's not forget about the potential drawbacks of telematics data. For instance, if you live in an area with high crime rates, your telematics data might show a higher risk of theft or vandalism. This could lead to higher premiums, even if you're a safe driver. So, it's crucial to weigh the pros and cons before opting-in to telematics tracking.

As a senior, you might also be concerned about the cost of telematics-based insurance. But, the truth is, it can be more affordable than traditional insurance. For instance, a senior driving a Tesla Model 3 might pay around $1,200 per year for telematics-based insurance, compared to $1,800 per year for traditional insurance.

Myth-Busting: Telematics Data Won't Invade Your Privacy

I've heard some wild claims about telematics data being used to track your every move... but that's just not true. Insurers are bound by strict data protection laws, and they only use telematics data for the purpose of evaluating your insurance risk. Dead serious, your privacy is protected.

In fact, most insurers use anonymized data, which means they don't even know it's you behind the wheel. And, if you're concerned about data sharing, you can always opt-out of telematics tracking or choose an insurer that doesn't use it. For example, some insurers offer a 'data-free' option, which means they won't collect any telematics data from your vehicle.

But, here's the thing: telematics data can actually help seniors like Marcus get better rates. By sharing their driving data, they can demonstrate their safe driving habits and potentially lower their premiums. So, it's not just about privacy; it's about using data to your advantage.

5 Key Takeaways for Seniors Shopping for the Best EV Insurance

When it comes to finding the best EV insurance for seniors, there are a few key things to keep in mind. First, consider the type of telematics system in your vehicle. Second, look for insurers that offer telematics-based discounts. Third, read the fine print and make sure you understand the terms and conditions. Fourth, weigh the pros and cons of telematics tracking. And fifth, don't be afraid to ask questions about how your data will be used.

For instance, a senior driving a Hyundai Ioniq 5 might want to consider an insurer like USAA, which offers a telematics-based discount program. Or, they might want to look at an insurer like GEICO, which offers a 'data-free' option. The key is to shop around and find the best policy for your needs and budget.

And, don't forget to consider the cost. The best EV insurance for seniors might not always be the cheapest option. But, with telematics data, you can potentially save hundreds of dollars per year. For example, a senior driving a Tesla Model 3 might pay around $1,500 per year for telematics-based insurance, compared to $2,000 per year for traditional insurance.

FAQs

#### What is telematics data, and how is it used in insurance?

Telematics data refers to the information collected by your vehicle's onboard computer, such as speed, acceleration, and braking patterns. Insurers use this data to evaluate your driving risk and determine your insurance premium. For example, a study by the Insurance Institute for Highway Safety found that telematics data can reduce the risk of accidents by up to 25%.

#### Can I opt-out of telematics tracking?

Yes, you can opt-out of telematics tracking, but you might miss out on potential discounts. Some insurers offer a 'data-free' option, which means they won't collect any telematics data from your vehicle. However, this might not always be the best option, as telematics data can actually help seniors like Marcus get better rates.

#### How much can I save with telematics-based insurance?

The amount you can save with telematics-based insurance varies depending on your driving habits, vehicle, and insurer. On average, seniors can save around 10-20% on their insurance premiums by opting-in to telematics tracking. For example, a senior driving a Rivian might pay around $1,800 per year for telematics-based insurance, compared to $2,200 per year for traditional insurance.

#### Is my telematics data secure?

Yes, your telematics data is secure. Insurers are bound by strict data protection laws, and they only use telematics data for the purpose of evaluating your insurance risk. In fact, most insurers use anonymized data, which means they don't even know it's you behind the wheel.

#### Can I switch to a different insurer if I'm not happy with my current rates?

Yes, you can switch to a different insurer if you're not happy with your current rates. In fact, shopping around and comparing rates from different insurers is one of the best ways to find the best EV insurance for seniors. For example, a senior driving a BMW iX might want to consider an insurer like Progressive, which offers a telematics-based discount program.

#### What are some tips for finding the best EV insurance for seniors?

Some tips for finding the best EV insurance for seniors include shopping around, considering the type of telematics system in your vehicle, and looking for insurers that offer telematics-based discounts. You should also read the fine print and make sure you understand the terms and conditions. And, don't be afraid to ask questions about how your data will be used.

#### Are there any specific insurers that offer the best EV insurance for seniors?

Some insurers that offer the best EV insurance for seniors include USAA, GEICO, and Progressive. These insurers offer a range of discounts and options, including telematics-based discounts and 'data-free' options. For example, a senior driving a Tesla Model 3 might want to consider USAA, which offers a telematics-based discount program.

The best policy is the one you actually understand. — Alex