Ugh, don't even get me started on the state of EV insurance right now. I mean, we've got companies like Geico and Progressive trying to offer 'competitive' rates, but really they're just slapping electric vehicles into the same old gas-guzzler categories. It's like they think a Tesla Model 3 is just a Toyota Corolla with a fancy battery. Nope. And then there are the so-called 'specialized' EV insurers that charge an arm and a leg for coverage. Sound familiar? You've probably seen those ads for 'green' insurance that promises to save you money, but when you actually try to sign up, the quote is way higher than you expected. That one stung.

COMPARISON: Electric Cars vs. Gas Guzzlers

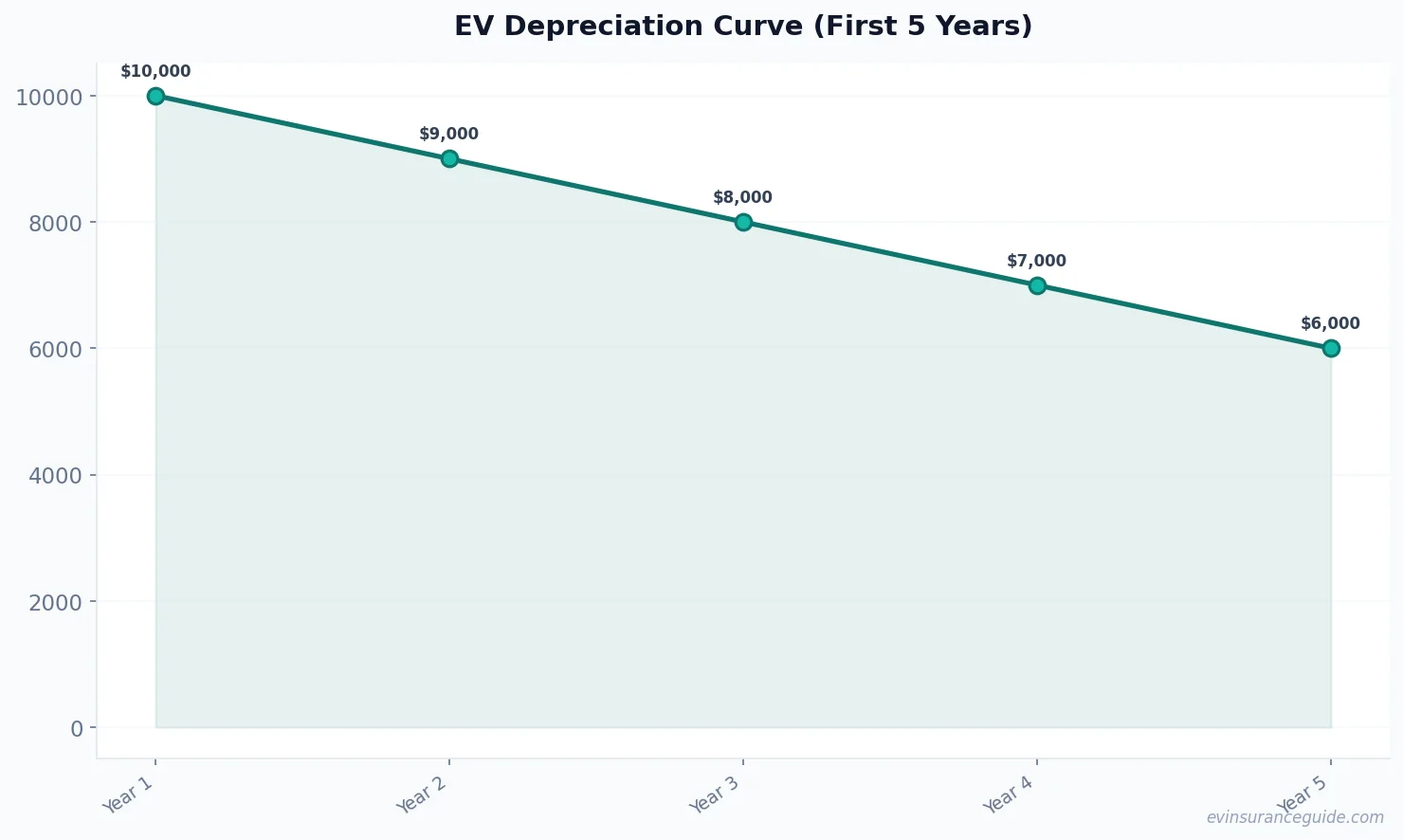

Let's compare the depreciation of electric cars to that of their gas-powered counterparts. We all know that cars lose value over time, but electric vehicles, like the BMW iX, tend to hold their value better than gas guzzlers. According to a study by Kelley Blue Book, the average gas-powered car loses around 50% of its value within the first three years. In contrast, electric cars like the Hyundai Ioniq 5 might only lose around 30-40% of their value in the same time frame. Know what the kicker is? This can actually work in your favor when it comes to insurance. If you're looking for the best EV insurance for seniors, you'll want to consider companies that take this slower depreciation into account. For example, some insurers offer specialty EV policies that factor in the unique characteristics of electric vehicles, like their lower maintenance costs and longer battery lifetimes. This can result in lower premiums for seniors who drive EVs.

But here's the thing: not all electric cars are created equal. The Tesla Model Y, for instance, is known for its high demand and relatively low depreciation rate. On the other hand, the Rivian R1T might lose more value due to its higher upfront cost and lower brand recognition. Wild, right? As a senior shopping for EV insurance, you'll want to research the specific depreciation curve for your vehicle to get the best rate. And don't even get me started on the importance of comparing quotes from multiple insurers. I mean, you wouldn't buy a car without test-driving a few options, would you?

MYTH_BUST: Electric Cars Don't Depreciate Faster

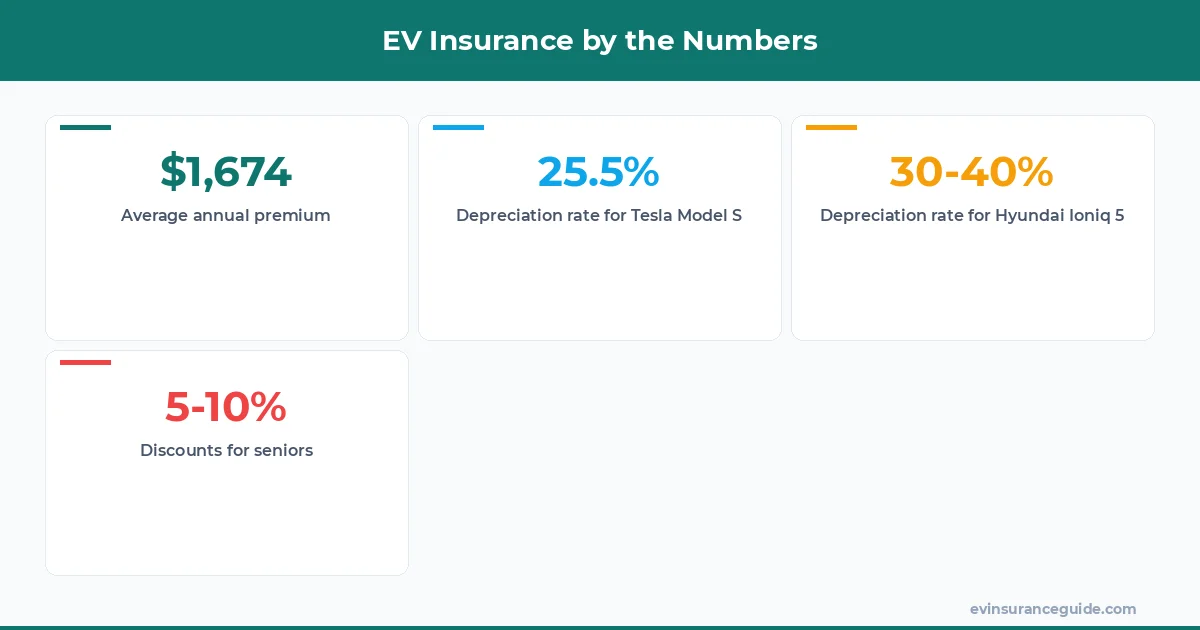

There's a common myth that electric cars depreciate faster than gas-powered vehicles. But is this really true? Let's look at some data. According to a study by iSeeCars, the top 5 electric cars with the lowest depreciation rates are all luxury models, including the Tesla Model S and the Audi e-tron. In fact, the Tesla Model S has a depreciation rate of just 25.5% over three years, which is lower than many gas-powered luxury cars. So, what does this mean for seniors looking for the best EV insurance for seniors? It means that if you're driving a luxury electric vehicle, you may be able to get a better insurance rate due to its slower depreciation.

Now, I know what you're thinking: what about the affordable EV options, like the Nissan Leaf or the Chevrolet Bolt? Don't they depreciate faster? Well, actually, the data suggests that these cars hold their value relatively well, too. The Nissan Leaf, for example, has a depreciation rate of around 35% over three years, which is comparable to many gas-powered compact cars. So, if you're a senior on a budget, you can still find an affordable EV that won't break the bank on insurance.

But, let's talk turkey. The cost of insurance for electric cars can vary widely depending on the company and the vehicle. For example, a senior driving a Tesla Model 3 might pay around $1,500 per year for insurance, while a senior driving a BMW iX might pay closer to $2,000 per year. And then there are the discounts. Some companies offer discounts for seniors who drive electric vehicles, which can range from 5-10% off the premium.

STORY_TEASE: My Friend's EV Insurance Nightmare

I've got a friend, let's call her Sarah, who recently bought a used Tesla Model Y. She was thrilled to get a great deal on the car, but when she went to insure it, she was shocked by the quote. The insurance company was charging her over $2,500 per year, which was way higher than she had expected. She ended up shopping around and finding a better rate with a different company, but not before she had to deal with a bunch of hassle and paperwork. And the worst part? The original insurer had tried to sell her a bunch of unnecessary add-ons, like roadside assistance and rental car coverage. Yeah, I know, another insurance article. But hear me out. This experience taught Sarah a valuable lesson: always, always, always compare quotes and read the fine print.

So, what can we learn from Sarah's experience? First, it's essential to shop around for insurance quotes, especially if you're a senior driving an electric vehicle. Don't just assume that your current insurer will give you the best rate. And second, be wary of add-ons and extra fees. While some of these might be useful, others might just be a waste of money. For example, if you already have roadside assistance through your vehicle's manufacturer or a separate service, you don't need to pay for it through your insurance company.

WARNING: Hidden Fees and Charges

When shopping for EV insurance, there are a few hidden fees and charges to watch out for. Some companies might charge extra for things like battery replacement or electric vehicle-specific repairs. Others might have higher deductibles or lower coverage limits for electric vehicles. And then there are the companies that will try to sell you unnecessary add-ons, like the ones I mentioned earlier. So, how can you avoid these traps? First, always read the fine print and ask questions if you're unsure about something. Second, look for companies that specialize in EV insurance and have experience with electric vehicles. These companies will often have more competitive rates and better coverage options.

For example, some companies offer a 'battery warranty' that covers the cost of replacing the vehicle's battery pack if it fails. This can be a valuable add-on, especially for seniors who might not be able to afford the high upfront cost of a new battery. But, be careful not to get taken in by unnecessary fees. If you're driving a Tesla, for instance, you might already have a battery warranty through the manufacturer. In that case, you wouldn't need to pay for it through your insurance company.

5 Things to Know About EV Insurance for Seniors

Here are five key things to keep in mind when shopping for EV insurance as a senior:

- 1. Depreciation matters: As we discussed earlier, electric cars tend to hold their value better than gas-powered vehicles. This can result in lower insurance premiums for seniors who drive EVs.

- 2. Shop around: Don't just assume that your current insurer will give you the best rate. Compare quotes from multiple companies to find the best deal.

- 3. Look for discounts: Some companies offer discounts for seniors who drive electric vehicles. These can range from 5-10% off the premium.

- 4. Read the fine print: Always read the policy carefully and ask questions if you're unsure about something. Watch out for hidden fees and charges.

- 5. Consider a specialty EV insurer: Companies that specialize in EV insurance might have more competitive rates and better coverage options for seniors.

What is the best EV insurance for seniors?

The best EV insurance for seniors will depend on a variety of factors, including the type of vehicle, driving history, and location. However, some companies that specialize in EV insurance, such as Tesla Insurance or EV Insurance by GEICO, might offer more competitive rates and better coverage options for seniors.

How much does EV insurance cost for seniors?

The cost of EV insurance for seniors can vary widely depending on the company and the vehicle. On average, seniors can expect to pay between $1,500 and $3,000 per year for insurance, although this can range from as low as $1,000 to over $5,000 per year.

Do seniors get discounts on EV insurance?

Yes, some companies offer discounts for seniors who drive electric vehicles. These can range from 5-10% off the premium and might be available for seniors who meet certain criteria, such as completing a defensive driving course or having a clean driving record.

What are the benefits of EV insurance for seniors?

The benefits of EV insurance for seniors include lower premiums due to slower depreciation, access to specialty EV insurers with more competitive rates and better coverage options, and discounts for seniors who drive electric vehicles.

How can seniors compare EV insurance quotes?

Seniors can compare EV insurance quotes by shopping around and researching different companies. They should look for companies that specialize in EV insurance and have experience with electric vehicles, and always read the fine print and ask questions if they're unsure about something.

What are some common mistakes seniors make when buying EV insurance?

Some common mistakes seniors make when buying EV insurance include not shopping around, not reading the fine print, and not considering specialty EV insurers. They might also overlook discounts or other benefits that could save them money on their premium.

Pro tip: always ask about discounts and promotions when shopping for EV insurance. Some companies might offer special deals for seniors or first-time buyers, which can help lower your premium.

And, finally, let's talk about the data. According to a study by the National Renewable Energy Laboratory, the average cost of insurance for an electric vehicle is around $1,674 per year, which is comparable to the cost of insurance for a gas-powered vehicle. However, this can vary widely depending on the company and the vehicle. For example, a senior driving a Tesla Model 3 might pay around $1,500 per year for insurance, while a senior driving a BMW iX might pay closer to $2,000 per year.

Well, actually, the best way to think about EV insurance is to consider the total cost of ownership. This includes not just the purchase price of the vehicle, but also the cost of insurance, maintenance, and fuel (or, in this case, electricity). When you factor in the lower operating costs of an electric vehicle, the overall cost of ownership can be significantly lower than that of a gas-powered vehicle. And, as a senior, you might be eligible for additional discounts or incentives that can help lower your premium even further.

That's my two cents. Take it or leave it — but I hope it helps. — Alex