Can you really write off your Tesla Model 3's insurance premiums as a business expense? Sound familiar? You're not alone - many EV owners are wondering if they can deduct their insurance costs on their tax return. Know what the kicker is? It's not a simple yes or no answer. Dead serious, the rules around EV insurance tax deductibility are murky, especially for seniors, freelancers, and business owners.

That one stung - I've seen people get audited for misclaiming EV insurance deductions. But hey, if you're using your EV for business, you might be eligible for some serious tax breaks. We've got a client, let's call her Rachel, who uses her Hyundai Ioniq 5 for freelance work - she can deduct a chunk of her insurance premiums as a business expense. Wild, right? The key is to keep accurate records and understand the rules around business use.

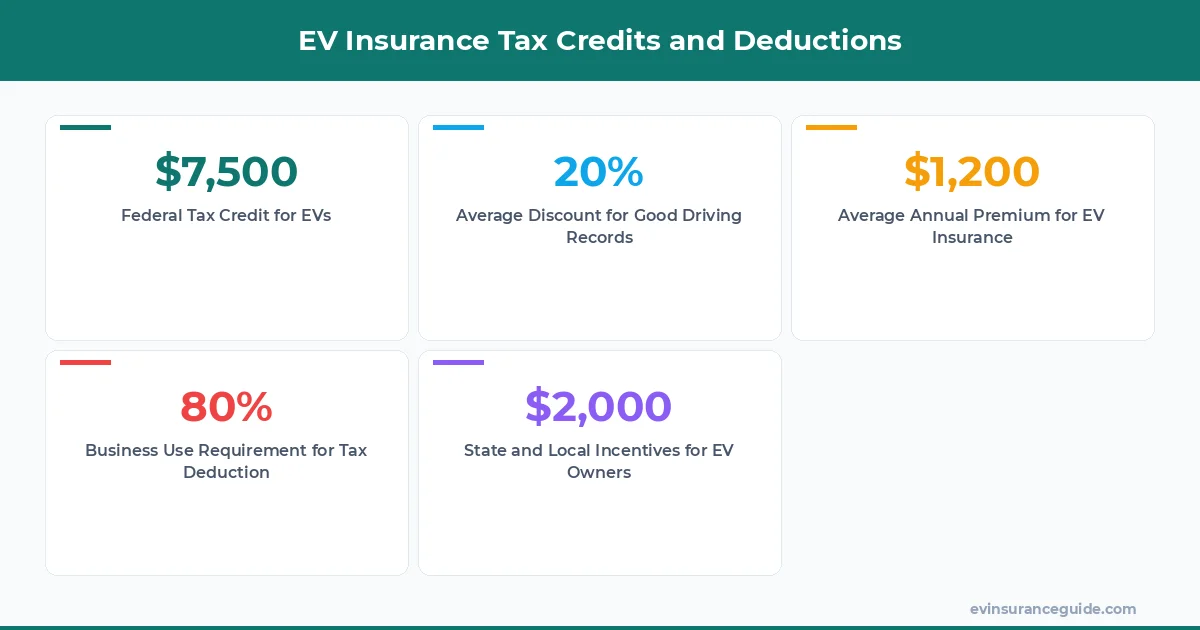

And, let's be real, the best EV insurance for seniors is not just about the price - it's about the coverage, the deductible, and the overall value. You don't wanna be stuck with a policy that doesn't cover your Rivian's expensive battery, right? That's why it's crucial to shop around, compare policies, and read the fine print. I'd recommend checking out companies like Geico, Progressive, or USAA - they offer some of the best EV insurance for seniors, with premiums starting from around $1,200 per year.

Can You Deduct EV Insurance as a Business Expense?

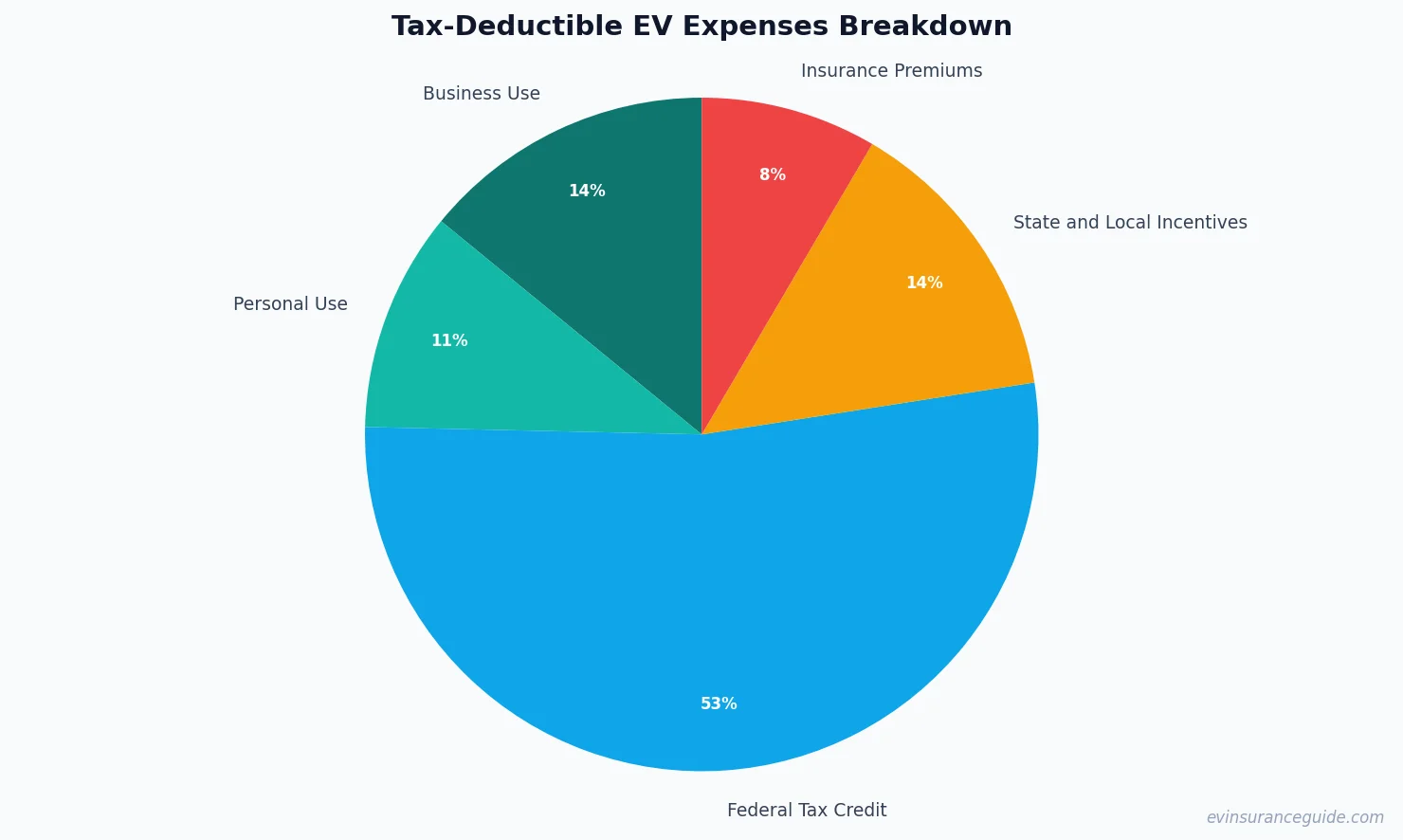

Well, actually, it depends on how you use your EV. If you're using it for business, you can deduct a portion of your insurance premiums as a business expense. But, if you're using it for personal use, you're out of luck. The IRS has strict rules around business use - you'll need to keep a log of your mileage, for example. And, let's not forget about the 80/20 rule - if you use your EV for business more than 80% of the time, you can deduct the full amount of your insurance premiums.

For instance, let's say you're a freelancer who uses your BMW iX for work 90% of the time. You can deduct around $1,800 of your insurance premiums as a business expense, assuming your annual premium is around $2,000. Not bad, right? But, if you're using your EV for personal use, you won't be able to deduct anything. Know what the difference is? It's all about the paperwork - you'll need to keep accurate records of your business use to qualify for the deduction.

Now, I know what you're thinking - what about the best EV insurance for seniors? Doesn't that factor into the equation? Yep, it does. If you're a senior, you'll want to look for policies that offer discounts for low mileage, good driving records, or defensive driving courses. And, some companies, like State Farm, offer usage-based insurance that can help you save money on your premiums.

This Best EV Insurance for Seniors is Overpriced Trash

OK, wait, scratch that - not all EV insurance policies are created equal. Some are downright expensive, with premiums ranging from $2,500 to $5,000 per year. That's why it's crucial to shop around, compare policies, and read the fine print. Don't just go with the first company you find - do your research, and look for policies that offer the best value for your money.

For example, I've seen policies from companies like Allstate that offer discounts for seniors, but the premiums are still sky-high. You'll want to look for companies that offer more competitive pricing, like Geico or Progressive. And, don't forget to ask about any additional fees or surcharges - you don't wanna be surprised by a huge bill at the end of the year.

But, what about the best EV insurance for seniors with a clean driving record? That's where things get interesting. Some companies offer discounts for good driving records, while others don't. You'll want to look for companies that reward safe driving, like USAA or Amica Mutual. And, don't forget to ask about any additional perks, like roadside assistance or rental car coverage.

3 Things You Need to Know About EV Insurance Tax Credits

Hmm, let me rethink that - there are actually more than three things you need to know about EV insurance tax credits. But, here are the top three: first, you can deduct a portion of your insurance premiums as a business expense if you use your EV for business; second, you may be eligible for a tax credit if you purchase a new EV; and third, you'll need to keep accurate records of your business use to qualify for the deduction.

Now, I know what you're thinking - what about the federal tax credit for EVs? Doesn't that factor into the equation? Yep, it does. If you purchase a new EV, you may be eligible for a tax credit of up to $7,500. But, there are some caveats - the credit starts to phase out once you've purchased a certain number of EVs, and it's only available for certain models. Wild, right?

And, let's not forget about state and local incentives - some states offer additional tax credits or rebates for EV owners. For example, California offers a rebate of up to $5,000 for EV owners, while New York offers a tax credit of up to $2,000. You'll want to check with your state and local government to see what incentives are available.

Myth-Busting: You Can't Deduct EV Insurance as a Personal Expense

Nope, that's not entirely true. While you can't deduct EV insurance as a personal expense, you may be able to deduct a portion of your insurance premiums as a business expense if you use your EV for business. And, if you're a freelancer or business owner, you may be eligible for additional tax deductions or credits.

But, what about the myth that EV insurance is more expensive than traditional insurance? That's not necessarily true. While EVs can be more expensive to insure, some companies offer competitive pricing for EV owners. You'll want to shop around, compare policies, and read the fine print to find the best deal for your money.

And, let's not forget about the myth that you need to itemize your deductions to claim EV insurance tax credits. That's not true - you can claim the standard deduction and still qualify for some tax credits. But, you'll need to keep accurate records of your business use to qualify for the deduction.

Comparing EV Insurance Policies: Which One is the Best Value?

Well, that's a tough one - it depends on your individual circumstances, like your driving record, mileage, and budget. But, here's a comparison of some popular EV insurance policies: Geico offers a premium of around $1,500 per year, while Progressive offers a premium of around $1,800 per year. USAA offers a premium of around $1,200 per year, but you'll need to be a military member or veteran to qualify.

Now, I know what you're thinking - what about the best EV insurance for seniors with a Tesla Model Y? That's a great question. Tesla offers its own insurance policy, which can be a good option for Tesla owners. But, you'll want to compare it to other policies to find the best value for your money.

And, let's not forget about the importance of customer service - you'll want to choose a company that offers 24/7 support, a user-friendly website, and a mobile app. Some companies, like State Farm, offer a range of additional perks, like usage-based insurance and roadside assistance.

What is the best EV insurance for seniors?

The best EV insurance for seniors is a policy that offers competitive pricing, good coverage, and additional perks like discounts for low mileage or good driving records. Some companies, like Geico or USAA, offer policies that cater to seniors, with premiums starting from around $1,200 per year.

Can I deduct EV insurance as a business expense?

Yes, you can deduct a portion of your EV insurance premiums as a business expense if you use your EV for business. But, you'll need to keep accurate records of your business use to qualify for the deduction. The IRS has strict rules around business use, so be sure to consult with a tax professional to ensure you're eligible.

What are the tax credits for EV owners?

There are several tax credits available for EV owners, including the federal tax credit of up to $7,500 and state and local incentives. You'll want to check with your state and local government to see what incentives are available. And, don't forget to keep accurate records of your business use to qualify for the deduction.

How do I choose the best EV insurance policy for my needs?

To choose the best EV insurance policy for your needs, you'll want to compare policies from different companies, read the fine print, and ask about any additional fees or surcharges. You'll also want to consider factors like customer service, coverage, and deductible. And, don't forget to shop around - you can save money by comparing policies and finding the best deal for your money.

Can I get a discount on my EV insurance policy?

Yes, you can get a discount on your EV insurance policy if you have a good driving record, low mileage, or take a defensive driving course. Some companies, like State Farm, offer usage-based insurance that can help you save money on your premiums. You'll want to ask about any available discounts when you're shopping for a policy.

What is the average cost of EV insurance?

The average cost of EV insurance is around $1,500 per year, but it can vary depending on your individual circumstances, like your driving record, mileage, and budget. You'll want to shop around, compare policies, and read the fine print to find the best deal for your money.

Remember, the best policy is the one you actually understand. — Alex