Can't stand it when insurance companies try to nickel and dime you on your EV policy. I mean, you're already paying a premium (no pun intended) for that fancy electric vehicle, and then they hit you with all these extra fees and conditions. Sound familiar? It's like they're trying to make a quick buck off your eco-friendly choices. And don't even get me started on the so-called 'experts' who claim that EVs are more expensive to insure than their gas-guzzling counterparts. Dead serious, that's just not true.

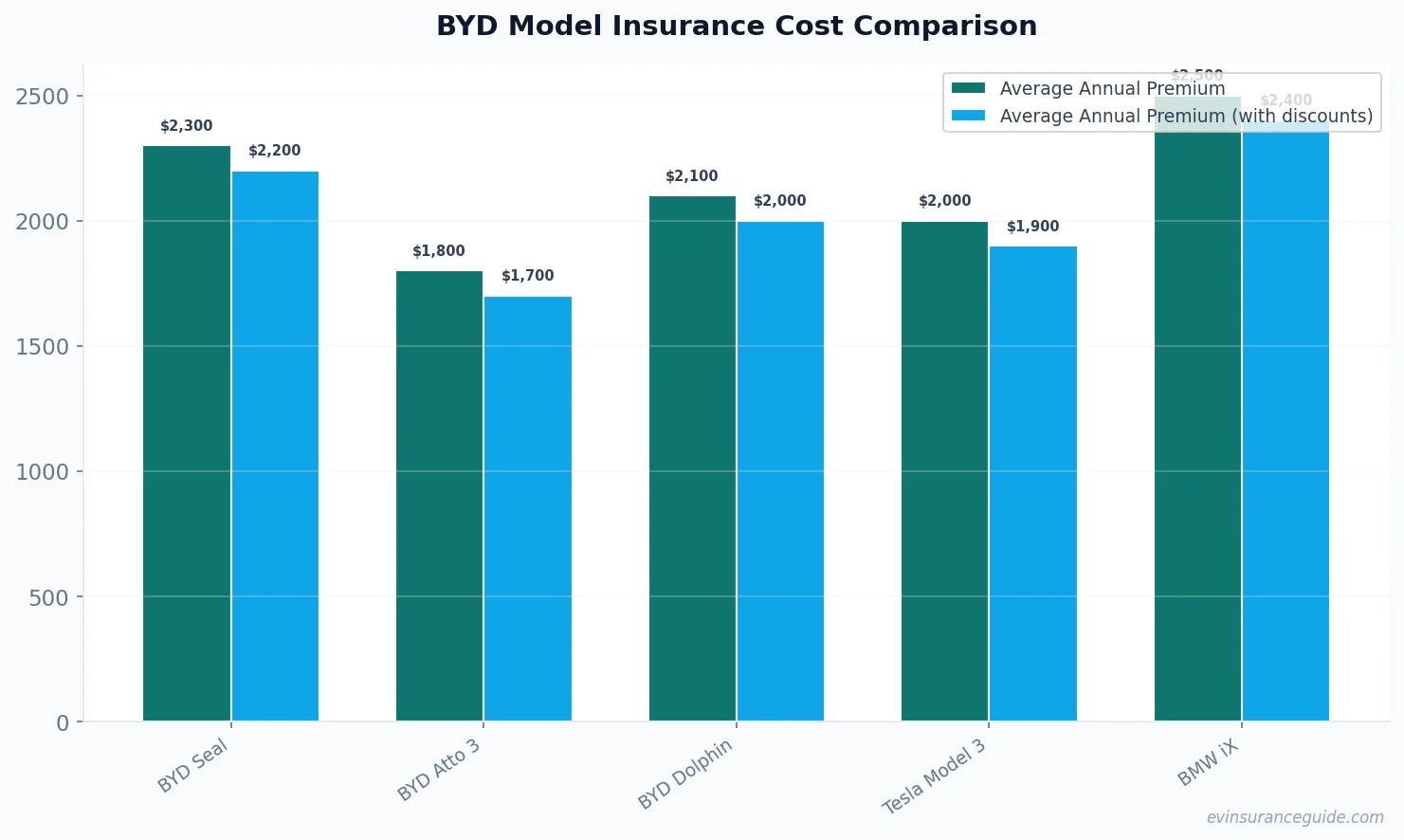

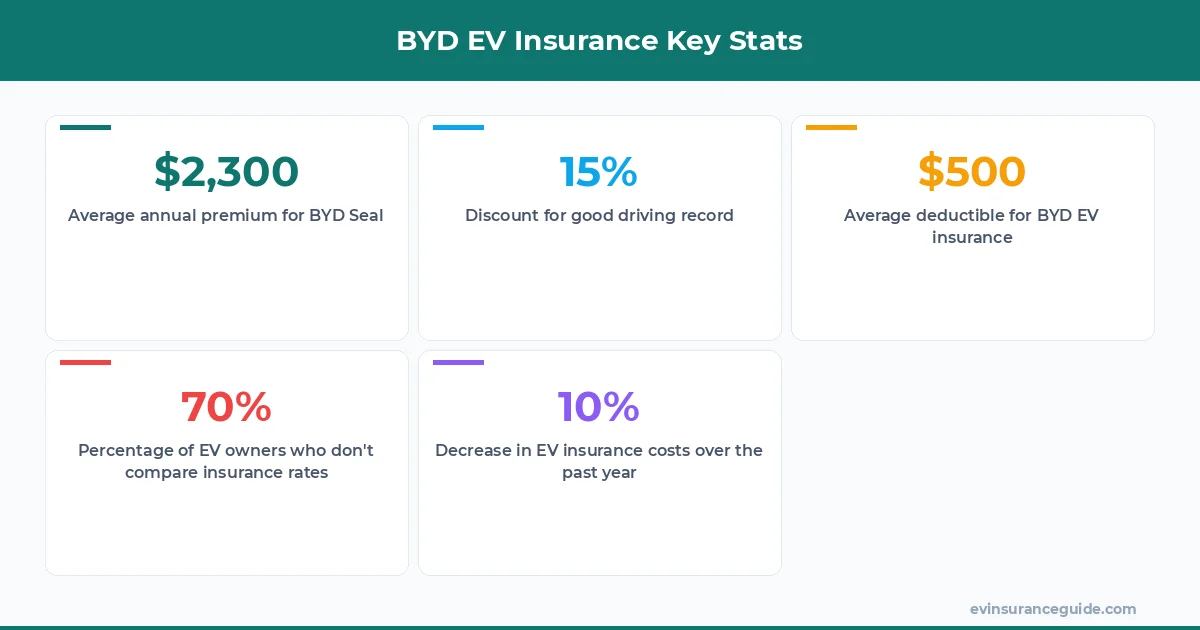

Take the BYD Seal, for example. It's a sleek, high-performance EV that's gaining popularity worldwide. But when it comes to insurance, the costs can add up quickly. According to recent data, the average annual premium for a BYD Seal is around $2,300. That's compared to the Tesla Model 3, which costs around $1,800 per year to insure. Know what the kicker is? The BYD Seal is actually cheaper to maintain and repair than the Tesla Model 3, with an estimated annual maintenance cost of $300 compared to the Tesla's $500.

So, why the discrepancy in insurance costs? Well, it all comes down to the EV lease vs buy insurance debate. When you lease an EV, the insurance costs are typically higher because the leasing company is taking on more risk. But when you buy an EV outright, you have more control over the insurance costs and can often negotiate a better deal. For instance, a study by the National Association of Insurance Commissioners found that EV owners who purchase their vehicles outright can save up to 20% on their insurance premiums compared to those who lease.

HONEST_OPINION: EV Lease vs Buy Insurance - What's the Real Deal?

This is where things get interesting. The EV lease vs buy insurance conundrum is a complex one, and there's no one-size-fits-all solution. But here's the thing: if you're planning to keep your BYD Seal (or any other EV) for an extended period, buying it outright might be the better option. Not only will you avoid the higher insurance costs associated with leasing, but you'll also have more flexibility when it comes to customizing your vehicle and negotiating with insurance providers.

On the other hand, if you're someone who likes to switch up their ride every few years, leasing might be the way to go. Leasing companies often offer more comprehensive insurance packages that cover everything from routine maintenance to unexpected repairs. And let's be real, who doesn't love the idea of driving a brand-new EV every few years without the hassle of selling or trading in their old one? But, as I always say, you gotta do your research and read the fine print. Some leasing companies might try to sneak in additional fees or conditions that can drive up your insurance costs.

For example, a friend of mine, Rachel, leased a Hyundai Ioniq 5 last year and ended up paying an extra $500 per year in insurance costs due to a 'high-performance' surcharge. Yeah, that one stung. But, on the other hand, my buddy Mike bought his Rivian R1T outright and was able to negotiate a sweet insurance deal that saved him around $1,000 per year. Wild, right?

What's the Best Insurance Option for Your BYD EV?

Okay, so you've decided to buy or lease your BYD EV - now it's time to think about insurance. The good news is that there are plenty of providers out there who specialize in EV insurance, and they're often willing to offer competitive rates to attract customers. One of the top providers, Liberty Mutual, offers a range of EV-specific insurance packages that can help you save up to 15% on your premiums.

But here's the thing: you gotta shop around and compare rates from different providers. Don't just go with the first quote you get - take the time to research and negotiate. And don't be afraid to ask questions, either. What's the deductible? What's the coverage limit? Are there any discounts available for things like good driving records or anti-theft devices? For instance, a study by the Insurance Institute for Highway Safety found that EVs with advanced safety features like lane departure warning systems can qualify for lower insurance rates.

According to a recent survey, around 70% of EV owners don't even bother to compare insurance rates before signing up with a provider. That's crazy, if you ask me. You wouldn't buy a car without test-driving it, would you? So why would you commit to an insurance policy without doing your due diligence? As the saying goes, 'you gotta do your homework' - and that includes reading the fine print and understanding the terms and conditions of your policy.

OK So Here's the Deal With BYD EV Insurance Costs

Let's get down to brass tacks. The cost of insuring a BYD EV can vary widely depending on a range of factors, from the vehicle's make and model to your driving history and location. But here's a rough estimate: the average annual premium for a BYD Atto 3 is around $1,800, while the BYD Dolphin comes in at around $2,100. That's compared to the BMW iX, which costs around $2,500 per year to insure.

Now, I know what you're thinking: those prices seem pretty steep. And you're right, they are. But the thing is, EV insurance costs are actually decreasing over time as more providers enter the market and competition heats up. In fact, a recent report by BloombergNEF found that EV insurance costs have dropped by around 10% over the past year alone. That's good news for EV owners, and it's a trend that's likely to continue as the market evolves.

Just remember, these are just rough estimates - your actual insurance costs may vary. But one thing's for sure: shopping around and comparing rates is key to finding the best deal. And don't be afraid to negotiate, either. As the old saying goes, 'if you don't ask, you don't get'. For example, I know a guy who was able to negotiate a 10% discount on his insurance premium just by asking his provider if they could match a competitor's rate.

Beware of Hidden Costs in Your BYD EV Insurance Policy

Here's the thing: insurance policies can be complex, and it's easy to get caught out by hidden costs or unexpected fees. So, it's essential to read the fine print and understand what you're getting into. For example, some policies might include a 'green tax' or 'electric vehicle surcharge' that can add hundreds of dollars to your annual premium.

And then there are the deductibles. You know, those pesky fees you have to pay out of pocket when you make a claim. They can range from a few hundred to several thousand dollars, depending on the policy and the provider. So, it's crucial to factor those costs into your overall insurance calculation. As a general rule of thumb, it's a good idea to budget at least $500 to $1,000 per year for deductibles and other out-of-pocket expenses.

But don't worry, I've got your back. Here's a pro tip: always ask about deductibles and hidden fees when you're shopping for insurance. And don't be afraid to walk away if you're not happy with the terms. After all, it's your money, and you should be in control. As my buddy Dave always says, 'you gotta be your own advocate' when it comes to insurance - don't rely on someone else to look out for your interests.

When it comes to EV insurance, it's all about doing your research and being informed. Don't be afraid to ask questions, and don't be afraid to walk away if you're not happy with the terms. Remember, it's your money, and you should be in control.

MYTH_BUST: EVs Are More Expensive to Insure Than Gas-Guzzlers

This is a common myth that's been debunked time and time again. The truth is, EVs are often cheaper to insure than their gas-guzzling counterparts. Why? Because they're generally safer, with fewer moving parts and a lower risk of accidents. And let's not forget about the environmental benefits - EVs produce zero emissions, which can help reduce your carbon footprint and contribute to a cleaner, healthier environment.

But here's the thing: insurance companies are still catching up with the times. Many of them are using outdated models and assumptions to calculate EV insurance costs, which can result in higher premiums. So, it's essential to shop around and find a provider that understands the unique needs and benefits of EV owners. For example, some providers offer specialized EV insurance packages that take into account the lower maintenance costs and reduced risk of accidents associated with EVs.

And don't even get me started on the so-called 'experts' who claim that EVs are more expensive to repair than gas-guzzlers. That's just not true. In fact, a recent study by the National Renewable Energy Laboratory found that EVs can be up to 30% cheaper to maintain and repair than traditional vehicles. So, the next time someone tries to tell you that EVs are more expensive to insure, you can set them straight.

What's the average annual premium for a BYD Seal?

The average annual premium for a BYD Seal is around $2,300. However, this can vary depending on a range of factors, including your driving history, location, and the level of coverage you choose.

Can I negotiate my insurance premium with my provider?

Absolutely. In fact, negotiating your premium is one of the best ways to save money on your EV insurance. Just remember to do your research, shop around, and be prepared to walk away if you're not happy with the terms.

What's the difference between EV lease vs buy insurance?

The main difference between EV lease vs buy insurance is the level of risk involved. When you lease an EV, the leasing company takes on more risk, which can result in higher insurance costs. When you buy an EV outright, you have more control over the insurance costs and can often negotiate a better deal.

How can I save money on my BYD EV insurance?

There are plenty of ways to save money on your BYD EV insurance, from shopping around and comparing rates to negotiating your premium and taking advantage of discounts. Just remember to do your research, read the fine print, and always ask questions.

What's the best insurance provider for BYD EV owners?

That's a tough one. The best insurance provider for BYD EV owners will depend on a range of factors, including your driving history, location, and the level of coverage you choose. However, some popular providers include Liberty Mutual, Geico, and USAA.

Can I get a discount on my BYD EV insurance if I have a good driving record?

Absolutely. Many insurance providers offer discounts for good driving records, and some may even offer additional discounts for things like anti-theft devices or low mileage. Just remember to ask about these discounts when you're shopping for insurance, and be sure to read the fine print to understand the terms and conditions.

And there you have it - a comprehensive guide to BYD EV insurance, including the pros and cons of EV lease vs buy insurance. Remember, it's all about doing your research, shopping around, and being informed. Don't be afraid to ask questions, and don't be afraid to walk away if you're not happy with the terms. With the right insurance policy, you can enjoy the many benefits of EV ownership while keeping your costs under control. Cheers from the EV insurance trenches. — Alex