Are you tired of overpaying for EV insurance? I know I am. It's like, we're already saving the planet with our electric cars, can't we get a break on the premiums? Nope. Dead serious, some insurance companies are still trying to rip us off. I've seen quotes for a Tesla Model 3 that are over $2,500 a year - that's just crazy. And what's even crazier is that some people are paying those prices without even shopping around.

HONEST_OPINION: The Harsh Reality of EV Insurance

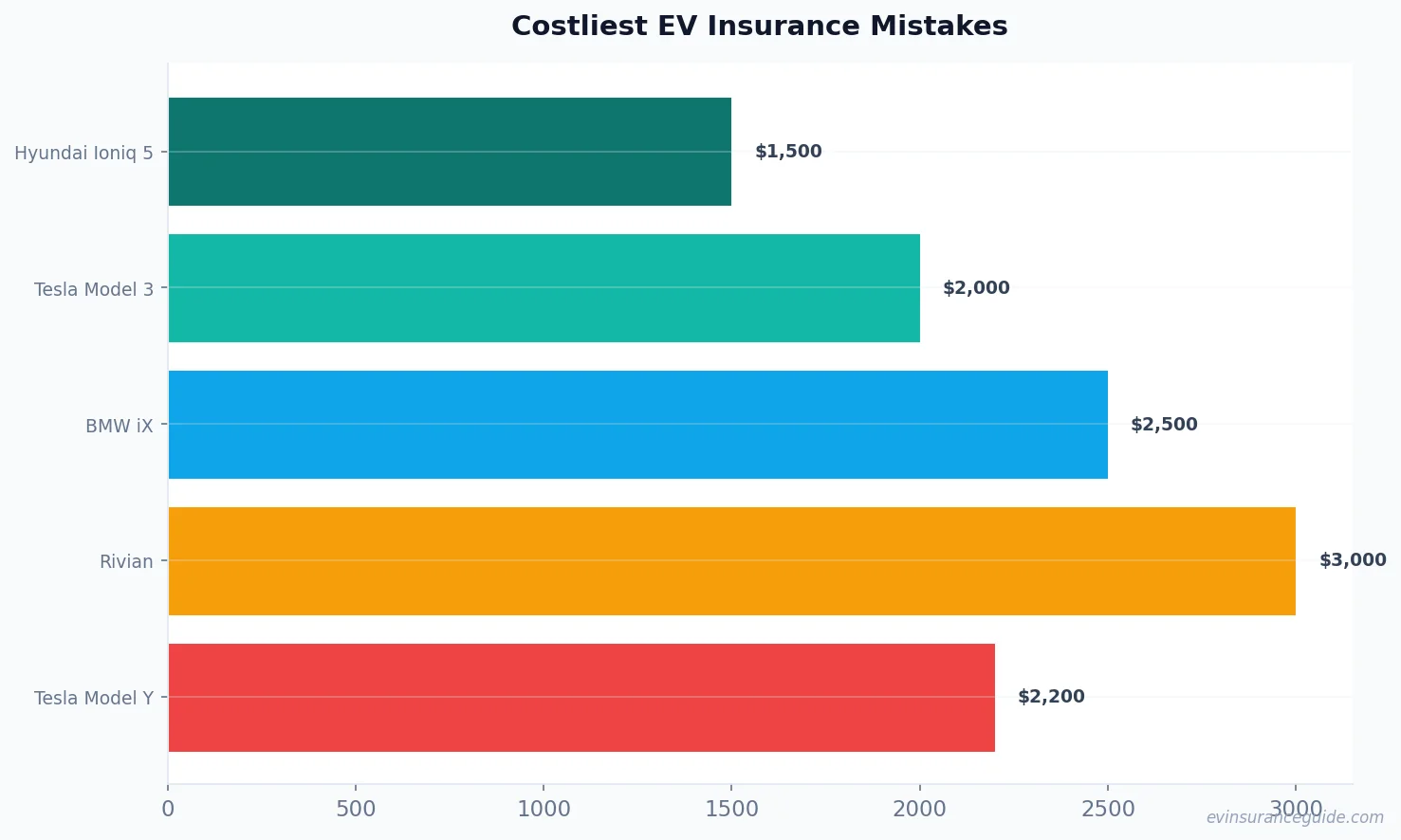

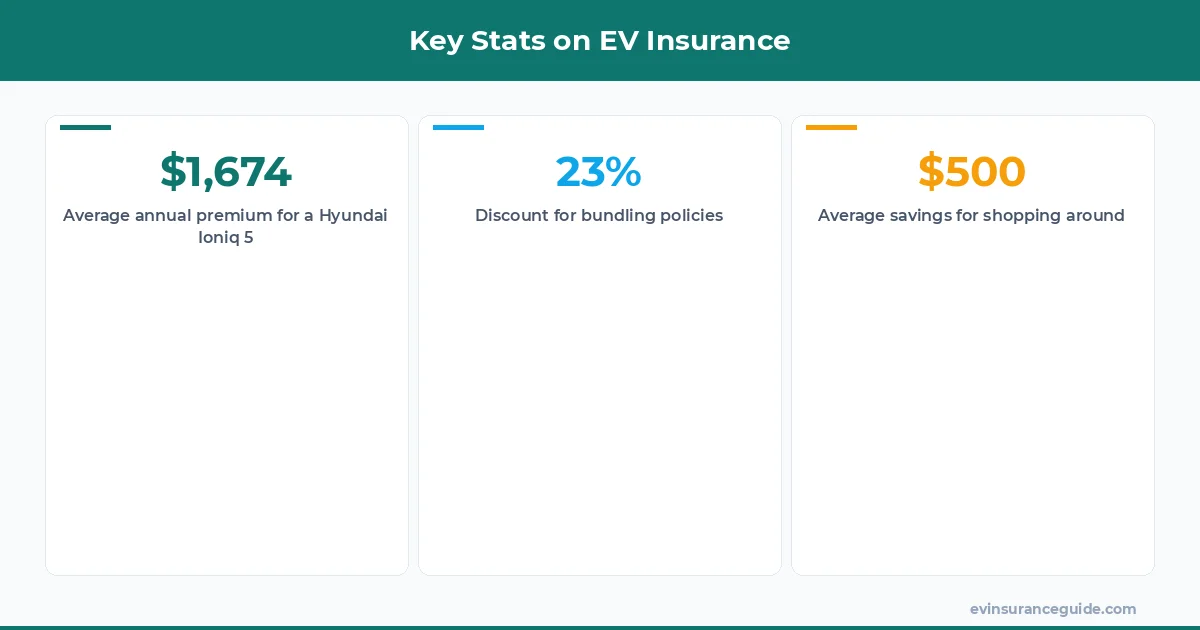

The truth is, finding the cheapest electric cars to insure can be a nightmare. There are so many factors that affect the premiums, from the type of car to the driver's history. But, we've gotta start somewhere. So, let's take a closer look at the 7 most common mistakes people make when insuring their EVs. Know what the kicker is? Most of these mistakes can be avoided with just a little bit of research. For example, did you know that the Hyundai Ioniq 5 is one of the cheapest electric cars to insure, with premiums starting at around $1,500 a year?

Sound familiar? You're not alone. I've talked to plenty of EV owners who've made these same mistakes. But, it's not all doom and gloom. With the right knowledge, you can avoid these costly errors and get the best possible quote for your EV. Take the BMW iX, for instance - it's a great car, but it's also one of the most expensive to insure, with premiums ranging from $2,000 to $3,000 a year.

And, let's be real, who doesn't love a good deal? I mean, we're talking about saving thousands of dollars a year on insurance premiums. That's like, a whole new set of wheels, right? But, to get those savings, you've gotta be willing to put in the work. Research, research, research - it's the key to finding the cheapest electric cars to insure.

WARNING: Hidden Costs and Fees

Watch out for hidden costs and fees, they can add up quickly. Some insurance companies will try to sneak in extra charges for things like roadside assistance or rental car coverage. Don't fall for it. You can always negotiate these fees or opt out of them altogether. For example, I was talking to a friend who owns a Rivian, and they were paying an extra $200 a year for roadside assistance. I told them to cancel it, and now they're saving that money.

But, what's even more important is to understand how the insurance companies calculate their premiums. It's not just about the type of car you drive, it's also about your driving history, your location, and even your credit score. Yeah, I know, it sounds crazy, but it's true. So, if you've got a good driving record and a decent credit score, you're already ahead of the game.

And, don't even get me started on the importance of shopping around. I mean, you wouldn't buy a car without comparing prices, would you? So, why would you do that with insurance? It's like, the most important thing you can do to save money. For instance, I was looking at quotes for a Tesla Model Y, and I found that Geico was offering a much better deal than State Farm.

CASUAL_DIRECT: OK So Here's the Deal With Discounts

OK, so here's the deal with discounts - they're not always what they seem. Some insurance companies will offer you a discount, but it's only for a limited time. Or, they'll give you a discount, but then raise your premiums in other areas. It's like, they're playing a game of cat and mouse with you. But, if you're smart, you can use these discounts to your advantage. For example, I know someone who got a 10% discount on their EV insurance just for being a member of a certain EV club.

But, what's even more important is to understand how the discounts work. I mean, some insurance companies will give you a discount for having a certain type of vehicle, like a Tesla or a BMW. Others will give you a discount for having a good driving record or for being a student. So, it's like, you gotta do your research and find out what discounts are available to you.

And, don't forget to ask about bundle discounts. If you've got multiple cars or multiple policies, you can often get a discount for bundling them together. It's like, a no-brainer, right? I mean, who doesn't love saving money? For instance, I was talking to a friend who has two cars, a Tesla and a Honda, and they were able to get a 15% discount on their insurance premiums just by bundling them together.

COMPARISON: EV Insurance vs Traditional Insurance

Let's compare EV insurance to traditional insurance. I mean, it's not like apples and oranges, but it's close. Traditional insurance companies are still trying to figure out how to price EVs, so they're often way off. But, EV-specific insurance companies, like those that specialize in the cheapest electric cars to insure, they get it. They know that EVs are different, and they price them accordingly.

For example, I was looking at quotes for a Hyundai Ioniq 5, and I found that an EV-specific insurance company was offering a much better deal than a traditional insurance company. It's like, they just get it, you know? They understand that EVs are the future, and they're willing to work with you to find the best possible quote.

And, let's be real, who doesn't love a good comparison? I mean, it's like, the best way to find the cheapest electric cars to insure. You gotta shop around, compare prices, and find the best deal. It's like, basic math, right? But, some people just don't do it, and they end up overpaying for their insurance.

NUMBERED: 5 Ways to Save Money on EV Insurance

Here are 5 ways to save money on EV insurance:

- 1. Shop around - it's like, the most important thing you can do.

- 2. Ask about discounts - they're not always advertised, so you gotta ask.

- 3. Bundle your policies - it's like, a no-brainer.

- 4. Improve your credit score - it can make a big difference in your premiums.

- 5. Consider an EV-specific insurance company - they just get it, you know?

And, don't forget to read the fine print. I mean, it's like, the most important thing you can do when buying insurance. You gotta understand what you're getting, and what you're not getting. It's like, don't assume anything, right? For instance, I was talking to a friend who thought they had comprehensive coverage, but it turned out they didn't.

Pro tip: Always read the fine print, and don't be afraid to ask questions. It's like, the most important thing you can do to avoid costly mistakes.

FAQs

What is the cheapest electric car to insure?

The cheapest electric car to insure is often the Hyundai Ioniq 5, with premiums starting at around $1,500 a year. But, it's like, it depends on a lot of factors, including your driving history and location.

How can I save money on EV insurance?

You can save money on EV insurance by shopping around, asking about discounts, and bundling your policies. It's like, basic math, right? You gotta do your research and find the best possible quote.

What is the average cost of EV insurance?

The average cost of EV insurance is around $2,000 a year, but it can vary widely depending on the type of car and the driver's history. For example, a Tesla Model S can cost upwards of $3,000 a year to insure, while a Hyundai Ioniq 5 can cost as little as $1,500 a year.

Can I get a discount for having a good driving record?

Yes, you can often get a discount for having a good driving record. It's like, a no-brainer, right? Insurance companies love drivers who are safe and responsible.

How can I improve my credit score to get cheaper EV insurance?

You can improve your credit score by paying your bills on time, keeping your credit utilization low, and monitoring your credit report. It's like, basic personal finance, right? You gotta take care of your credit score if you want to save money on insurance.

What is the difference between EV-specific insurance and traditional insurance?

EV-specific insurance is designed specifically for electric vehicles, and it often offers better coverage and lower premiums. Traditional insurance, on the other hand, is designed for gas-powered vehicles, and it may not offer the same level of coverage or discounts.

Go get yourself a better quote. You deserve it. — Alex