Breaking news: just last week, Tesla announced a significant decrease in insurance rates for their Model 3 and Model Y owners, with some drivers seeing savings of up to $500 per year. This got me thinking - what other electric vehicles offer affordable insurance options, and which add-ons are actually worth paying for? Sound familiar? You're probably wondering how you can get in on these savings. Well, let's break it down.

A Story of Two EV Owners

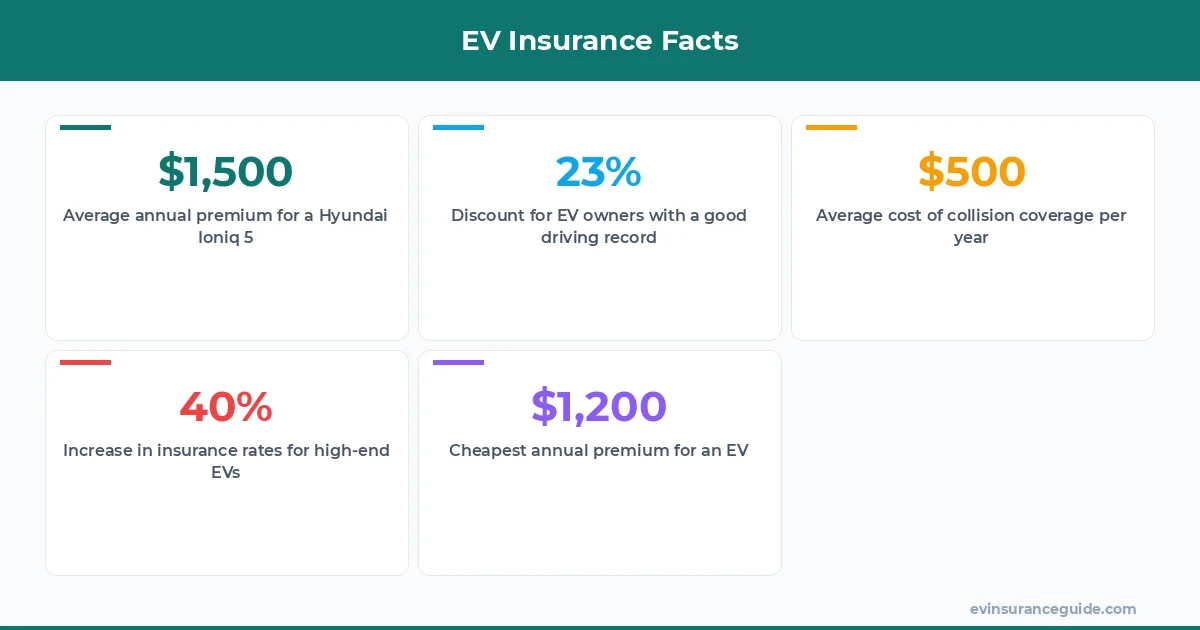

I've got a friend, let's call him Dave, who owns a BMW iX - a sleek, high-end electric SUV. He's been paying a pretty penny for insurance, around $2,500 per year, despite having a clean driving record. On the other hand, I've got another friend, Rachel, who drives a Hyundai Ioniq 5 - a more budget-friendly option. She's only paying around $1,800 per year for her insurance. That's a significant difference, and it's all because of the vehicle make and model. Know what the kicker is? Rachel's got some add-ons that Dave doesn't, and they're actually saving her money in the long run.

But what about the cheapest electric cars to insure? If you're in the market for a new EV, you'll want to consider models like the Nissan Leaf, the Chevrolet Bolt, or the Ford Mustang Mach-E. These vehicles tend to have lower insurance rates, with some owners paying as little as $1,200 per year. And if you're looking for add-ons, you might want to consider collision coverage, which can cost anywhere from $200 to $500 per year, depending on your provider and location.

Comparing Add-Ons: Tesla vs Rivian

So, how do the add-ons compare between different EV manufacturers? Let's take a look at Tesla and Rivian, two popular brands with very different approaches to insurance. Tesla offers a range of add-ons, including collision coverage, roadside assistance, and even a "Valet" service that will come to you if you're stranded. Rivian, on the other hand, offers more basic add-ons, like collision coverage and liability insurance. But here's the thing - Rivian's add-ons are often cheaper than Tesla's, with some owners paying as little as $100 per year for collision coverage. That's a significant difference, especially when you consider that Rivian's vehicles are often more expensive than Tesla's. Wild, right?

And then there's the issue of insurance rates for specific models. For example, the Tesla Model 3 is generally cheaper to insure than the Model Y, with some owners paying around $1,500 per year for the Model 3 versus $1,800 per year for the Model Y. But if you opt for the BMW iX, you're looking at insurance rates of $2,500 per year or more. That's a big difference, especially when you consider that the iX is a more expensive vehicle to begin with.

OK So Here's the Deal With Add-Ons

Add-ons can be a great way to customize your insurance policy and get the coverage you need. But they can also be a waste of money if you're not careful. For example, if you've got a brand-new EV, you might not need collision coverage - at least, not until the vehicle is a few years old. And if you've got a good driving record, you might not need roadside assistance. But if you're driving a high-end EV like the Rivian R1T, you might want to consider add-ons like valet service or rental car coverage. These can be pricey, but they can also give you peace of mind.

And let's not forget about the cheapest electric cars to insure. If you're looking for a budget-friendly option, you might want to consider models like the Hyundai Kona Electric or the Audi e-tron. These vehicles tend to have lower insurance rates, with some owners paying as little as $1,500 per year. And if you're looking for add-ons, you might want to consider collision coverage or liability insurance.

Honestly, Some Add-Ons Are a Waste of Money

Dead serious - some add-ons are just not worth the cost. For example, if you've got a low-end EV, you might not need all the bells and whistles that come with premium insurance policies. And if you're a good driver, you might not need accident forgiveness or other perks that can drive up the cost of your policy. But if you're driving a high-end EV like the Tesla Model S, you might want to consider add-ons like luxury rental car coverage or valet service. These can be pricey, but they can also give you peace of mind.

Pro tip: always read the fine print before signing up for any insurance policy. You don't want to end up with a bunch of add-ons you don't need, or worse, find out that your policy doesn't cover something you thought it did. That one stung - I learned the hard way.

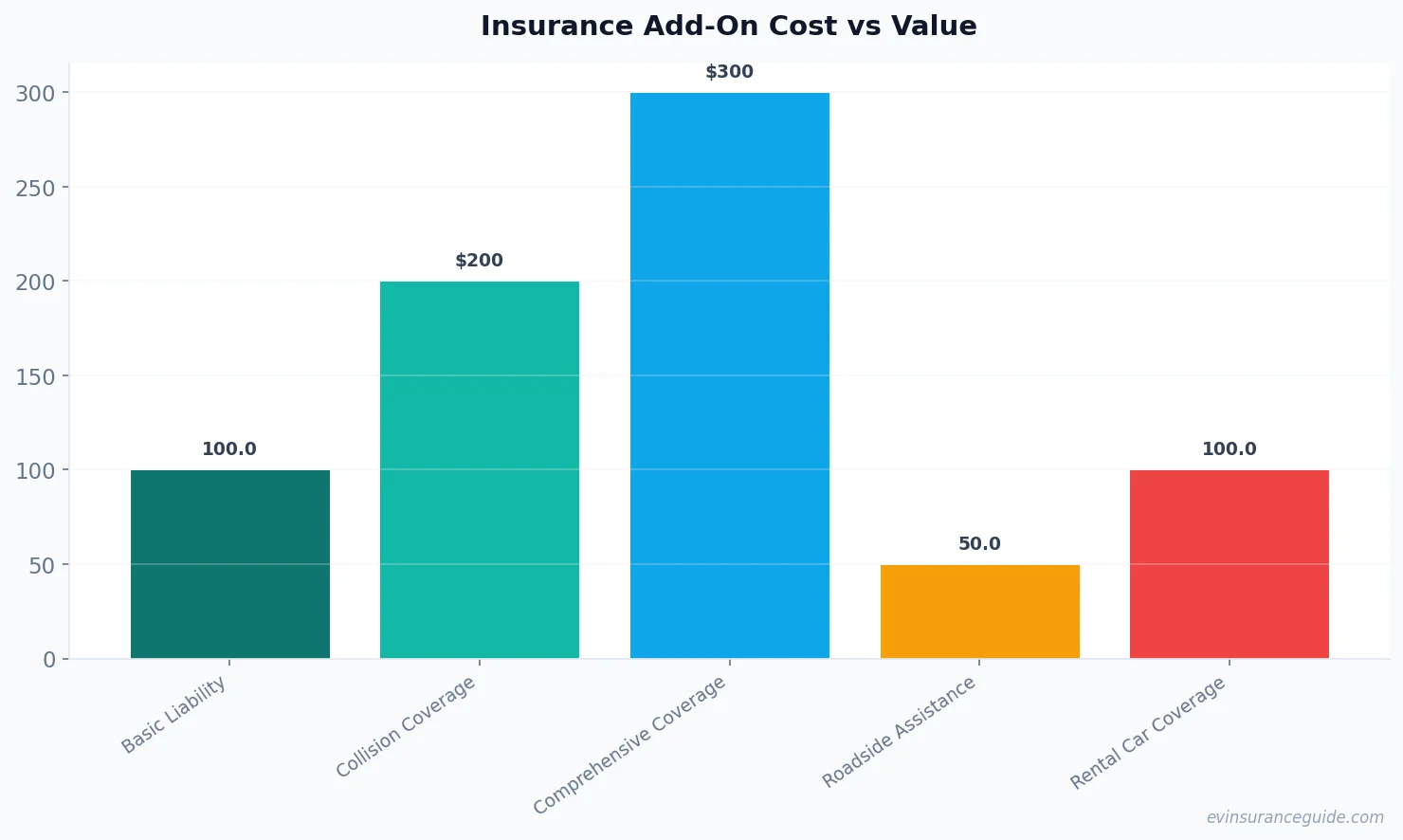

5 Add-Ons That Are Actually Worth Paying For

So, what are the add-ons that are actually worth paying for? Here are five options to consider:

- 1. Collision coverage - this can be a lifesaver if you're in an accident, and it's often relatively affordable, with costs ranging from $200 to $500 per year.

- 2. Roadside assistance - if you've got an EV, you know how important it is to have someone to call if you're stranded. This can be especially important if you're driving in areas with limited charging infrastructure.

- 3. Rental car coverage - if you're in an accident or your vehicle is in the shop, rental car coverage can be a huge help. This can cost anywhere from $50 to $200 per year, depending on your provider and location.

- 4. Liability insurance - this is a must-have for any vehicle owner, and it's often relatively affordable, with costs ranging from $100 to $300 per year.

- 5. Glass repair - if you've got a high-end EV with fancy glass features, you'll want to consider glass repair coverage. This can cost anywhere from $50 to $100 per year, depending on your provider and location.

Frequently Asked Questions

#### What's the Cheapest Electric Car to Insure?

The cheapest electric car to insure is often the Hyundai Ioniq 5, with some owners paying as little as $1,200 per year. However, this can vary depending on your location, driving record, and other factors.

#### How Much Do Add-Ons Cost?

Add-ons can cost anywhere from $50 to $500 per year, depending on the type of coverage and your provider. For example, collision coverage can cost around $200 to $500 per year, while roadside assistance can cost around $50 to $100 per year.

#### Do I Need Add-Ons for My EV?

It depends on your specific situation. If you've got a brand-new EV, you might not need add-ons like collision coverage or roadside assistance. But if you've got a high-end EV or you're driving in areas with limited charging infrastructure, you might want to consider add-ons like valet service or rental car coverage.

#### Can I Customize My Insurance Policy?

Yes, most insurance providers offer customizable policies that allow you to add or remove add-ons as needed. This can be a great way to tailor your policy to your specific needs and budget.

#### How Do I Choose the Right Insurance Provider?

When choosing an insurance provider, consider factors like cost, coverage, and customer service. You'll also want to read reviews and do your research to find the best provider for your needs.

#### What's the Average Cost of Insurance for an EV?

The average cost of insurance for an EV can vary widely depending on the make and model of your vehicle, as well as your location and driving record. However, some owners pay as little as $1,200 per year, while others pay $2,500 or more.

#### Are There Any Discounts Available for EV Owners?

Yes, some insurance providers offer discounts for EV owners, especially those who drive eco-friendly vehicles or have a good driving record. You'll want to ask about these discounts when shopping for a policy.

#### How Do I Know Which Add-Ons Are Worth Paying For?

It's all about weighing the costs and benefits. Consider your specific situation and needs, and then research the different add-ons available. You might want to consult with an insurance expert or do some online research to find the best options for your budget and lifestyle.

Until next time — Alex