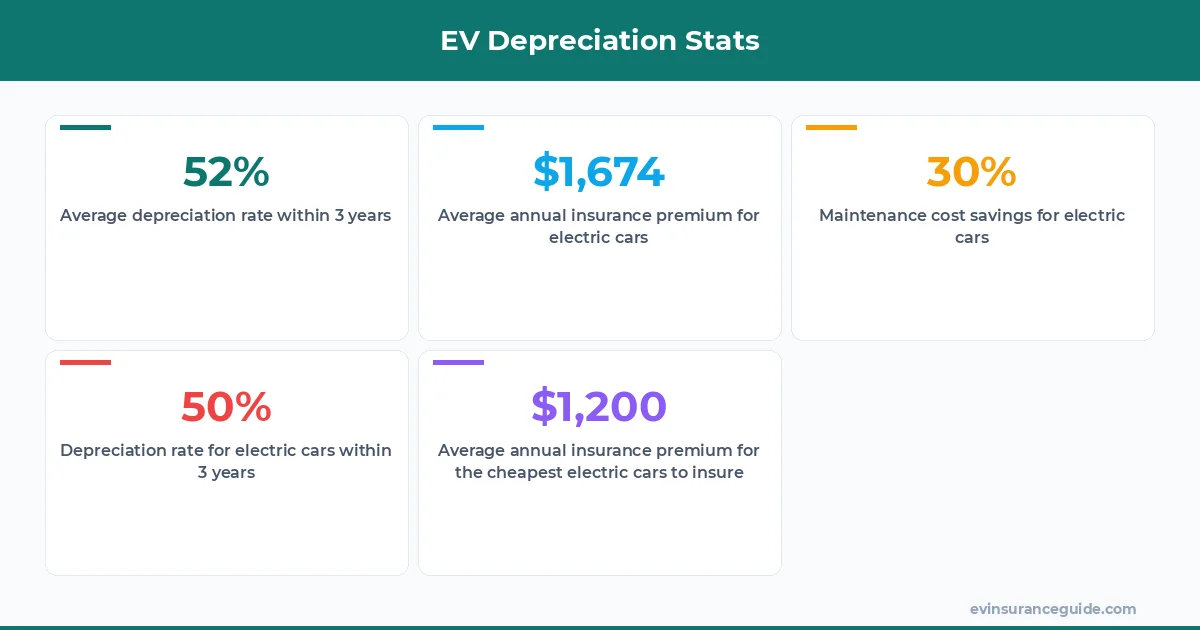

The average electric car loses around 52% of its value within the first three years of ownership - sound familiar? That's a huge hit, especially when you consider the prices of some of these vehicles. Take the Tesla Model 3, for instance - it can cost upwards of $50,000 brand new. But after three years, it's worth around $24,000. That's a loss of $26,000. Wild, right?

Now, you might be thinking - what's the big deal? Cars depreciate, it's just part of the game. But the thing is, electric cars depreciate faster than their gas-guzzling counterparts. And that affects your insurance premiums. Know what the kicker is? Insurance companies take depreciation into account when calculating your premiums. So, if your car is losing value fast, you'll likely end up paying more for insurance in the long run.

A Story of EV Depreciation

I've got a friend, let's call him Ryan, who bought a brand new BMW iX last year. He paid around $80,000 for it, and it was a beauty. But fast forward to today, and that same car is worth around $40,000. That one stung. Ryan's insurance premiums have gone up by around $500 per year, and he's not happy about it. Dead serious, it's like the insurance companies are just waiting for your car to depreciate so they can hike up your premiums.

But here's the thing - not all electric cars depreciate at the same rate. Some, like the Hyundai Ioniq 5, hold their value pretty well. In fact, the Ioniq 5 has been named one of the cheapest electric cars to insure, with average annual premiums ranging from $1,200 to $1,800.

And then there are cars like the Rivian, which have seen some crazy depreciation rates. I mean, we're talking around 70% loss of value within the first two years of ownership. That's insane. But, on the other hand, the Rivian is also one of the most expensive electric cars out there, with prices starting at around $70,000. So, it's not all bad news.

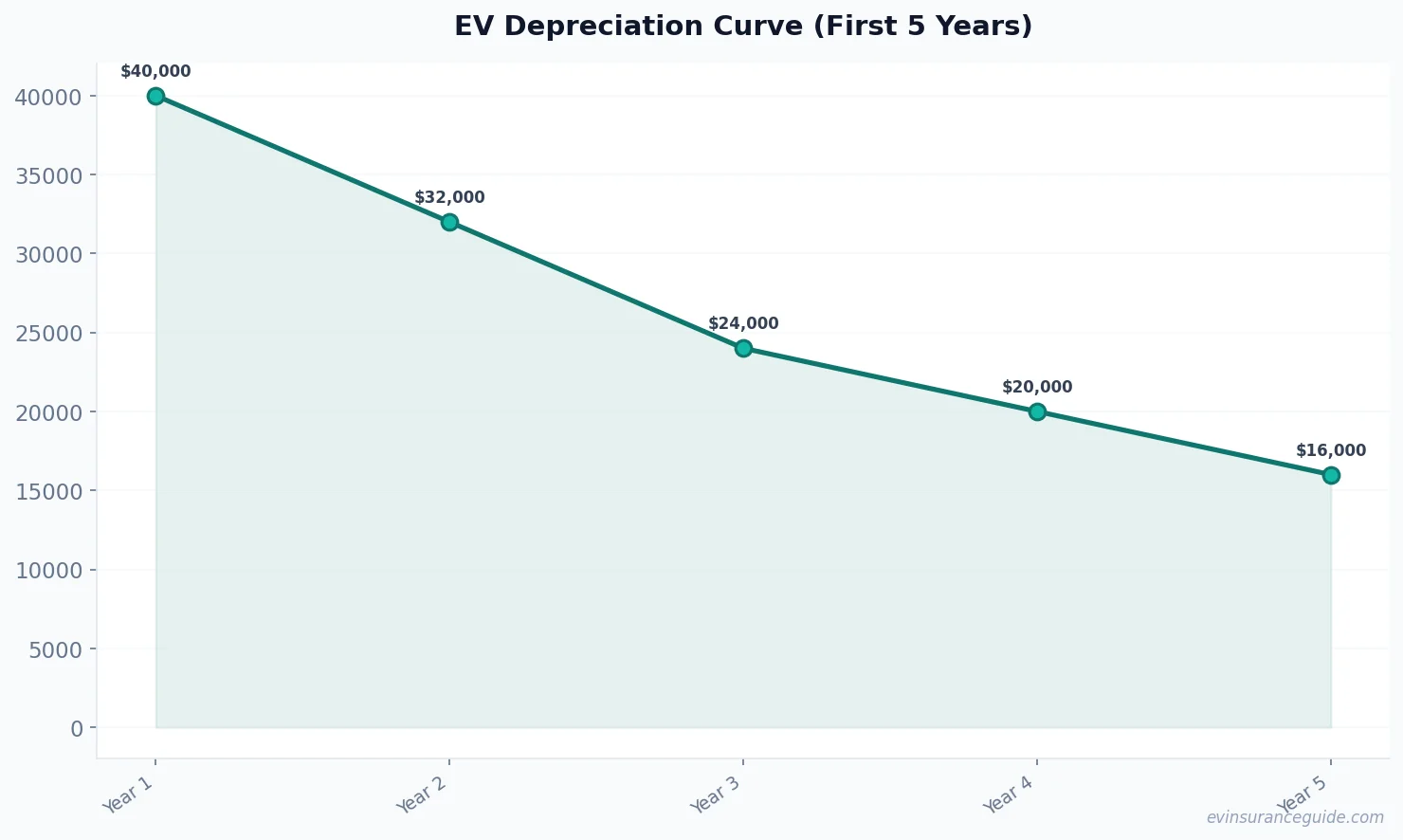

5 Years of EV Depreciation Data

Over the past five years, we've seen some significant changes in the way electric cars depreciate. For instance, back in 2018, the average electric car would lose around 30% of its value within the first year of ownership. Fast forward to today, and that number has jumped to around 40%. Know what that means? It means insurance companies are taking a closer look at depreciation rates when calculating your premiums.

In fact, some insurance companies, like Geico and Progressive, have started offering specialized insurance policies for electric car owners. These policies take into account the unique depreciation rates of electric cars, and they can end up saving you money in the long run.

But, let's be real - these policies can also be pretty expensive. I mean, we're talking around $2,000 to $3,000 per year, depending on the make and model of your car. That's why it's so important to shop around and compare rates before making a decision.

Can You Really Save Money on EV Insurance?

So, the big question is - can you really save money on EV insurance? The answer is yes, but it's not always easy. You've got to do your research, compare rates, and find the best policy for your specific needs.

For instance, if you own a Tesla Model Y, you might be able to find a policy that costs around $1,500 per year. But, if you own a BMW iX, you might be looking at premiums of around $2,500 per year. That's a big difference, and it's all because of depreciation rates.

Pro tip: when shopping for EV insurance, make sure to ask about depreciation rates and how they'll affect your premiums. Some insurance companies, like State Farm, offer specialized policies that take into account the unique depreciation rates of electric cars.

And, let's not forget about the cheapest electric cars to insure. I mean, we're talking about cars like the Nissan Leaf, which can cost as little as $1,000 per year to insure. That's a steal, especially when you consider the overall cost of ownership.

Myth Busting: Electric Cars Don't Depreciate Faster

There's a myth out there that electric cars don't depreciate faster than gas-powered cars. But, that's just not true. In fact, electric cars depreciate at a rate of around 50% within the first three years of ownership, compared to around 30% for gas-powered cars.

That's a big difference, and it's all because of the way electric cars are designed. I mean, they're built with specialized technology, like batteries and electric motors, which can be expensive to replace.

But, on the other hand, electric cars also have some advantages when it comes to depreciation. For instance, they tend to have lower maintenance costs, which can help offset the cost of depreciation. And, let's not forget about the cheapest electric cars to insure - they can end up saving you money in the long run.

OK So Here's the Deal With Insurance Companies

Insurance companies are not always transparent about how they calculate premiums. But, one thing is for sure - they take depreciation rates into account.

In fact, some insurance companies, like Allstate, use specialized software to calculate depreciation rates and determine premiums. And, let's be real - it's not always fair. I mean, some cars depreciate faster than others, and that's just the way it is.

But, as a consumer, you have the power to shop around and compare rates. And, if you're looking for the cheapest electric cars to insure, you might want to consider cars like the Hyundai Kona Electric or the Audi e-tron. They're both relatively affordable, with prices starting at around $30,000.

FAQs

#### What's the average depreciation rate for electric cars?

The average depreciation rate for electric cars is around 50% within the first three years of ownership. However, this can vary depending on the make and model of the car, as well as other factors like maintenance costs and insurance premiums.

#### How do insurance companies calculate premiums for electric cars?

Insurance companies use a variety of factors to calculate premiums for electric cars, including depreciation rates, maintenance costs, and the overall cost of ownership. They may also use specialized software to determine premiums.

#### What's the cheapest electric car to insure?

The cheapest electric car to insure is likely to be the Nissan Leaf, with average annual premiums ranging from $1,000 to $1,500. However, this can vary depending on the trim level, options, and other factors.

#### Can I save money on EV insurance by shopping around?

Yes, you can save money on EV insurance by shopping around and comparing rates. In fact, some insurance companies, like Geico and Progressive, offer specialized policies for electric car owners that can end up saving you money in the long run.

#### Do all electric cars depreciate at the same rate?

No, not all electric cars depreciate at the same rate. Some, like the Hyundai Ioniq 5, hold their value pretty well, while others, like the Rivian, depreciate much faster.

#### How can I find the cheapest electric cars to insure?

You can find the cheapest electric cars to insure by researching different models, comparing prices, and shopping around for insurance quotes. You may also want to consider factors like maintenance costs and the overall cost of ownership.

Well, actually, the whole process of finding the cheapest electric cars to insure can be pretty overwhelming. But, with a little research and patience, you can end up saving money in the long run. And, let's be real - who doesn't love saving money?

So, there you have it - the cheapest electric cars to insure, and how to find them. It's not always easy, but it's worth it in the end. Keep those batteries topped up and those premiums low.

— Alex