Buying insurance for a performance EV is kinda like trying to find a needle in a haystack - except the needle is on fire and the haystack is made of money. Sound familiar? You're looking for the cheapest electric cars to insure, but you also want that rush of adrenaline when you hit the gas pedal. Well, buckle up, because we're about to explore how 0-60 times and high horsepower affect your premium.

OK So Here's the Deal With Performance EV Insurance

Performance EVs like the Tesla Model S, with its 2.5 seconds 0-60 time, and the BMW iX, with its 4.6 seconds 0-60 time, are a thrill to drive, but they can also be a thrill to insure. The cost of insurance for these vehicles can range from $2,500 to $5,000 per year, depending on the insurer and the state you live in. For example, a 35-year-old driver in California with a clean record can expect to pay around $3,200 per year for a Tesla Model 3 with a 3.2 seconds 0-60 time, while a Hyundai Ioniq 5 with a 5.2 seconds 0-60 time would cost around $2,500 per year. Know what the kicker is? The insurance companies are gonna charge you more for that 0-60 time, even if you never actually drive that fast. Wild, right?

That being said, some insurers are more lenient than others. For instance, USAA offers competitive rates for military personnel and their families, with premiums starting at around $1,800 per year for a Tesla Model Y with a 3.5 seconds 0-60 time. On the other hand, Geico is known for its affordable rates, but their premiums for performance EVs can be steeper, with a starting price of around $2,800 per year for a Rivian R1T with a 3 seconds 0-60 time. The key is to shop around and compare rates from different insurers to find the best deal.

Busting the Myth: High Horsepower Always Means High Premiums

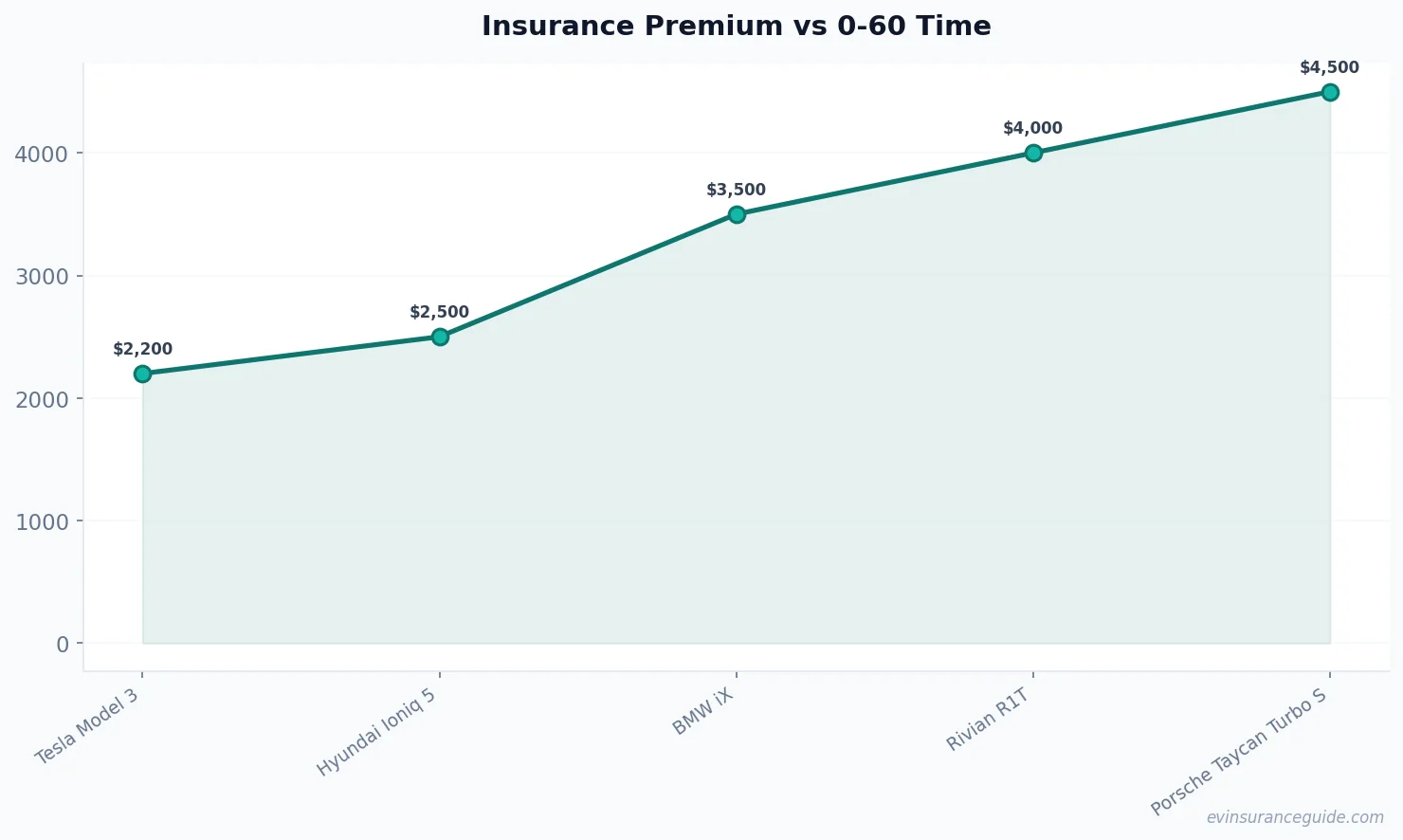

We've all heard the myth that high horsepower EVs are automatically more expensive to insure. But is that really true? Not always. While it's true that high-performance EVs can be more expensive to insure, there are some exceptions to the rule. For example, the Tesla Model 3 Performance, with its 3.2 seconds 0-60 time and 450 horsepower, can be insured for around $2,200 per year with some insurers. That's not much more than the standard Model 3, which has a 5.1 seconds 0-60 time and 258 horsepower. The reason for this is that some insurers consider the overall safety features and driver assistance systems of the vehicle, not just its horsepower.

Of course, there are some cases where high horsepower does mean high premiums. The Porsche Taycan Turbo S, with its 2.4 seconds 0-60 time and 750 horsepower, can cost upwards of $4,500 per year to insure. But that's because it's a high-end sports car, not just an EV. So, the moral of the story is that high horsepower doesn't always mean high premiums, but it can. It really depends on the specific vehicle and the insurer.

A Story of Two EVs: How 0-60 Time Affects Insurance Premiums

I've got a friend, let's call him Dave, who owns a Tesla Model S and a Hyundai Ioniq 5. Both are great cars, but they're worlds apart in terms of performance. The Model S has a 2.5 seconds 0-60 time, while the Ioniq 5 has a 5.2 seconds 0-60 time. Guess which one is cheaper to insure? Yep, you guessed it - the Ioniq 5. Dave pays around $2,000 per year to insure the Ioniq 5, while the Model S costs him around $3,500 per year. That's a significant difference, especially considering that both cars are electric and have similar safety features.

But here's the thing: Dave doesn't really drive that fast. He's a pretty laid-back guy who just wants to get from point A to point B without breaking the bank. So, is it fair that he's paying more for insurance just because his car can go from 0-60 in under 3 seconds? That one stung. I mean, shouldn't the insurance companies be rewarding him for being a safe driver, rather than punishing him for having a fast car? It's all about finding that balance between performance and affordability.

Can You Really Save Money on Insurance by Choosing a Slower EV?

So, let's say you're in the market for a new EV, and you're trying to decide between a few different models. One of them is the Tesla Model 3, which has a 5.1 seconds 0-60 time and a starting price of around $35,000. Another option is the Hyundai Kona Electric, which has a 7.6 seconds 0-60 time and a starting price of around $36,000. Both cars are great options, but they have some key differences. The Model 3 is definitely the more performance-oriented of the two, while the Kona Electric is more focused on practicality and affordability.

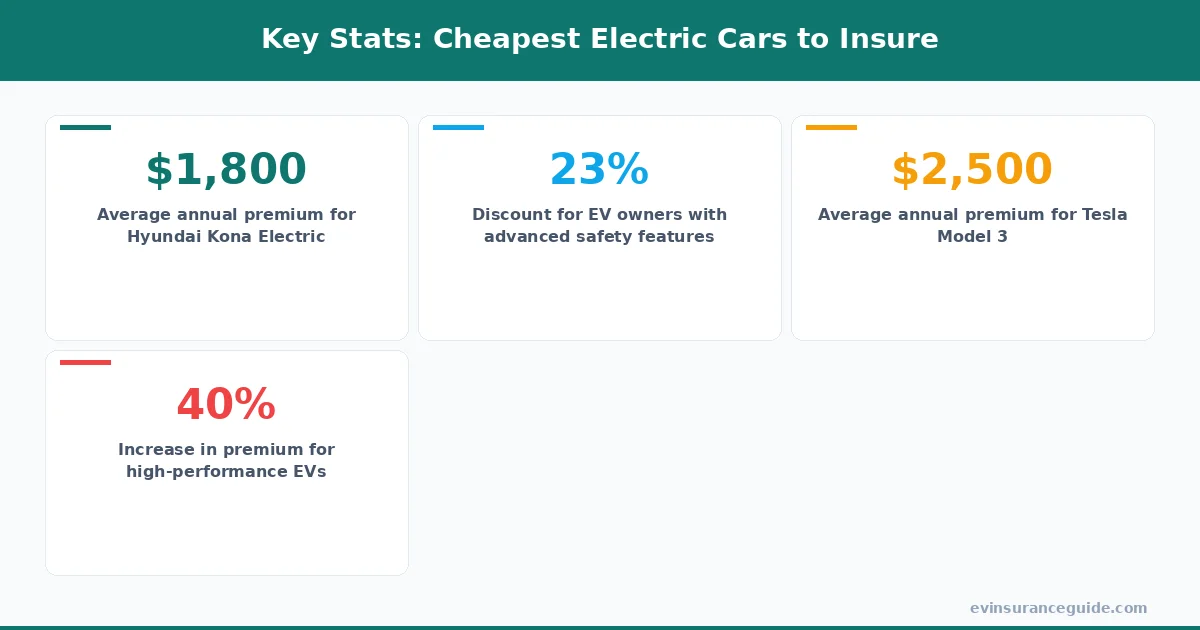

But here's the thing: the Kona Electric is actually one of the cheapest electric cars to insure. With a starting price of around $36,000 and an estimated annual insurance premium of around $1,800, it's a great option for budget-conscious buyers. On the other hand, the Model 3 is a bit pricier to insure, with an estimated annual premium of around $2,200. So, if you're looking to save money on insurance, the Kona Electric might be the way to go.

5 Things to Consider When Insuring Your Performance EV

When it comes to insuring your performance EV, there are a few things to keep in mind. First, make sure you're shopping around and comparing rates from different insurers. This can help you find the best deal and save money on your premium. Second, consider the safety features and driver assistance systems of your vehicle. Insurers often offer discounts for cars with advanced safety features, so it's worth looking into. Third, think about the cost of repairs and replacement parts for your vehicle. If your car is particularly expensive to repair, you may want to consider a higher deductible to lower your premium. Fourth, don't forget to ask about any discounts you may be eligible for, such as a good student discount or a military discount. And finally, make sure you're reading the fine print and understanding what's covered and what's not.

For example, some insurers may offer a discount for EV owners who charge their cars at home, rather than on the go. Others may offer a discount for drivers who have a good driving record and low mileage. It's all about finding the right combination of coverage and affordability for your specific needs and budget.

FAQs

#### What is the cheapest electric car to insure?

The cheapest electric car to insure is often the Hyundai Kona Electric, with an estimated annual insurance premium of around $1,800. However, this can vary depending on the insurer and the state you live in.

#### How does 0-60 time affect insurance premiums?

The 0-60 time of your EV can affect your insurance premiums, with faster cars generally costing more to insure. However, this is not always the case, and some insurers may consider other factors such as safety features and driver assistance systems.

#### Can I save money on insurance by choosing a slower EV?

Yes, choosing a slower EV can potentially save you money on insurance. For example, the Hyundai Kona Electric has a 7.6 seconds 0-60 time and is one of the cheapest electric cars to insure, with an estimated annual premium of around $1,800.

#### What safety features can help lower my insurance premium?

Advanced safety features such as lane departure warning, blind spot detection, and forward collision warning can help lower your insurance premium. Insurers often offer discounts for cars with these features, so it's worth looking into.

#### How do I find the best insurance deal for my performance EV?

To find the best insurance deal for your performance EV, be sure to shop around and compare rates from different insurers. You can also consider working with an insurance broker who specializes in EVs, as they may have access to exclusive discounts and deals.

#### Are there any discounts available for EV owners?

Yes, some insurers offer discounts for EV owners, such as a discount for charging your car at home or a discount for driving a certain number of miles per year. It's worth asking about these discounts when shopping for insurance.

#### What is the average annual insurance premium for a performance EV?

The average annual insurance premium for a performance EV can range from $2,500 to $5,000, depending on the insurer and the state you live in. However, this can vary widely depending on the specific vehicle and the driver's profile.

As a pro tip, it's always a good idea to read the fine print and understand what's covered and what's not. Don't assume that just because you have insurance, you're completely protected - there may be certain exclusions or limitations that apply to your policy.

And remember: the best policy is the one you actually understand.