So, you've finally decided to join the EV revolution, and you're excited to hit the road in your shiny new Tesla Model 3. But, here's the thing - have you thought about insurance? Nope. I didn't think so. It's like nobody wants to talk about the elephant in the room - the crazy-high premiums that come with owning an electric vehicle. I mean, what's the point of saving the planet if you're gonna break the bank on insurance, right? Sound familiar?

Comparing Apples to Oranges - EV Insurance Discounts

When it comes to ev insurance discounts, it's all about comparing the right factors. Take the Tesla Model Y, for example. Its insurance premium can range from $1,200 to $2,500 per year, depending on the insurance provider and your location. Now, compare that to the BMW iX, which can cost anywhere from $1,800 to $3,000 per year to insure. That's a significant difference, especially if you're looking to save some cash on ev insurance discounts. Know what the kicker is? Your credit score plays a huge role in determining these premiums. Wild, right?

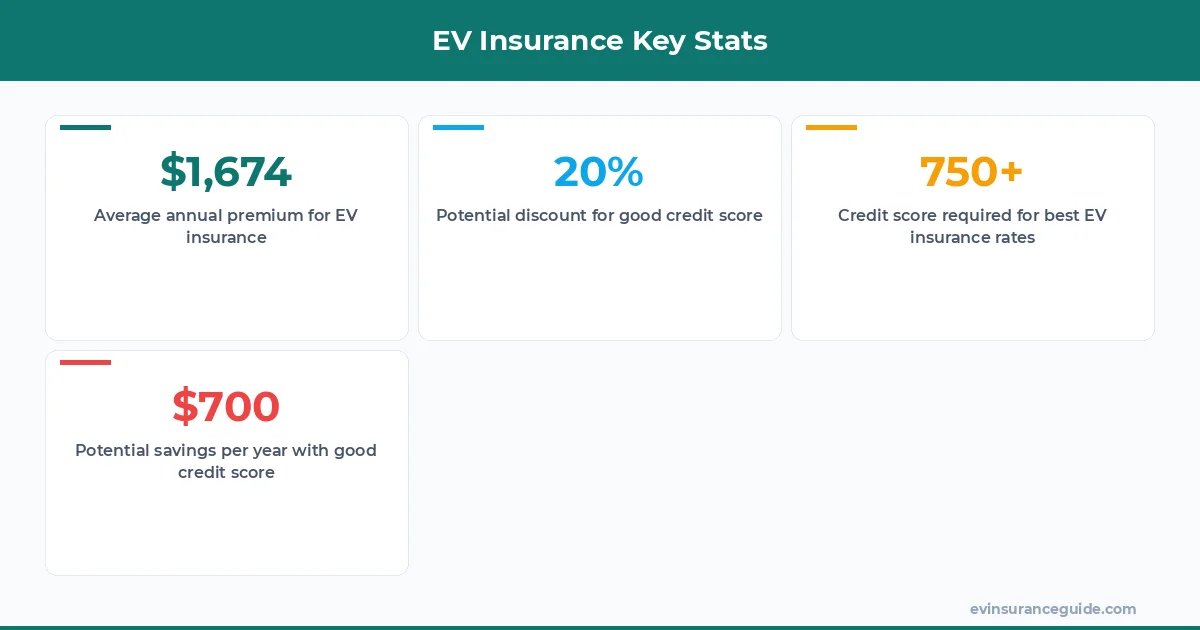

But, here's the thing - not all insurance providers are created equal. Some, like Geico, offer more competitive rates for EV owners with good credit scores. I mean, we're talking up to 20% off the premium price. That's some serious ev insurance discounts right there. On the other hand, companies like State Farm might not be as generous, but they do offer other perks, like 24/7 customer support. So, it's all about weighing your options and finding the best fit for your needs.

And, let's not forget about the Hyundai Ioniq 5 - a game-changer in the EV world. Its insurance premium can range from $1,500 to $2,800 per year, depending on the trim level and your location. Now, I know what you're thinking - what about Rivian? Well, that's a whole different story. Rivian's insurance premiums can be steep, ranging from $2,000 to $4,000 per year. But, hey, if you're willing to pay the price, you'll get an incredible vehicle with some serious tech behind it.

A Story of EV Insurance Woes - Don't Get Caught Out

I've got a friend, let's call him Dave, who recently bought a Tesla Model 3. He was thrilled, until he got his insurance quote - a whopping $2,800 per year. That one stung. He thought he was getting a good deal, but it turned out his credit score was the culprit. He had some late payments on his credit card, which tanked his score and, subsequently, his insurance premium. He ended up switching to a different provider, but not before learning a valuable lesson - check your credit score before applying for EV insurance.

Now, I know some of you might be thinking, 'But, Alex, I've got a great credit score. I'm golden, right?' Well, actually, it's not that simple. Even with a good credit score, you can still get ripped off by insurance companies. That's why it's crucial to shop around, compare rates, and look for ev insurance discounts. Don't be afraid to negotiate, either. You'd be surprised what you can get if you just ask.

Pro tip: Always check your credit report before applying for EV insurance. You can get a free report from the three major credit bureaus - Equifax, Experian, and TransUnion. It's worth the effort, trust me.

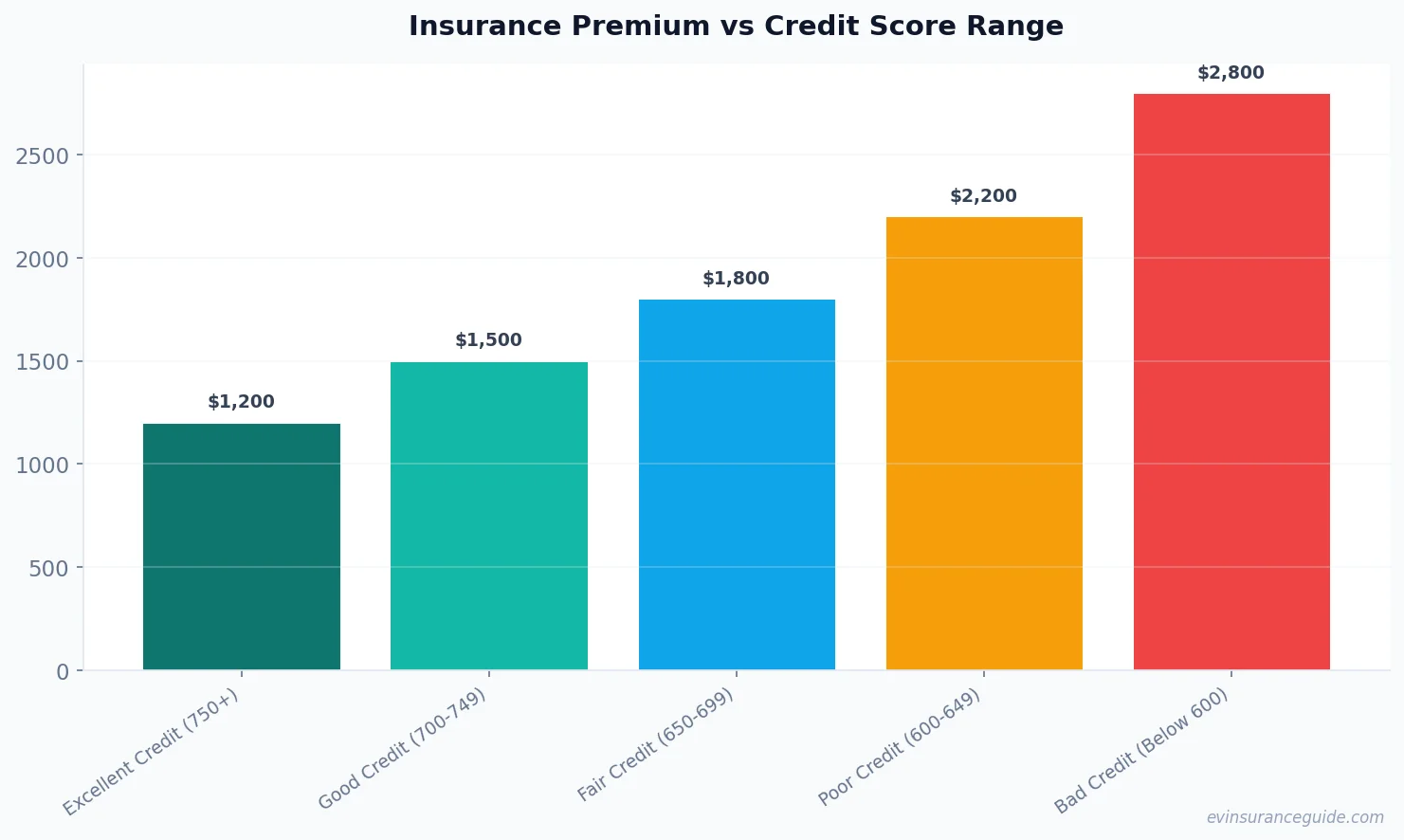

Can Your Credit Score Really Affect EV Insurance Rates?

So, you're probably wondering - how much can my credit score really impact my EV insurance rates? The answer is - a lot. I mean, we're talking hundreds, even thousands of dollars per year. It's crazy, right? But, here's the thing - it's not just about the premium price. A good credit score can also get you better coverage options, like comprehensive and collision insurance.

Take, for example, the case of Sarah, who owns a Hyundai Ioniq 5. She had a credit score of 750, which got her a premium of $1,800 per year. But, after some financial setbacks, her credit score dropped to 650. Suddenly, her premium jumped to $2,500 per year. That's a $700 difference, just because of her credit score. Know what the worst part is? She didn't even realize it was happening until it was too late.

5 Key Factors to Consider When Shopping for EV Insurance

So, you're in the market for EV insurance, and you want to get the best deal possible. Here are 5 key factors to consider:

- 1. Credit score - we've already discussed this one, but it's crucial.

- 2. Vehicle make and model - some EVs are more expensive to insure than others.

- 3. Location - where you live can impact your premium price.

- 4. Driving history - a clean record can get you better rates.

- 5. Coverage options - don't skimp on comprehensive and collision insurance.

And, let's not forget about the cost. I mean, we're talking anywhere from $1,000 to $4,000 per year, depending on the provider and your location. That's why it's essential to shop around, compare rates, and look for ev insurance discounts. Don't be afraid to negotiate, either. You'd be surprised what you can get if you just ask.

OK So Here's the Deal With EV Insurance Discounts

So, you're looking for ev insurance discounts, and you want to know the best way to get them. Well, here's the deal - it's all about your credit score. I mean, if you've got a good credit score, you're golden. You can get up to 20% off your premium price, depending on the provider. But, if you've got a bad credit score, you're in trouble. You'll be paying top dollar for your EV insurance, and that's just not worth it.

But, hey, don't worry. There are ways to improve your credit score, and it's not as hard as you think. Just pay your bills on time, keep your credit utilization low, and avoid late payments. Easy peasy, right? And, if you're looking for ev insurance discounts, just remember - it's all about shopping around and comparing rates. Don't be afraid to negotiate, either. You'd be surprised what you can get if you just ask.

FAQs

#### What is the average cost of EV insurance?

The average cost of EV insurance can range from $1,000 to $4,000 per year, depending on the provider and your location. It's essential to shop around and compare rates to get the best deal possible.

#### How can I improve my credit score to get better EV insurance rates?

To improve your credit score, just pay your bills on time, keep your credit utilization low, and avoid late payments. It's not as hard as you think, and it's worth the effort.

#### What are some common mistakes to avoid when shopping for EV insurance?

Some common mistakes to avoid when shopping for EV insurance include not comparing rates, not checking your credit report, and not negotiating with the provider. Don't be afraid to ask for a better deal - you'd be surprised what you can get.

#### Can I get EV insurance discounts if I have a bad credit score?

Unfortunately, it's not easy to get ev insurance discounts with a bad credit score. But, hey, don't worry. There are ways to improve your credit score, and it's not as hard as you think. Just pay your bills on time, keep your credit utilization low, and avoid late payments.

#### How often should I check my credit report to ensure I'm getting the best EV insurance rates?

You should check your credit report at least once a year to ensure you're getting the best EV insurance rates. It's essential to catch any errors or discrepancies that could be impacting your credit score.

#### What are some tips for negotiating with EV insurance providers?

When negotiating with EV insurance providers, just remember - it's all about being confident and persistent. Don't be afraid to ask for a better deal, and be willing to walk away if you don't get what you want.

#### Are there any specific EV insurance providers that offer better rates for EV owners with good credit scores?

Yes, there are several EV insurance providers that offer better rates for EV owners with good credit scores. Some examples include Geico, Progressive, and USAA. Just remember to shop around and compare rates to get the best deal possible.

Keep those batteries topped up and those premiums low. — Alex