Do you need special EV insurance or is that just another upsell story insurers love to tell? Plenty of drivers assume their Tesla Model 3 or Hyundai Ioniq 5 needs some exotic policy, yet standard auto coverage from GEICO or State Farm already protects most EVs without drama. The real question is which extras actually save money when a battery fails or a charger gets fried.

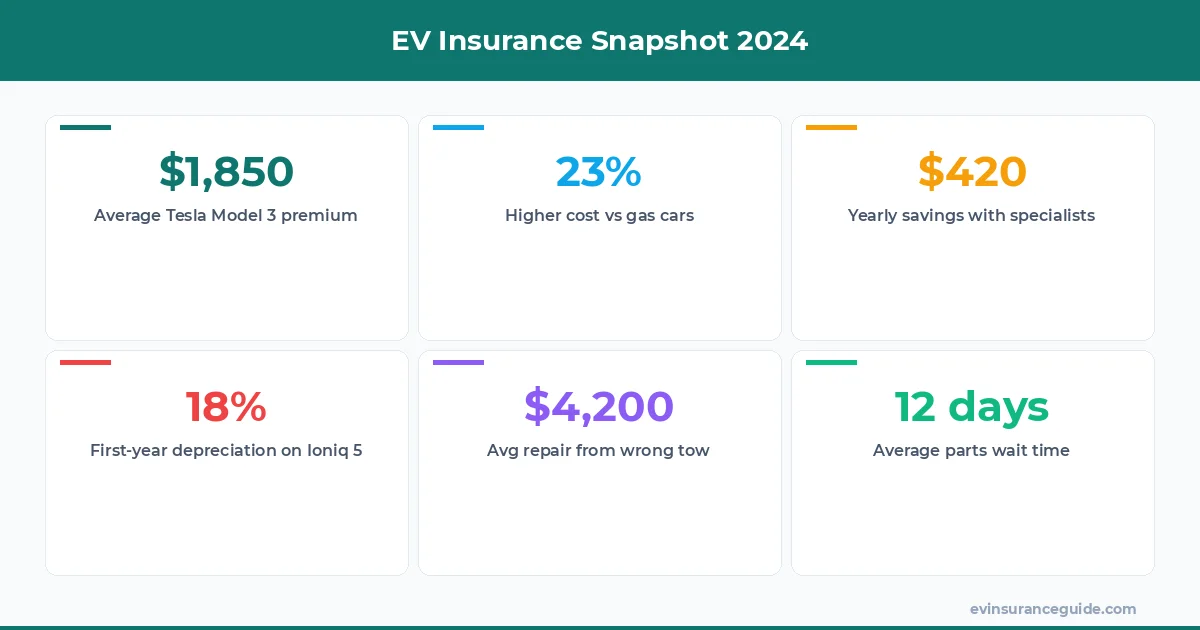

Battery replacement on a BMW iX can run $20,000 plus labor. Standard policies cap that at original cost minus depreciation, leaving you exposed. Roadside assistance often sends a tow truck that drags the car on its wheels, which voids warranties on many electric models. Those gaps explain why some owners pay $1,850 a year while others drop to $1,420 with the right tweaks.

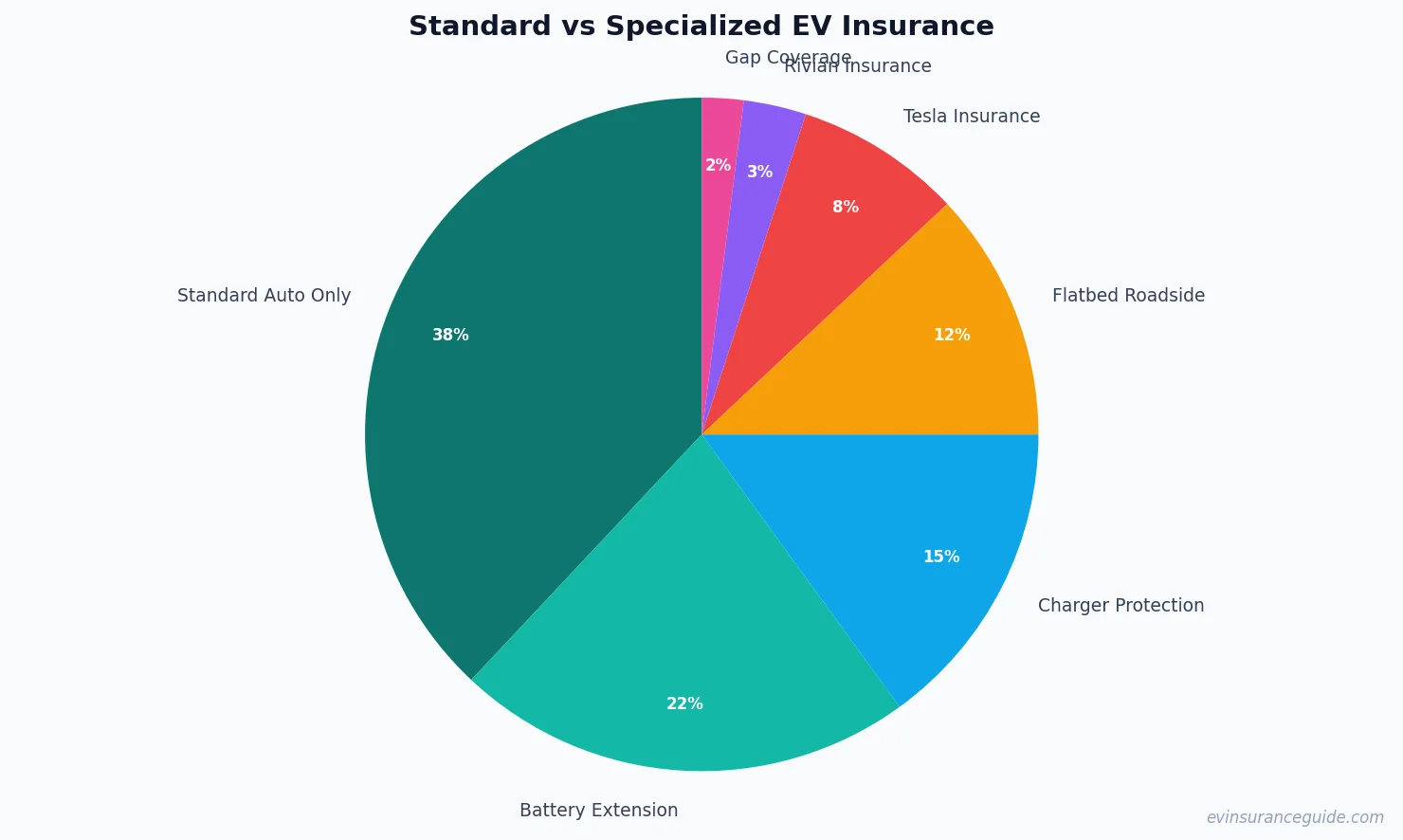

Know what the kicker is? Most people over-insure and still miss the exact protections EVs demand. A quick policy review usually shows you only need three targeted add-ons instead of a full specialized plan. Sound familiar?

5 Add-Ons Worth Every Penny for Your EV Battery coverage extension tops the list. It extends replacement protection beyond the factory 8-year limit for roughly $180 extra per year on a Tesla Model Y. Without it you risk a $15,000 surprise after year nine. GEICO offers this as a rider and most drivers recover the premium after one claim.

Charging equipment coverage protects your home wall box against surges or theft. A $1,200 Level 2 charger plus installation runs $2,400 total. This add-on costs about $90 annually yet pays for itself fast if lightning hits. State Farm bundles it with home policies but stands alone on auto for $75.

Roadside assistance with flatbed towing is non-negotiable. Standard plans send dollies that damage the battery tray on a Rivian R1T. The EV-specific version costs $120 a year and guarantees a flatbed every time. One call after a dead 12-volt battery proved the difference.

Gap coverage still matters even with EVs holding value better than gas cars. A new Hyundai Ioniq 5 loses 18 percent in the first year. Adding this rider for $110 closes the loan gap if totaled early. Rental car reimbursement at $40 daily covers the wait for parts that now average 22 days on backorder.

Is paying for all five overkill? Usually. Start with the first three and reassess after one renewal. That approach keeps premiums realistic while covering the real risks.

Honestly, Tesla Insurance Beats Most Traditional Options Traditional carriers like State Farm still treat EVs like regular sedans and charge 23 percent more on average. Their adjusters rarely understand battery degradation or high-voltage repairs, so claims drag on for weeks. Tesla Insurance, by contrast, pulls real-time driving data from the car and rewards safe habits with discounts up to 40 percent.

Rivian Insurance follows the same model and undercuts GEICO by $400 a year on a new R1S for qualified drivers. The catch is availability. Tesla Insurance only operates in 12 states so far. Outside those zones you are stuck negotiating with legacy companies that have not updated their rate tables since 2019.

Still, even Tesla Insurance can overprice if your credit score sits below 680. Shop both sides before locking in. The difference between the best and worst quote on the same Model 3 often hits $900 annually. That gap alone justifies one afternoon of phone calls.

What Happened When My Buddy Insured His Rivian My buddy Mike bought a Rivian R1T last spring and went straight to his longtime State Farm agent. The quote came back at $2,650 a year with basic roadside. He added the flatbed rider and battery extension for another $310. Total felt reasonable until a month later when a tree limb took out his home charger.

The claim process exposed gaps he never saw coming. State Farm covered the charger but fought the $3,800 battery preconditioning module replacement for six weeks. Mike switched to Rivian Insurance at renewal and dropped to $1,980 with better roadside terms. The story spread through our group chat and three other owners followed his move.

That single switch highlighted how quickly standard policies reveal their limits on newer platforms. The lesson stuck: test both worlds instead of assuming your current agent already knows the EV playbook.

Watch Out for This Hidden Towing Cost Trap Many drivers discover too late that standard roadside sends a regular tow truck. Dragging an EV on its drive wheels can fry the motors and void the powertrain warranty. Repair bills start at $4,200 and insurers often label it owner negligence. The fix is confirming flatbed language in writing before you sign.

Some policies advertise EV towing yet cap mileage at 15 miles. Beyond that you pay $3.50 per mile out of pocket. On a 40-mile tow after a highway breakdown that adds $140 fast. Always read the actual endorsement, not the marketing bullet.

Do you need special EV insurance just to avoid this one trap? No. You simply need the right rider added to a standard policy. Skip that step and you are gambling with your battery warranty.

Is Tesla Insurance Right for Your Model Y? Tesla Insurance shines for drivers who average under 12,000 miles and maintain safety scores above 95. The savings can reach $600 yearly versus GEICO on a Model Y Long Range. Yet the program still excludes multi-car households in several states and penalizes any at-fault claim harder than legacy carriers.

Compare apples to apples. Pull quotes from Tesla, Rivian, State Farm, and Progressive on the exact same vehicle and driving record. The spread on a 2024 Model 3 Performance reached $1,100 between the cheapest and most expensive option last quarter. That data point alone shows why shopping beats guessing.

Rhetorical questions aside, the math favors testing Tesla Insurance first if you qualify. Just keep a backup quote ready because one bad score update can erase the entire discount overnight.

Pro tip: Always request flatbed language in writing and compare at least three EV-specific quotes before renewing. One overlooked towing clause has cost owners more than the entire premium difference.

How much more does standard insurance cost for a Tesla Model 3? Expect $300 to $700 extra per year compared with a similar gas sedan. State Farm and GEICO both showed this gap on 2023 renewals. The difference shrinks once you add battery and charger riders.

Does Rivian Insurance cover older Tesla models? No, Rivian Insurance stays limited to Rivian vehicles for now. Tesla owners must choose Tesla Insurance or traditional carriers. Switching platforms requires a fresh quote every time.

Can I keep my current agent if I buy a Hyundai Ioniq 5? Yes, but insist on the EV add-on package. Agents unfamiliar with high-voltage systems often leave gaps. One client paid $2,100 before adding the right coverage and dropped to $1,650 after.

What happens if my home charger gets stolen? Standard auto policies treat it as personal property under homeowners. Add the $90 charger rider to close the loophole. Claims under $2,500 process in under 10 days with the rider attached.

Is roadside assistance with flatbed worth $120 yearly? Absolutely for any vehicle over 4,000 pounds. BMW iX and Rivian examples show regular tows create $4,000-plus repair bills. The rider prevents that exposure and keeps warranties intact.

Do you need special EV insurance after a total loss? Gap coverage on a standard policy closes most of the loan difference. Specialized plans add faster payout but rarely justify the extra cost unless your credit is thin.

Shop both traditional and EV-only insurers every renewal. The right mix of standard coverage plus three add-ons keeps costs realistic without the hype. Do you need special EV insurance? Usually not, yet ignoring the targeted riders can sting when the battery or charger fails.

Stay charged and stay covered! — Alex