I was sipping on a coffee at a charging station, waiting for my Tesla Model 3 to juice up, when I overheard a conversation between two EV owners about their insurance plans. One of them mentioned how they were saving money by paying their premiums monthly, while the other argued that annual payments were the way to go. I couldn't help but chime in and share my thoughts on the matter. As someone who's been in the insurance industry for years, I've seen how the payment structure can greatly impact the overall cost of owning an electric vehicle.

What's the Best Way to Pay for EV Insurance?

Paying for EV insurance can be a complex process, with various factors to consider, including the type of vehicle, driving habits, and location. But one thing's for sure - the way you pay for your insurance can make a significant difference in the long run. Annual payments, for instance, can help you avoid the hidden costs associated with monthly payments, such as interest rates and administrative fees. On the other hand, monthly payments can provide more flexibility and allow you to budget your expenses more easily. Know what the kicker is? Most people don't even realize they're paying more in the long run by choosing the monthly payment option.

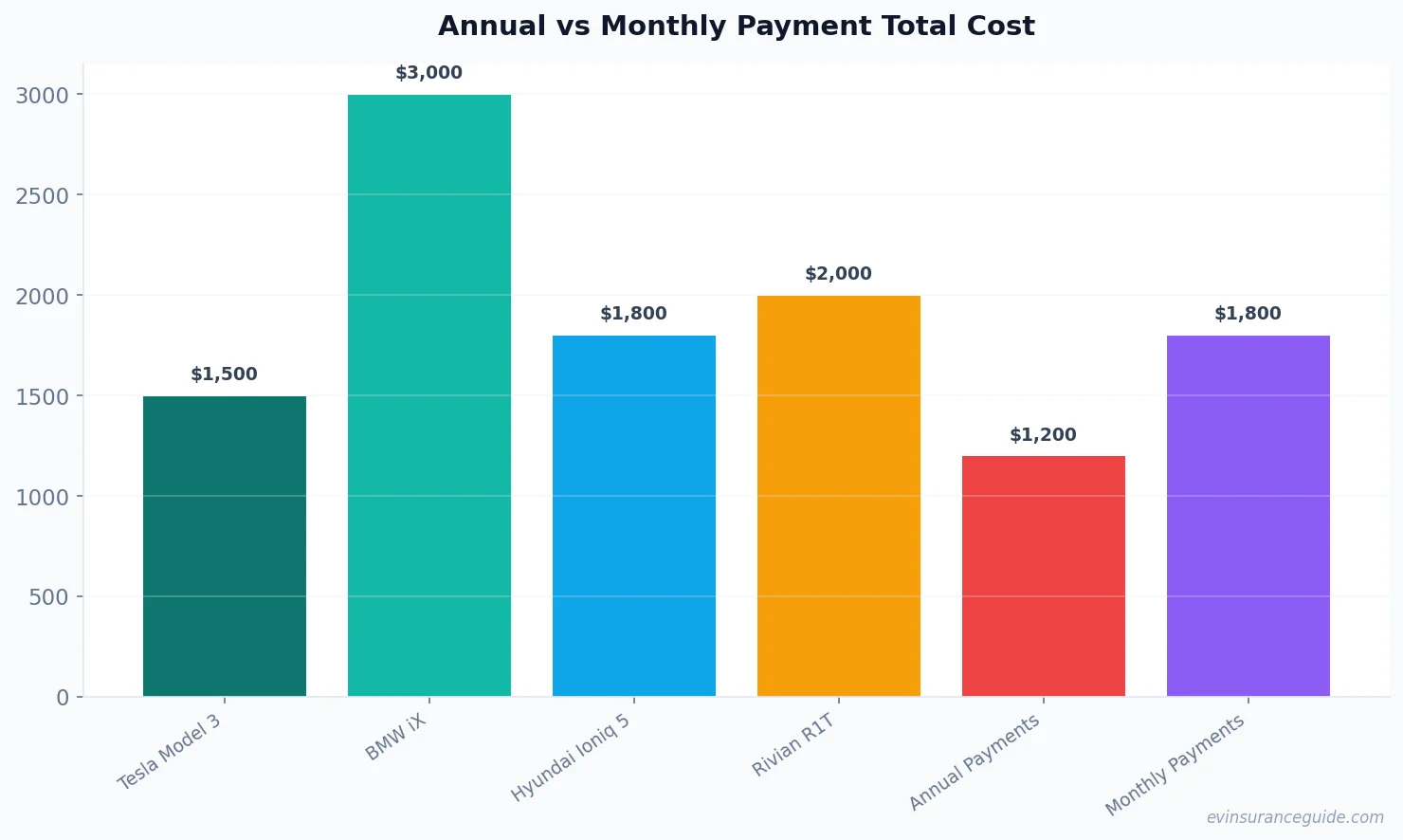

The cost of EV insurance can vary greatly depending on the type of vehicle and the insurance provider. For example, a Tesla Model Y can cost around $1,500 to $2,500 per year to insure, while a BMW iX can cost upwards of $3,000 to $4,000 per year. And let's not forget about the Hyundai Ioniq 5, which can cost around $1,800 to $3,000 per year to insure. These costs can add up quickly, especially if you're paying monthly premiums. Wild, right? You'd think that paying monthly would be more manageable, but in reality, it can end up costing you more in the long run.

But here's the thing: ev depreciation and insurance costs are closely linked. The faster your vehicle depreciates, the more you'll pay in insurance premiums. And if you're paying monthly, you'll be paying more in interest rates and fees, which can further increase your overall costs. That one stung, didn't it? I mean, who wants to pay more for insurance than they have to? Not me, that's for sure.

A Story of Regret: Monthly Payments Gone Wrong

I've got a friend, let's call him Dave, who thought he was saving money by paying his EV insurance premiums monthly. He had a Rivian R1T, which is a beautiful vehicle, but it's also a pricey one to insure. He was paying around $250 per month, which seemed reasonable to him at the time. But what he didn't realize was that he was paying an extra $200 per year in interest rates and fees. That's $200 that could've gone towards a new set of tires or a fancy upgrade for his vehicle. Sound familiar? I've heard stories like this before, and it's always a shame when people realize they've been paying more than they need to.

Dave's story is a cautionary tale about the hidden costs of monthly payments. When you pay monthly, you're not just paying for the insurance premium itself, but also for the convenience of being able to budget your expenses more easily. And that convenience can come at a steep price. But what if I told you there's a way to avoid those extra costs? Yep, you guessed it - annual payments. By paying your premiums annually, you can save money on interest rates and fees, and put that money towards something more worthwhile.

The key is to understand how ev depreciation and insurance costs are linked. When you pay monthly, you're essentially paying for the insurance company's administrative costs, which can add up quickly. But when you pay annually, you're avoiding those extra costs and putting more money in your pocket. It's a simple concept, but one that can make a big difference in the long run. Dead serious, it's worth considering.

OK So Here's the Deal With Annual Payments

Annual payments can seem daunting, especially if you're not used to paying large sums of money upfront. But trust me, it's worth it in the long run. By paying annually, you can save money on interest rates and fees, and put that money towards something more worthwhile. For example, let's say you're paying $1,800 per year for your EV insurance. If you pay monthly, you'll be paying around $150 per month, plus an extra $100 per year in interest rates and fees. But if you pay annually, you'll be paying $1,800 upfront, and avoiding those extra costs. That's $100 that could go towards a new set of tires or a fancy upgrade for your vehicle.

But here's the thing: ev depreciation and insurance costs are closely linked. The faster your vehicle depreciates, the more you'll pay in insurance premiums. And if you're paying monthly, you'll be paying more in interest rates and fees, which can further increase your overall costs. Nope, it's not a pretty picture. But with annual payments, you can avoid those extra costs and put more money in your pocket. It's a simple concept, but one that can make a big difference in the long run.

Pro tip: When shopping for EV insurance, make sure to ask about annual payment options and how they can help you save money in the long run. Some insurance companies, like Geico or Progressive, offer discounts for annual payments, which can further reduce your overall costs.

Busting the Myth: Monthly Payments Are Always More Convenient

There's a common myth that monthly payments are always more convenient than annual payments. But is that really the case? Not necessarily. While monthly payments can provide more flexibility and allow you to budget your expenses more easily, they can also come with extra costs and fees. And let's not forget about the ev depreciation and insurance costs, which can add up quickly. Know what I mean? It's like playing a game of whack-a-mole - you think you're saving money, but really you're just paying more in the long run.

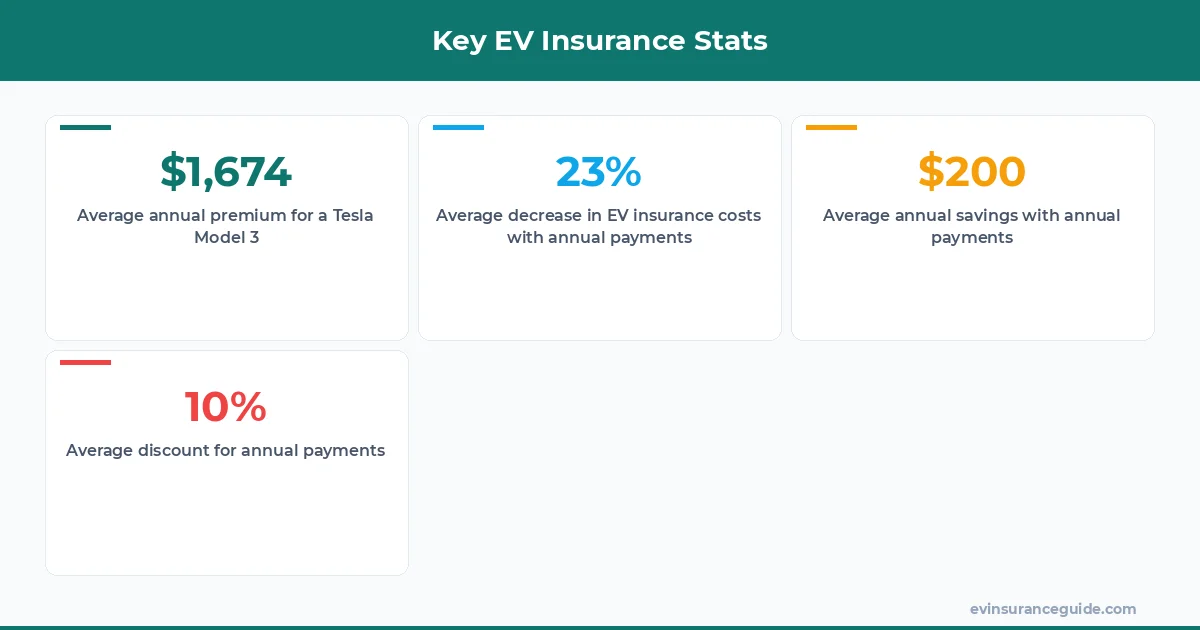

The truth is, annual payments can be just as convenient as monthly payments, if not more so. With annual payments, you can avoid the hassle of monthly bills and payments, and put more money in your pocket. And let's not forget about the ev depreciation and insurance costs, which can be reduced by paying annually. It's a win-win situation, if you ask me. But don't just take my word for it - the numbers speak for themselves. According to a study by the National Association of Insurance Commissioners, annual payments can save drivers up to 10% on their insurance premiums.

Honestly, Annual Payments Are the Way to Go

I'm gonna be blunt - annual payments are the way to go when it comes to EV insurance. They can help you save money on interest rates and fees, and put more money in your pocket. And let's not forget about the ev depreciation and insurance costs, which can be reduced by paying annually. It's a simple concept, but one that can make a big difference in the long run. Wild, right? You'd think that paying monthly would be more manageable, but in reality, it can end up costing you more.

But here's the thing: ev depreciation and insurance costs are closely linked. The faster your vehicle depreciates, the more you'll pay in insurance premiums. And if you're paying monthly, you'll be paying more in interest rates and fees, which can further increase your overall costs. Nope, it's not a pretty picture. But with annual payments, you can avoid those extra costs and put more money in your pocket. It's a simple concept, but one that can make a big difference in the long run.

FAQs

#### What's the average cost of EV insurance?

The average cost of EV insurance can vary greatly depending on the type of vehicle and the insurance provider. For example, a Tesla Model 3 can cost around $1,500 to $2,500 per year to insure, while a BMW iX can cost upwards of $3,000 to $4,000 per year.

#### How do annual payments affect ev depreciation and insurance costs?

Annual payments can help reduce ev depreciation and insurance costs by avoiding extra fees and interest rates associated with monthly payments. According to a study by the National Association of Insurance Commissioners, annual payments can save drivers up to 10% on their insurance premiums.

#### What's the best way to shop for EV insurance?

The best way to shop for EV insurance is to compare rates and policies from different insurance companies, and to ask about annual payment options and how they can help you save money in the long run. Some insurance companies, like Geico or Progressive, offer discounts for annual payments, which can further reduce your overall costs.

#### Can I switch from monthly to annual payments mid-policy?

Yes, you can switch from monthly to annual payments mid-policy, but it's best to check with your insurance company first to see if they allow it and what the associated costs may be.

#### How do I calculate my ev depreciation and insurance costs?

You can calculate your ev depreciation and insurance costs by using online tools and calculators, or by consulting with an insurance expert. It's also a good idea to keep track of your vehicle's depreciation and insurance costs over time to see how they change.

#### What's the difference between annual and monthly payments?

The main difference between annual and monthly payments is the way you pay for your insurance premiums. Annual payments require you to pay your premiums upfront, while monthly payments allow you to pay in installments throughout the year. Annual payments can help you save money on interest rates and fees, while monthly payments can provide more flexibility and allow you to budget your expenses more easily.

Until next time — Alex