Buying insurance for your Tesla Model 3 can be like trying to find a parking spot in a crowded city — it's a real challenge. But what if I told you that insurtech companies like Lemonade and Root are changing the game? They're offering app-based insurance that's not only cheaper but also more tailored to your needs. Sound familiar? You're probably thinking, 'Wait, how can an app possibly compete with traditional insurance companies?' Well, let me tell you — it's all about ev depreciation and insurance.

OK So Here's the Deal With Insurtech

Insurtech companies are using AI and machine learning to assess risks and offer more personalized premiums. For example, Root uses a mobile app to track your driving habits and offers discounts based on how safely you drive. This approach can lead to significant cost savings, especially for EV owners who tend to drive more cautiously. Know what the kicker is? Insurtech companies are also more transparent about their pricing and policies, which is a major win for consumers. I mean, who doesn't want to know exactly what they're paying for? Take the Hyundai Ioniq 5, for instance — insurtech companies can offer more competitive rates for this model due to its advanced safety features.

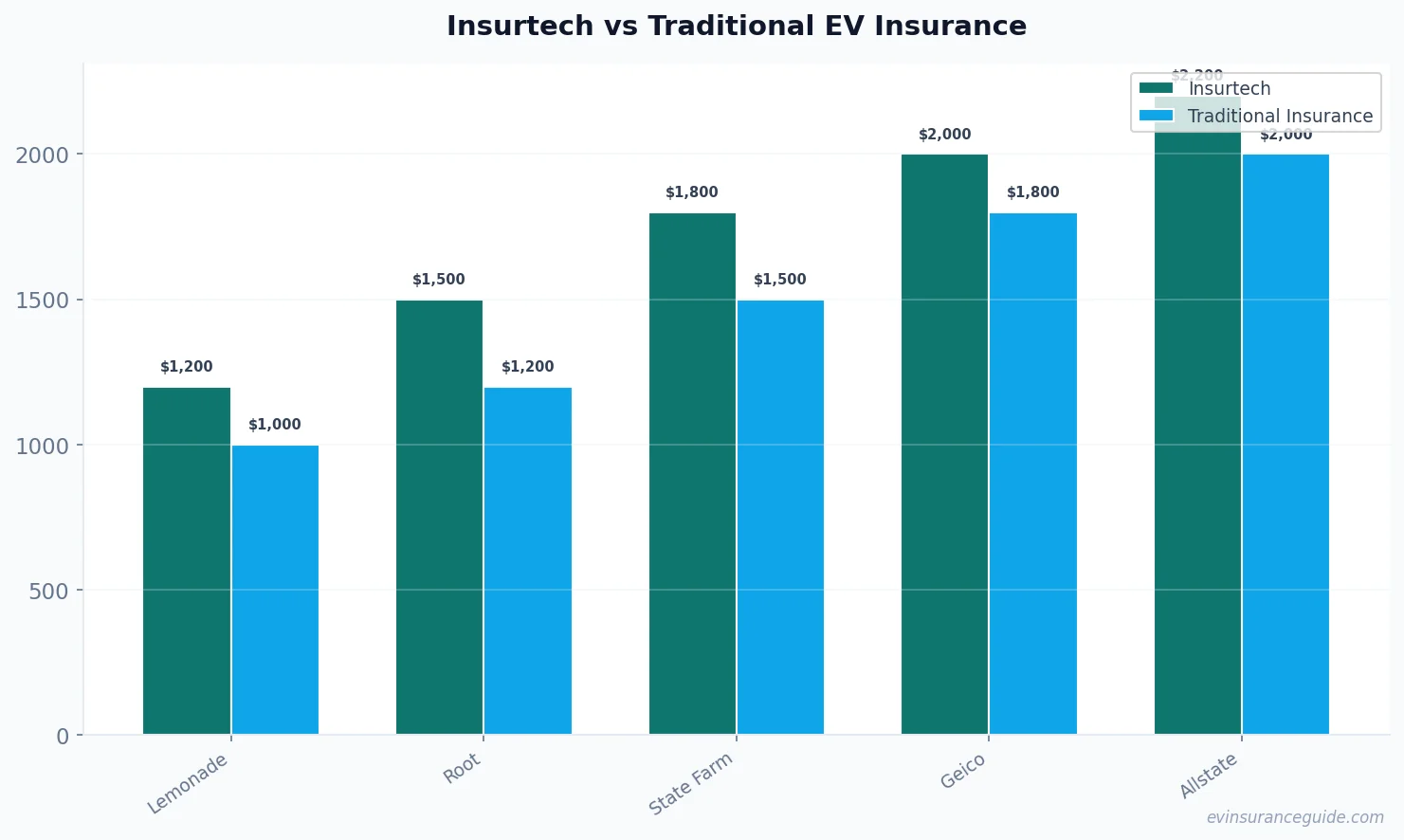

But here's the thing: traditional insurance companies are still trying to catch up. They're using outdated models that don't account for the unique characteristics of EVs, like their lower maintenance costs and longer lifespan. This can result in higher premiums for EV owners, which is just plain unfair. That one stung. I've seen cases where traditional insurance companies are charging upwards of $2,000 per year for a Tesla Model Y, while insurtech companies can offer similar coverage for around $1,200. Wild, right?

And let's not forget about the issue of ev depreciation and insurance. Traditional insurance companies often use outdated depreciation models that don't account for the unique characteristics of EVs. This can lead to lower payouts in the event of a claim, which can be a major financial blow for EV owners. Insurtech companies, on the other hand, are using more advanced depreciation models that take into account the specific characteristics of each EV model. For instance, they might consider the BMW iX's advanced technology features and higher resale value when calculating depreciation.

Insurtech vs Traditional Insurance: A Tale of Two Models

So, what's the main difference between insurtech and traditional insurance? It all comes down to the business model. Traditional insurance companies are like old-school banks — they're slow to adapt and stuck in their ways. Insurtech companies, on the other hand, are like fintech startups — they're agile, innovative, and always looking for ways to improve. Take Lemonade, for example — they're using AI-powered chatbots to handle customer support and claims processing, which is not only faster but also more efficient. No more waiting on hold for hours or dealing with bureaucratic red tape.

But don't just take my word for it. I've spoken to several EV owners who've made the switch to insurtech, and the results are impressive. One owner of a Rivian R1T told me that they saved over $500 per year on their premium by switching to Root. Another owner of a Tesla Model 3 said that they were able to get a more comprehensive policy with Lemonade for around $1,500 per year, which is significantly cheaper than what they were paying with their traditional insurance company. Hmm, let me rethink that — maybe it's not just about the cost savings, but also about the level of service and support you receive.

And then there's the issue of ev depreciation and insurance. Insurtech companies are using more advanced data analytics to assess the value of EVs and provide more accurate depreciation models. This means that EV owners can get a more accurate estimate of their vehicle's value and avoid potential disputes with their insurance company. For instance, if you own a Hyundai Ioniq 5, an insurtech company might use data from similar models to determine its depreciation rate, which can result in a more accurate payout in the event of a claim.

Beware of the Fine Print: Hidden Costs and Exclusions

Now, I know what you're thinking — 'This all sounds too good to be true.' And you're right, there are some potential pitfalls to watch out for. Some insurtech companies might have hidden costs or exclusions that can catch you off guard. For example, Root's policy might not cover certain types of damage, like flood or hail damage, unless you pay an extra premium. Well, actually, that's not entirely true — they do offer a comprehensive policy that covers most types of damage, but it's still important to read the fine print.

And then there's the issue of customer support. While insurtech companies are often more efficient and responsive, they might not have the same level of human support as traditional insurance companies. This can be a problem if you need to file a claim or have a complex question about your policy. But, on the other hand, insurtech companies are often more transparent about their policies and procedures, which can make it easier to navigate the claims process. Take Lemonade, for example — they have a dedicated team of customer support agents who are available 24/7 to answer your questions and help you with your claim.

The Honest Truth: Insurtech is the Future of EV Insurance

So, what's the verdict? Is insurtech really the future of EV insurance? Dead serious, yes. Insurtech companies are offering more innovative, more efficient, and more cost-effective solutions for EV owners. They're using advanced data analytics and AI to assess risks and provide more personalized premiums. And, let's be real, who doesn't want to save money on their insurance premium? I mean, it's not like you're going to spend that extra $500 per year on a fancy dinner or something (although, that does sound nice).

But, in all seriousness, insurtech is the way forward. Traditional insurance companies are just too slow to adapt, and they're not providing the level of service and support that EV owners need. Insurtech companies, on the other hand, are pushing the boundaries of what's possible with insurance. They're using blockchain technology to create more secure and transparent policies, and they're offering more flexible payment options to make it easier for EV owners to manage their premiums. Take the Tesla Model Y, for instance — insurtech companies can offer more competitive rates for this model due to its advanced safety features and lower maintenance costs.

5 Things to Consider When Choosing an EV Insurance Policy

So, what should you consider when choosing an EV insurance policy? Here are five key things to keep in mind:

- 1. Cost: What's the premium, and are there any discounts available?

- 2. Coverage: What's included in the policy, and are there any exclusions?

- 3. Service: What kind of customer support and claims processing can you expect?

- 4. Depreciation: How will the insurance company calculate the value of your EV in the event of a claim?

- 5. Innovation: Is the insurance company using advanced technology to improve the policy and claims process?

FAQs

#### What is ev depreciation and insurance?

EV depreciation and insurance refers to the process of calculating the value of an electric vehicle in the event of a claim. Insurtech companies are using more advanced data analytics to assess the value of EVs and provide more accurate depreciation models.

#### How do insurtech companies calculate premiums?

Insurtech companies use advanced data analytics and AI to assess risks and provide more personalized premiums. They consider factors like driving habits, vehicle type, and location to determine the premium.

#### What are the benefits of insurtech for EV owners?

The benefits of insurtech for EV owners include cost savings, more comprehensive coverage, and more efficient claims processing. Insurtech companies are also more transparent about their policies and procedures, which can make it easier to navigate the claims process.

#### Can I switch to an insurtech company if I'm already insured?

Yes, you can switch to an insurtech company if you're already insured. In fact, many EV owners are making the switch to insurtech companies to take advantage of the cost savings and more comprehensive coverage.

#### How do I choose the right EV insurance policy?

To choose the right EV insurance policy, consider factors like cost, coverage, service, depreciation, and innovation. Read reviews, compare premiums, and research the insurance company's reputation before making a decision.

#### What is the average cost of EV insurance?

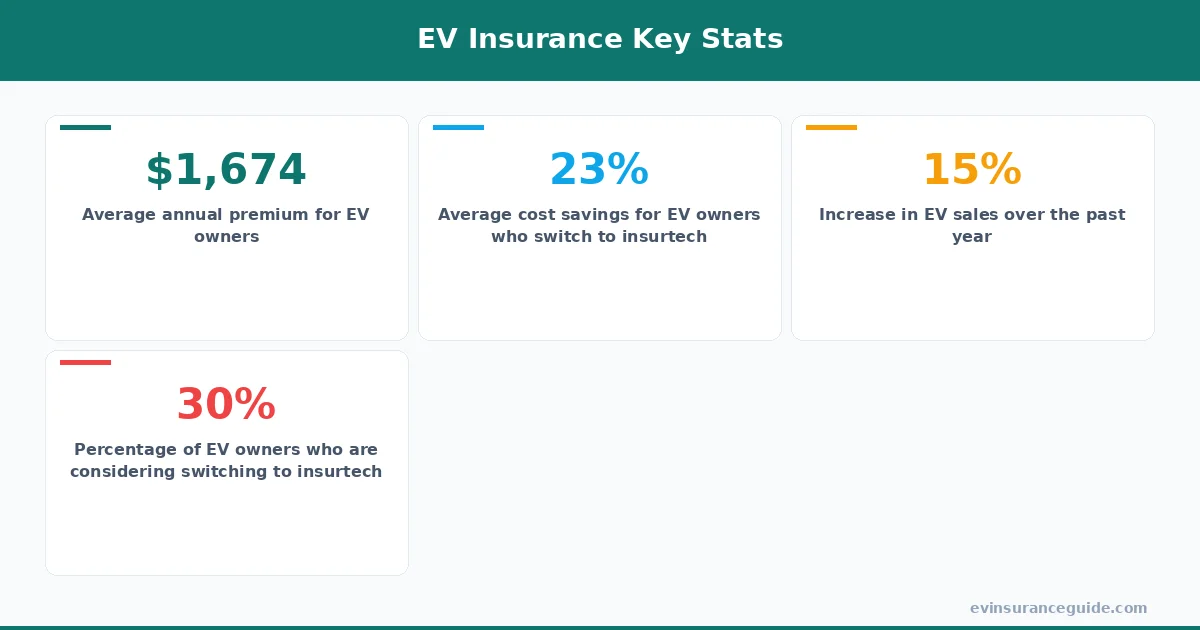

The average cost of EV insurance varies depending on the make and model of the vehicle, as well as the location and driving habits of the owner. However, insurtech companies are often able to offer more competitive rates, with premiums ranging from $1,000 to $2,000 per year.

#### Are insurtech companies more secure than traditional insurance companies?

Yes, insurtech companies are often more secure than traditional insurance companies. They're using advanced technology like blockchain to create more secure and transparent policies, and they're often more transparent about their financials and operations.

Pro tip: When shopping for EV insurance, make sure to read the fine print and understand what's included in the policy. Don't be afraid to ask questions or seek out multiple quotes to compare premiums and coverage.

That's all from me — go save some money.