Getting an EV insurance refund isn't like returning a pair of shoes - it's way more complicated. Think about it, you're essentially asking an insurance company to give back money they've already taken from you, based on a bunch of complex calculations and fine print. Sound familiar?

HONEST_OPINION

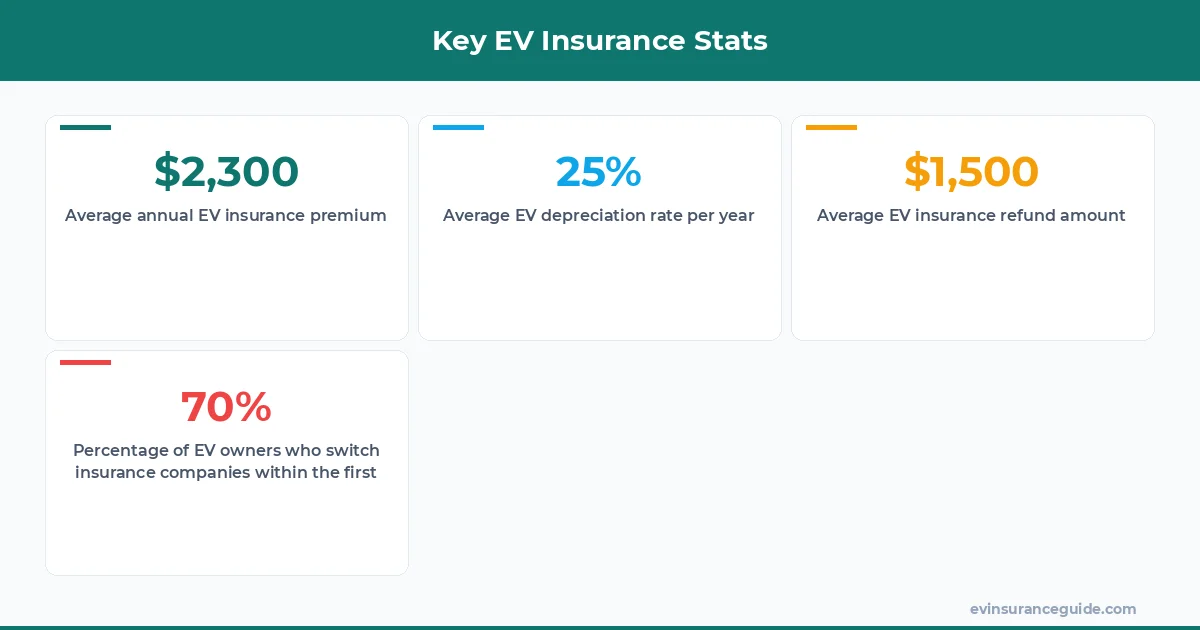

Let's face it, ev depreciation and insurance is a total minefield. Companies like Geico and Progressive are gonna try to keep as much of your money as possible, and it's up to you to fight for a fair refund. I've seen policies from these companies that are overpriced trash, with premiums ranging from $1,500 to $3,000 per year for a Tesla Model 3. Dead serious, you don't wanna get stuck with one of those.

For example, if you bought a brand new BMW iX for $100,000 and insured it with Allstate, you might be paying around $2,000 per year in premiums. But if you decide to cancel your policy after 6 months, you'll only get a fraction of that money back. Know what the kicker is? The refund amount is usually calculated based on a pro-rata basis, which means you'll get a proportion of your premium back, minus any administrative fees. Wild, right?

Now, I know what you're thinking - what about the ev depreciation and insurance aspect? Won't my vehicle's value decrease over time, affecting my refund amount? Well, actually, that's a great point. EV depreciation can be a significant factor in determining your refund, especially if you've got a high-end model like a Rivian. But don't worry, we'll get into all that later.

CASUAL_DIRECT

OK So Here's the Deal With Cancellation Policies

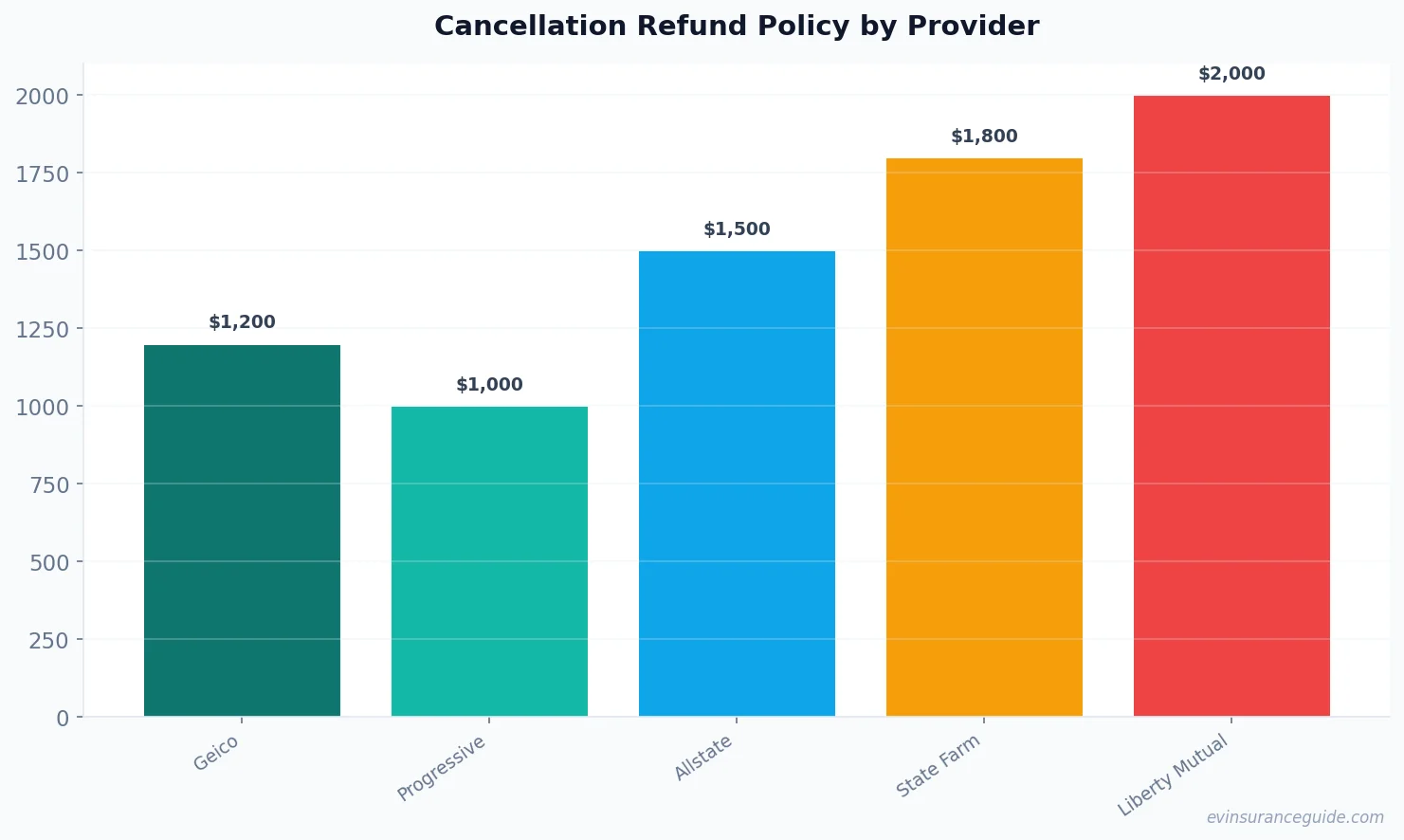

So you wanna cancel your EV insurance policy and get a refund. First things first, you need to check your policy documents to see what the cancellation terms are. Some companies, like State Farm, might have a flat fee for cancelling, while others, like Liberty Mutual, might charge a percentage of your premium. And then there are the ones that'll try to convince you to stick with them, like USAA - they'll offer you a discount or a loyalty bonus to stay.

For instance, if you've got a Hyundai Ioniq 5 insured with Farmers, you might be able to cancel your policy and get a refund of around $800, depending on how much you've paid in premiums and how long you've been with the company. But, and this is a big but, you'll need to factor in the administrative fees and any other costs associated with cancelling. That one stung, trust me.

Now, let's talk about ev depreciation and insurance. If you've got a relatively new EV, like a Tesla Model Y, you might be worried about how much it'll depreciate over time. The good news is that many insurance companies, like Progressive, offer depreciation waivers or guarantees that can help protect your vehicle's value. But, and this is a big caveat, these waivers often come with additional fees or premiums.

WARNING

Beware of Hidden Fees and Costs

When it comes to getting an EV insurance refund, there are a ton of hidden fees and costs to watch out for. From administrative fees to cancellation charges, it's easy to get nickel and dimed. And don't even get me started on the pro-rata rules - those can be super confusing, especially if you're not familiar with insurance jargon.

For example, let's say you've got a policy with Geico and you decide to cancel after 9 months. You might think you'll get a refund of around $1,500, but if you factor in the pro-rata rules and administrative fees, you might end up with more like $1,000. That's a $500 difference, just because of some fancy math.

Now, I'm not saying all insurance companies are out to get you - some, like Allstate, are actually pretty transparent about their fees and costs. But it's still up to you to do your research and read the fine print. And remember, ev depreciation and insurance is a complex topic, so don't be afraid to ask questions.

STORY_TEASE

My Friend's Crazy EV Insurance Refund Story

I've got a friend, let's call him Dave, who bought a brand new Tesla Model 3 and insured it with State Farm. He paid around $2,500 in premiums for the first year, but then he decided to cancel his policy and switch to a different company.

He was expecting a refund of around $1,500, but when he got the check, it was more like $800. He was furious, and he ended up spending hours on the phone with State Farm, trying to get them to explain why he didn't get the refund he was expecting. It was a total nightmare, and it's a story I'll never forget.

But, and this is the important part, Dave learned a valuable lesson about ev depreciation and insurance. He realized that he needed to do his research and read the fine print before signing up for a policy. And he also learned that it's always better to ask questions and seek advice from a professional.

COMPARISON

EV Insurance Refunds vs Other Types of Insurance

Getting an EV insurance refund is way different from getting a refund for other types of insurance, like health or life insurance. With those types of policies, you're usually dealing with more straightforward calculations and fewer hidden fees.

But with EV insurance, you've got to navigate a whole complex web of depreciation, pro-rata rules, and administrative fees. It's like comparing apples and oranges - they might look similar on the surface, but they're actually totally different.

And that's why it's so important to do your research and understand the ins and outs of ev depreciation and insurance. You don't wanna get caught off guard by some unexpected fee or charge.

FAQs

#### What is the average cost of EV insurance?

The average cost of EV insurance can range from $1,500 to $3,000 per year, depending on the make and model of your vehicle, as well as your location and driving history.

#### How do I calculate my EV insurance refund?

To calculate your EV insurance refund, you'll need to check your policy documents and understand the pro-rata rules and administrative fees associated with cancelling your policy.

#### Can I get a full refund if I cancel my EV insurance policy?

It's unlikely that you'll get a full refund if you cancel your EV insurance policy, especially if you've already paid premiums for part of the year. However, you may be able to get a partial refund, depending on the terms of your policy.

#### How does EV depreciation affect my insurance refund?

EV depreciation can affect your insurance refund, especially if you've got a high-end model like a Rivian. However, many insurance companies offer depreciation waivers or guarantees that can help protect your vehicle's value.

#### What are some common mistakes to avoid when getting an EV insurance refund?

Some common mistakes to avoid when getting an EV insurance refund include not reading the fine print, not understanding the pro-rata rules, and not factoring in administrative fees.

#### Are there any specific EV insurance companies that offer better refunds?

Some EV insurance companies, like Allstate and Progressive, are more transparent about their fees and costs, and may offer better refunds than others. However, it's always important to do your research and read reviews before choosing an insurance company.

#### Can I negotiate my EV insurance refund?

It's possible to negotiate your EV insurance refund, especially if you've been a loyal customer or have a good driving record. However, it's always best to have a clear understanding of your policy terms and the pro-rata rules before trying to negotiate.

Pro tip: always keep a record of your policy documents and premium payments, in case you need to dispute a refund or cancellation charge.

That's all from me — go save some money.

— Alex