Breaking news: just last week, Tesla announced a significant price drop for its Model 3 and Model Y in the US market, which is gonna impact EV depreciation and insurance rates. This move is expected to boost sales, but it also raises questions about the long-term value of these vehicles. Sound familiar? We've seen this happen before with other EV manufacturers, and it's gonna be interesting to see how insurance companies respond.

A Story of EV Depreciation and Insurance

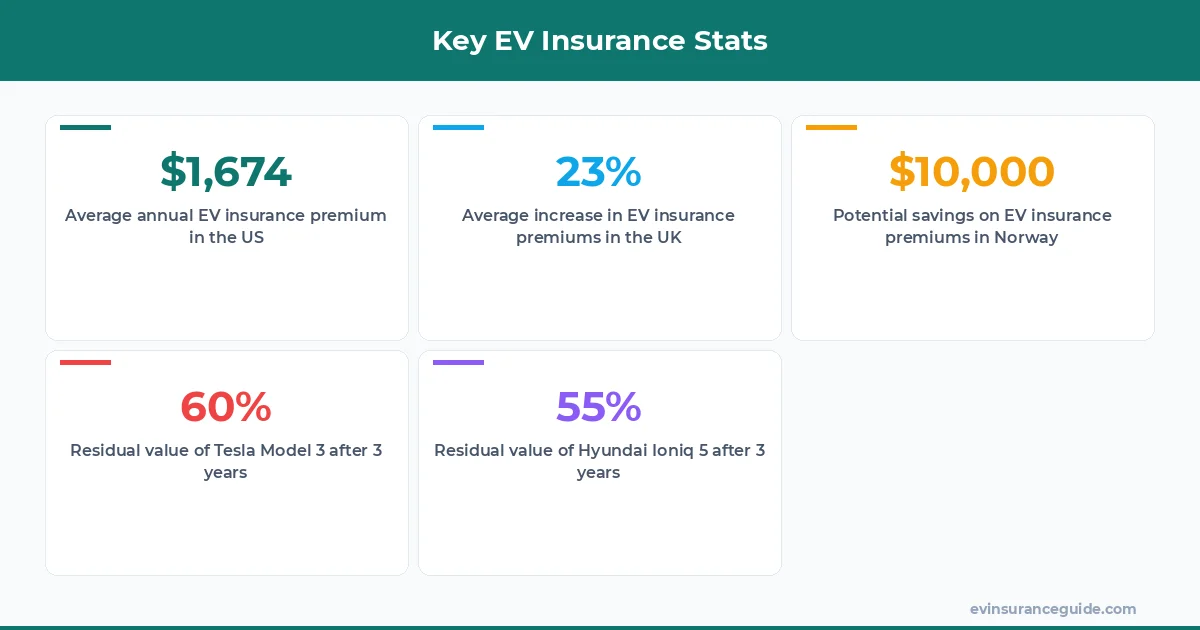

I've been following the EV insurance market for years, and I've seen some wild fluctuations in rates. For example, in the UK, EV insurance premiums have increased by an average of 23% over the past year, according to data from the Association of British Insurers. This is partly due to the growing demand for EVs, which has led to higher production costs and, subsequently, higher insurance rates. Know what the kicker is? The UK government has also introduced new regulations that require insurance companies to provide more comprehensive coverage for EVs, which has driven up costs even further. But, on the other hand, some insurers are offering discounts for EV owners who install home charging stations or use public charging networks.

Take the case of BMW iX owners in the US, who are seeing insurance premiums range from $1,500 to $3,000 per year, depending on their location, driving history, and other factors. That's a pretty wide range, and it's not just about the cost of the vehicle itself - it's also about the cost of replacing or repairing its advanced technology features. And, of course, there's the issue of EV depreciation, which can be a major concern for owners who plan to sell their vehicles in the future. For instance, a study by Kelley Blue Book found that the Tesla Model 3 retains around 60% of its value after three years, while the Hyundai Ioniq 5 retains around 55%.

But, here's the thing: not all EVs are created equal when it comes to insurance rates. The Rivian R1T, for example, is a luxury EV pickup truck that's priced around $70,000, and its insurance premiums are accordingly higher, ranging from $2,500 to $4,000 per year. On the other hand, the Nissan Leaf is a more affordable EV option, with insurance premiums ranging from $1,200 to $2,500 per year. So, it's all about doing your research and comparing rates from different insurers to find the best deal for your specific vehicle.

Warning: Hidden Costs in EV Insurance Policies

One thing to watch out for when shopping for EV insurance is hidden costs, such as administrative fees or charges for additional coverage options. These can add up quickly, and they're not always transparent. For instance, some insurers may charge an extra $100 to $300 per year for roadside assistance or towing services, which may not be necessary for all EV owners. And, of course, there are the inevitable rate hikes that come with renewing your policy each year. That one stung - I recently saw an EV owner's premium increase by 30% after just one year, simply because the insurer had raised its rates across the board.

To avoid these hidden costs, it's essential to carefully review your policy documents and ask questions before signing up. Don't be afraid to negotiate, either - some insurers may be willing to waive certain fees or offer discounts for loyal customers. And, if you're not satisfied with your current insurer, don't hesitate to shop around and compare rates from other providers. After all, it's your money, and you deserve to get the best value for it. Wild, right?

As a seasoned EV insurance expert, I've seen too many owners get caught out by these hidden costs. So, here's a pro tip: always read the fine print, and don't be afraid to ask questions. As the saying goes, 'if it sounds too good to be true, it probably is'.

Be cautious of insurers that offer 'too good to be true' deals, as these may come with hidden costs or limitations that can leave you high and dry in the event of a claim.

Honest Opinion: EV Depreciation and Insurance Rates Are a Concern

Let's be real - EV depreciation and insurance rates are a major concern for many owners, and it's not just about the cost of the vehicle itself. It's about the residual value, the cost of replacement parts, and the overall risk profile of the vehicle. And, honestly, some insurers are not doing enough to address these concerns. I mean, take the case of the Tesla Model S, which has been known to retain its value relatively well, but still commands high insurance premiums due to its advanced technology features and high repair costs.

But, here's the thing: not all EVs are created equal when it comes to depreciation and insurance rates. The Hyundai Kona Electric, for example, is a more affordable EV option that's priced around $36,000, and its insurance premiums are accordingly lower, ranging from $1,000 to $2,000 per year. And, of course, there are the various EV insurance discounts and incentives that are available, such as the US federal tax credit for EV purchases, which can help offset the cost of insurance premiums.

So, what's the solution? Well, actually, it's not just about finding the cheapest insurance policy - it's about finding a policy that provides comprehensive coverage and supports the long-term value of your vehicle. And, that's where the concept of 'ev depreciation and insurance' comes in - it's about understanding the complex interplay between these two factors and making informed decisions about your insurance policy.

OK So Here's the Deal With EV Insurance in Australia

In Australia, the EV insurance market is still in its infancy, but it's growing rapidly. Insurers such as NRMA and AAMI are offering specialized EV insurance policies that take into account the unique characteristics of these vehicles, such as their advanced technology features and higher repair costs. And, of course, there are the various state-based incentives and discounts that are available, such as the New South Wales government's rebate scheme for EV purchases.

But, here's the thing: the Australian EV insurance market is still largely unregulated, which means that owners need to be vigilant when shopping for policies. Some insurers may not provide adequate coverage or may charge excessive premiums, so it's essential to do your research and compare rates from different providers. And, don't forget to ask about any discounts or incentives that may be available, such as discounts for low-mileage drivers or owners who install home charging stations.

For instance, a study by the Australian Automobile Association found that EV owners in New South Wales can save up to $500 per year on their insurance premiums by installing a home charging station. And, of course, there are the various EV insurance comparison websites and tools that are available, which can help owners navigate the complex EV insurance landscape and find the best policy for their needs.

A Comparison of EV Insurance Rates Across the Globe

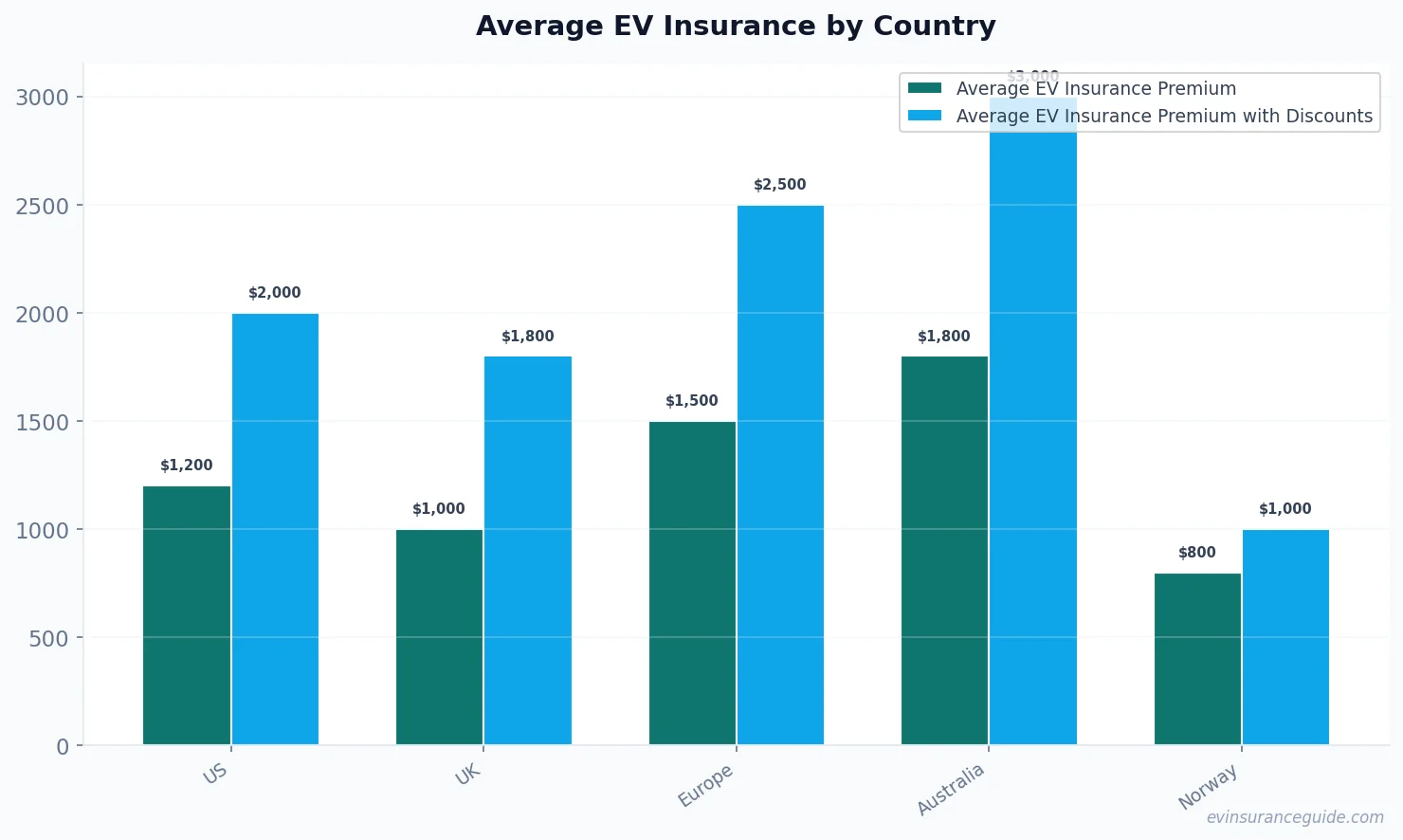

So, how do EV insurance rates compare across different countries? Well, it's a mixed bag, to say the least. In the US, EV insurance premiums are generally higher than in the UK or Europe, due to factors such as higher repair costs and more stringent safety regulations. But, on the other hand, some countries such as Norway and the Netherlands are offering significant incentives and discounts for EV owners, such as tax credits and exemptions from certain fees.

For example, in Norway, EV owners can save up to $10,000 per year on their insurance premiums by taking advantage of the country's generous tax credit scheme. And, of course, there are the various international EV insurance comparison websites and tools that are available, which can help owners navigate the complex global EV insurance landscape and find the best policy for their needs.

But, here's the thing: when it comes to 'ev depreciation and insurance', it's not just about comparing rates across different countries - it's about understanding the complex interplay between these two factors and making informed decisions about your insurance policy. So, do your research, compare rates, and don't be afraid to ask questions. Your wallet will thank you.

FAQs

#### What are the average EV insurance rates in the US?

The average EV insurance rates in the US range from $1,200 to $3,000 per year, depending on the vehicle make and model, location, driving history, and other factors.

#### How do EV insurance rates compare to traditional gasoline-powered vehicles?

EV insurance rates are generally higher than traditional gasoline-powered vehicles, due to factors such as higher repair costs and more stringent safety regulations.

#### What are some common discounts and incentives available for EV owners?

Some common discounts and incentives available for EV owners include low-mileage discounts, home charging station discounts, and tax credits.

#### Can I customize my EV insurance policy to fit my specific needs?

Yes, many insurers offer customizable EV insurance policies that allow you to tailor your coverage to fit your specific needs and budget.

#### How do I find the best EV insurance policy for my needs?

To find the best EV insurance policy for your needs, it's essential to do your research, compare rates from different providers, and ask questions about any discounts or incentives that may be available.

#### Are there any specific EV insurance requirements or regulations that I should be aware of?

Yes, there are various EV insurance requirements and regulations that you should be aware of, such as regulations related to safety features, emissions standards, and more.

And, finally, here's a key takeaway: when it comes to 'ev depreciation and insurance', it's all about understanding the complex interplay between these two factors and making informed decisions about your insurance policy. So, do your research, compare rates, and don't be afraid to ask questions. Until next time — Alex