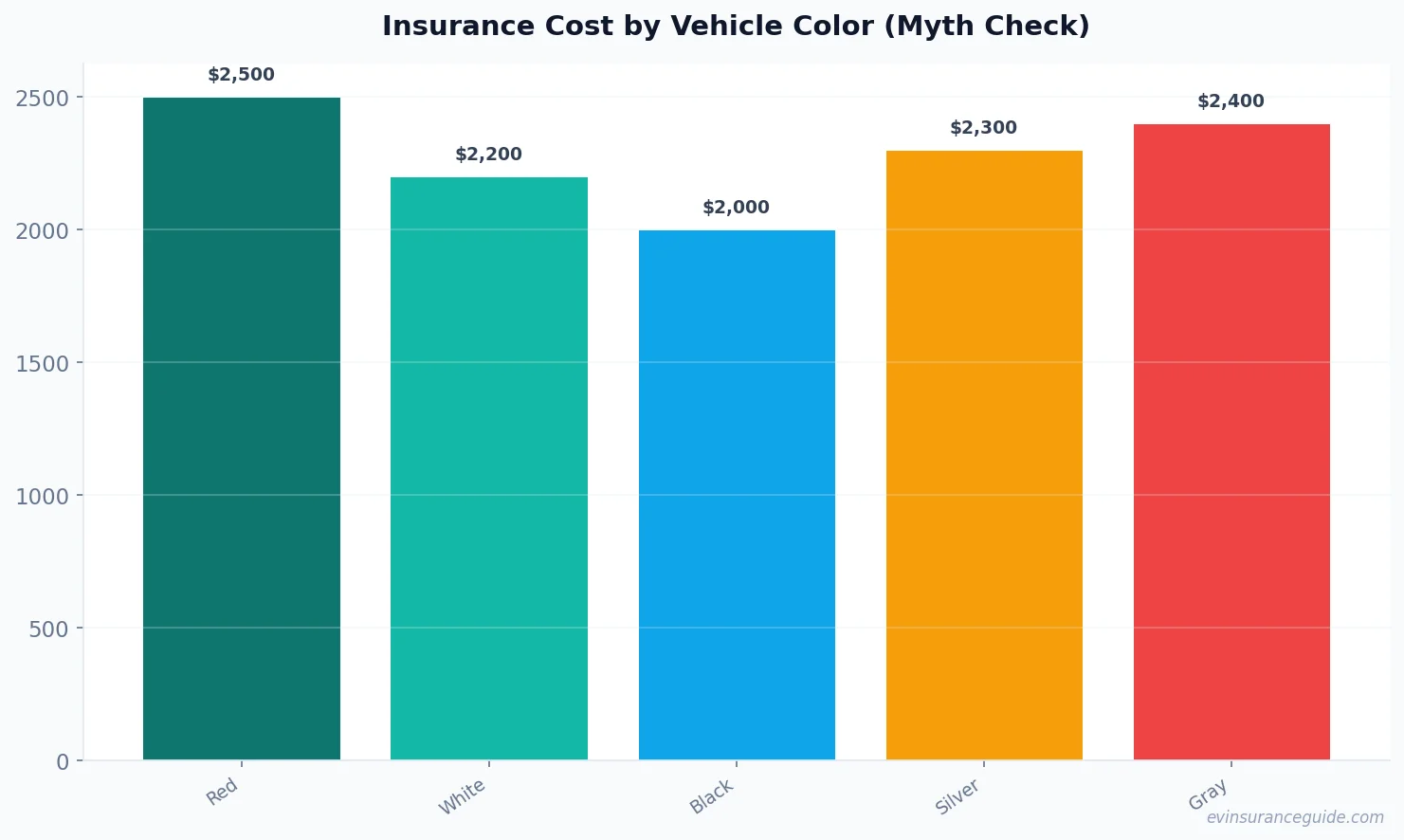

Paying more for insurance just because your EV is red? Sounds like a myth, right? But what if I told you that the color of your car can affect its depreciation, and that's a factor insurance companies consider? It's a complicated web, and I'm gonna break it down for you.

You see, EV depreciation and insurance are closely tied. A car that holds its value well will generally cost less to insure, and vice versa. For example, a Tesla Model 3, which retains its value amazingly well, will likely have lower insurance premiums compared to a car that depreciates faster, like the BMW iX. But does the color really play a role?

OK So Here's the Deal With EV Depreciation and Insurance

EV depreciation and insurance are like two peas in a pod - they're connected, but not in the way you think. The color of your car might not directly impact your insurance premiums, but it can affect the car's resale value, which in turn affects insurance costs. For instance, a white Hyundai Ioniq 5 might be more in demand than a red one, simply because white cars are often perceived as more desirable in many markets. This demand can influence the car's depreciation rate, and thus, its insurance premium.

But here's the thing: insurance companies like Geico, Progressive, and State Farm don't explicitly factor in the color of your car when calculating premiums. What they do consider, however, is the car's make, model, year, and - you guessed it - its expected depreciation. So, while the color itself might not be a direct factor, its impact on depreciation can indirectly influence your insurance costs.

Know what the kicker is? The perceived value of a car's color can vary wildly by region and cultural context. In some places, a red car is seen as a status symbol; in others, it's just a fancy way of saying 'cop magnet'. This subjective valuation can lead to differences in how quickly a car depreciates, depending on where you live and the local demand for certain car colors.

EV Depreciation and Insurance: A Comparison to Gas Guzzlers

Buying an EV is like investing in a house - it's a long-term commitment. And just like a house, the value of your EV can fluctuate based on various factors, including its condition, mileage, and - believe it or not - color. Now, compare this to gas guzzlers: their depreciation is often more straightforward, driven primarily by mileage and the rising cost of fuel. But EVs? They're a different story altogether.

For one, EVs have a higher upfront cost, which can lead to a steeper depreciation curve. However, their lower operating costs (think cheaper 'fuel' and less maintenance) can offset some of that initial expense. It's a trade-off, really. And when it comes to insurance, companies are still figuring out how to price EVs accurately, given their unique depreciation profiles.

Take the Rivian, for example. This electric truck is a beast, with capabilities that rival its gas-powered counterparts. But its insurance premiums? Those are still a bit of a mystery, largely because there's not enough data on how these vehicles depreciate over time. It's a chicken-and-egg problem: insurers need more data to set accurate premiums, but they can't get that data until more people buy and own these cars.

Get Ready for a Wild Story About EV Insurance and Depreciation

So, I've got a friend, let's call him Dave, who bought a brand-new Tesla Model Y last year. Beautiful car, and Dave was thrilled - until he got his insurance quote. It was higher than he expected, and he couldn't understand why. That's when he discovered that his car's depreciation was forecasted to be steeper than average, partly because of its color.

Now, Dave's story isn't unique. Many EV owners face similar situations, where the expected depreciation of their vehicle affects their insurance premiums. But here's the thing: you can negotiate with your insurer. If you've done your research and know your car's value, you can make a case for lower premiums. It's all about understanding how EV depreciation and insurance are intertwined.

Pro tip: When negotiating your insurance premiums, highlight your car's unique features that might reduce its depreciation rate, such as advanced safety features or a comprehensive maintenance record.

5 Key Factors That Actually Affect EV Insurance Premiums

Here are the factors that really influence your EV insurance costs:

- 1. The car's make and model - a Tesla Model 3 will generally cost less to insure than a Rivian, due to its lower purchase price and better depreciation rate.

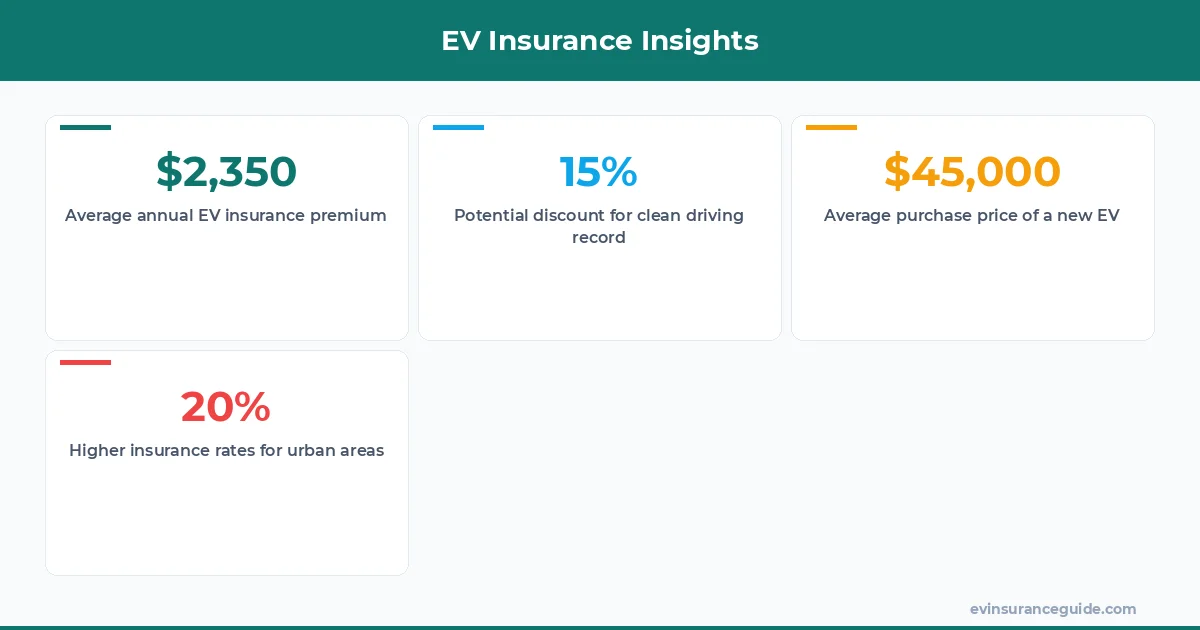

- 2. Your driving record - a clean record can save you up to 20% on premiums.

- 3. Where you live - urban areas tend to have higher insurance rates due to the increased risk of accidents and theft.

- 4. The car's safety features - cars with advanced safety features like lane departure warning systems can qualify for discounts.

- 5. Your annual mileage - driving less can lead to lower premiums, as you're less likely to be involved in an accident.

Honestly, EV Insurance Can Be a Total Rip-Off

I'm gonna be blunt here: some insurance companies are taking advantage of EV owners. They're charging higher premiums without fully understanding the unique depreciation profiles of these vehicles. It's not right, and it's up to us as consumers to push back.

We need more transparency in how insurance companies calculate EV premiums. We need them to consider the actual depreciation rates of these cars, rather than relying on outdated models that don't account for the lower operating costs and unique demand dynamics of EVs. Until then, we're at the mercy of an industry that's still learning how to price EV insurance accurately.

That one stung. But let's move on to some FAQs.

How does EV depreciation affect insurance premiums?

EV depreciation can affect insurance premiums by influencing the car's resale value. If a car depreciates quickly, its insurance premium might be higher to account for the potential loss in value.

Can I negotiate my EV insurance premiums?

Yes, you can negotiate your EV insurance premiums. Research your car's value, highlight its unique features that might reduce depreciation, and make a case to your insurer for lower premiums.

What's the average annual insurance premium for an EV?

The average annual insurance premium for an EV can range from $1,500 to $3,000, depending on the car's make, model, and your personal driving record.

Do all insurance companies offer EV insurance?

Not all insurance companies offer EV insurance, but most major providers like Geico, Progressive, and State Farm do. It's always a good idea to shop around and compare rates.

How does the color of my EV affect its insurance premium?

The color of your EV might indirectly affect its insurance premium by influencing its resale value. However, insurance companies do not explicitly factor in the color of your car when calculating premiums.

Can I get a discount on my EV insurance for having a good driving record?

Yes, a clean driving record can save you up to 20% on your EV insurance premiums.

Are EVs more expensive to insure than gas-powered cars?

EVs can be more expensive to insure than gas-powered cars, primarily due to their higher upfront cost and unique depreciation profiles. However, this can vary depending on the car's make, model, and your personal driving record.

And that's the truth about EV depreciation and insurance. It's complicated, but understanding how these factors interplay can save you money in the long run.

That's my two cents. Take it or leave it — but I hope it helps. — Alex