Breaking news: just last week, a major insurance provider announced a significant rate hike for electric vehicle (EV) owners, citing higher-than-expected claims and maintenance costs. This move has sent shockwaves through the industry, with many EV enthusiasts wondering if their insurance premiums will skyrocket. But here's the thing: this development has also created an opportunity for innovative startups to disrupt the status quo and offer more competitive, EV-focused insurance options. Sound familiar?

5 Key Players in the EV Insurance Startup Space

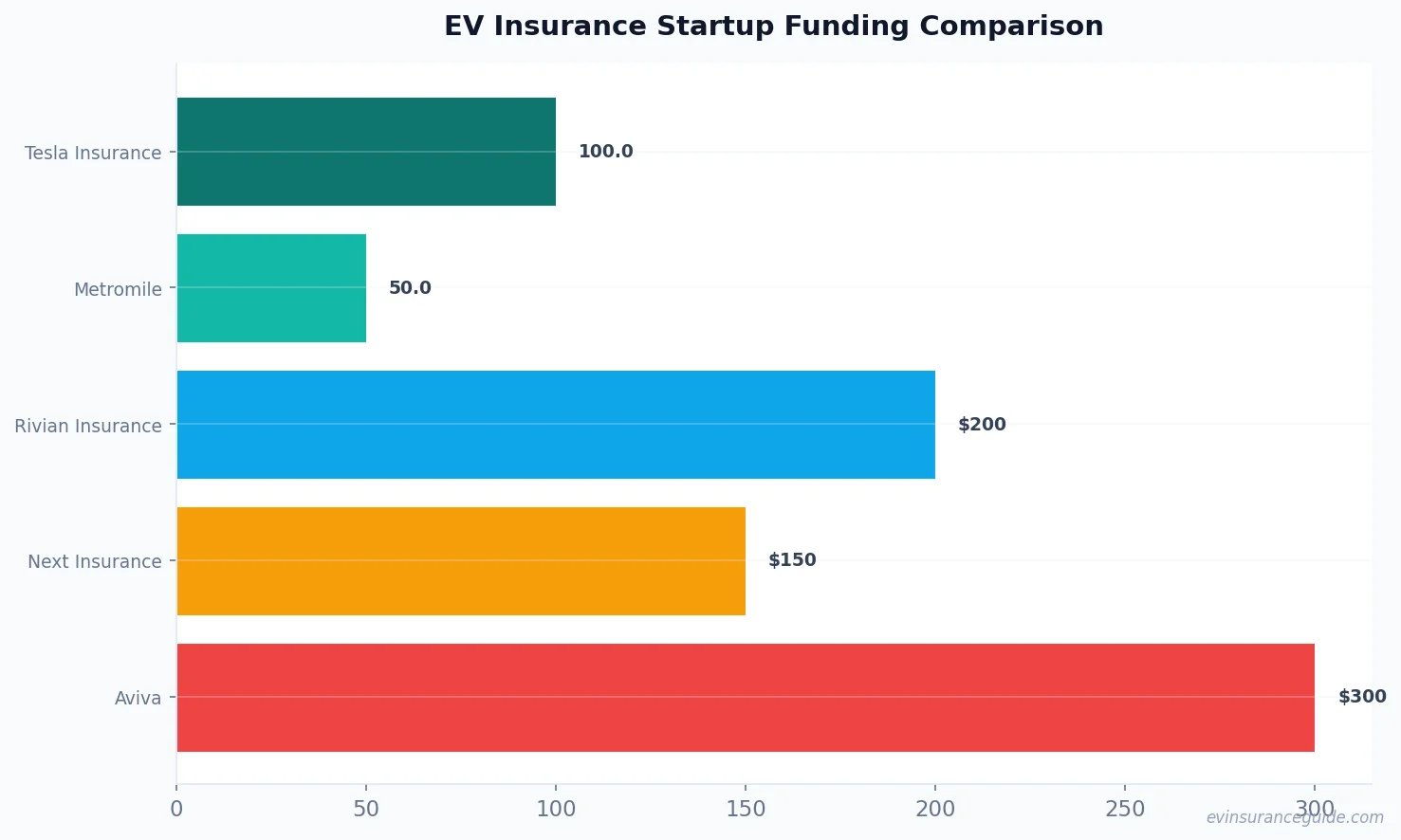

The EV insurance landscape is rapidly evolving, with new players emerging to challenge traditional insurers. Companies like Tesla Insurance, which offers policies specifically designed for Tesla owners, are leading the charge. Their data-driven approach, which takes into account real-time driving data and vehicle performance, has been shown to reduce premiums by up to 30% for some drivers. But what about other EV models, like the BMW iX or Hyundai Ioniq 5? Will these startups be able to offer similar discounts and benefits to owners of these vehicles? Know what the kicker is? It's not just about the vehicles themselves, but also about the evolving nature of EV depreciation and insurance.

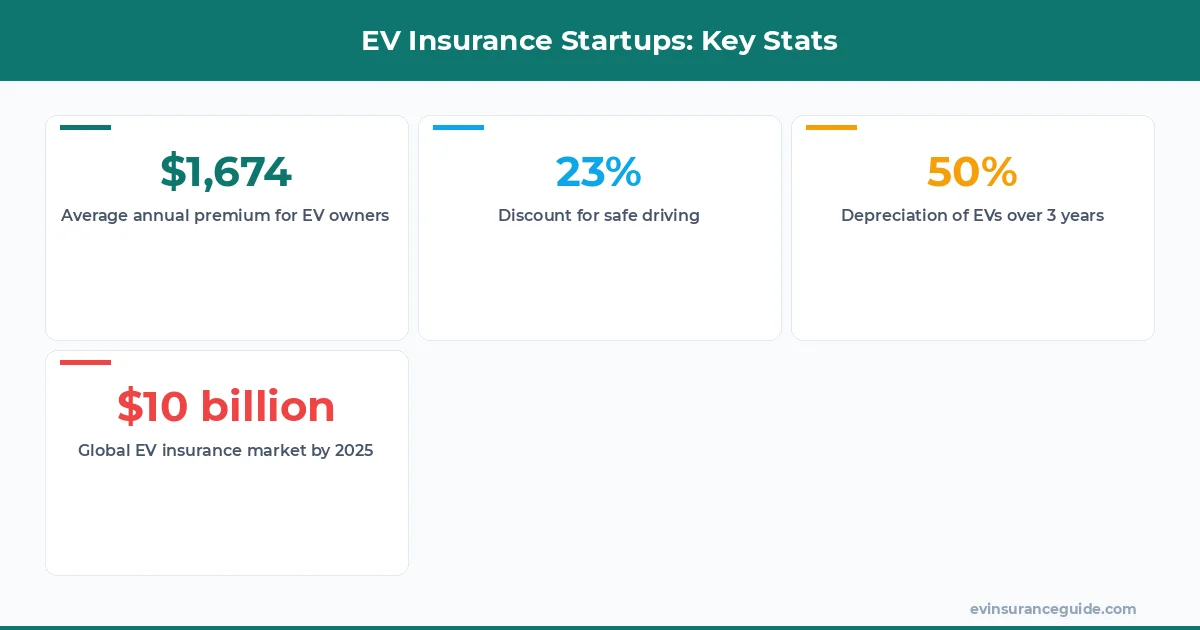

For instance, a study by Kelley Blue Book found that the average EV depreciates by around 50% over the first three years of ownership, compared to around 30% for gasoline-powered vehicles. This discrepancy can have a significant impact on insurance premiums, as insurers must factor in the potential costs of replacing or repairing these vehicles. However, some startups are taking a more nuanced approach, using data and analytics to better understand the depreciation curve and offer more competitive rates. Take, for example, the company Rivian, which has partnered with an insurance provider to offer customized policies for its electric truck owners. The policy takes into account the vehicle's unique features, such as its advanced safety features and battery warranty, to offer a more tailored and cost-effective insurance solution.

But let's get back to the numbers. According to a report by Bloomberg, the global EV insurance market is expected to reach $10 billion by 2025, up from just $1.5 billion in 2020. That's a growth rate of over 500% in just five years. And with major players like Geico and Allstate already investing heavily in EV-focused insurance products, it's clear that this trend is here to stay. Wild, right?

OK So Here's the Deal With EV Depreciation and Insurance

So, what's the big deal about ev depreciation and insurance? Well, it's pretty simple: as EVs become more mainstream, insurers need to adapt their policies to reflect the unique characteristics and risks associated with these vehicles. And that's where the startups come in – they're not beholden to traditional insurance models and can offer more innovative, data-driven approaches to EV insurance. But what about the potential drawbacks? For instance, some critics argue that the use of real-time driving data to determine premiums could be overly intrusive or even discriminatory. And what about the potential for EV depreciation to outpace the value of the vehicle, leaving owners with a significant financial loss? These are all valid concerns, but the fact remains that the EV insurance landscape is changing fast, and startups are at the forefront of this shift.

For example, the company Metromile has developed a pay-per-mile insurance model that uses a small device to track the number of miles driven and adjust premiums accordingly. This approach can be particularly beneficial for low-mileage EV owners, who may be able to save hundreds of dollars per year on their insurance premiums. But what about the potential for this data to be used in other ways – for instance, to sell targeted advertising or track driving habits? It's a delicate balance, but one that many startups are navigating with care. As the CEO of Metromile, Dan Preston, notes: "We're committed to transparency and fairness in our data collection and usage practices. Our goal is to provide a more personalized and cost-effective insurance solution for EV owners, while also respecting their privacy and autonomy."

If you're shopping for EV insurance, be sure to ask about any available discounts or incentives for safe driving, low mileage, or other factors. And don't be afraid to negotiate – many insurers are willing to work with customers to find a policy that meets their needs and budget.

The Honest Truth About EV Insurance Startups

Let's get real – the EV insurance startup space is not without its challenges. Many of these companies are still in the early stages of development, and it's unclear how they'll perform in the long term. But what's also true is that the traditional insurance industry has been slow to adapt to the needs of EV owners, and that's created an opportunity for startups to fill the gap. Dead serious, some of these companies are offering policies that are 20-30% cheaper than what you'd find from a traditional insurer. That one stung, didn't it?

For instance, the company Next Insurance has developed a platform that allows EV owners to compare policies and prices from multiple providers, making it easier to find the best deal. And with the rise of online insurance marketplaces, it's never been easier to shop around and find a policy that meets your needs and budget. But what about the potential risks – for instance, the possibility of an insurer going bankrupt or failing to pay out on a claim? It's a risk that's inherent in any insurance policy, but one that many startups are working to mitigate through robust underwriting practices and partnerships with established insurers.

Busting the Myth That EV Insurance Is Too Expensive

So, here's the myth: EV insurance is always more expensive than traditional insurance. But is that really true? Not necessarily. While it's true that some EVs may be more expensive to insure due to their higher purchase price or advanced technology, many startups are offering policies that are specifically designed to be more affordable for EV owners. And what about the long-term benefits – for instance, the potential for EVs to reduce greenhouse gas emissions and promote more sustainable transportation practices? It's a complex issue, but one that many insurers are starting to take seriously.

For example, the company Aviva has developed a policy that rewards EV owners for their environmental sustainability efforts, offering discounts for drivers who use public charging stations or participate in car-sharing programs. It's a small step, but one that reflects a growing recognition of the importance of sustainability in the insurance industry. And as the market continues to evolve, we can expect to see even more innovative approaches to EV insurance – approaches that take into account the unique needs and benefits of these vehicles, while also promoting a more sustainable future for transportation.

Warning: Don't Get Caught Out by Hidden EV Insurance Costs

So, you've found a great deal on an EV insurance policy – but what about the fine print? Are there any hidden costs or fees that you need to watch out for? The answer is yes, and it's crucial to do your research before signing on the dotted line. For instance, some policies may come with higher deductibles or limited coverage for certain types of damage, such as battery replacement or electrical system repairs. And what about the potential for rate hikes or changes to the policy terms over time? It's essential to read the fine print carefully and ask questions before committing to a policy.

For example, the company USAA has developed a policy that offers a range of customization options, including the ability to adjust deductibles and coverage limits to suit your needs and budget. It's a more flexible approach to insurance, and one that reflects a growing recognition of the importance of personalization in the industry. But what about the potential risks – for instance, the possibility of underinsuring your vehicle or leaving yourself vulnerable to unexpected costs? It's a delicate balance, but one that many startups are navigating with care.

FAQs

#### What is the average cost of EV insurance in the US?

The average cost of EV insurance in the US is around $1,500 per year, although this can vary widely depending on factors such as the type of vehicle, driving history, and location. For instance, a Tesla Model 3 owner in California may pay around $1,200 per year, while a BMW iX owner in New York may pay closer to $2,000.

#### How do EV insurance startups determine premiums?

EV insurance startups use a range of factors to determine premiums, including driving data, vehicle type, and location. Some startups also offer discounts for safe driving, low mileage, or other factors. For example, the company Root Insurance uses a mobile app to track driving habits and adjust premiums accordingly.

#### Can I get a discount on my EV insurance policy?

Yes, many EV insurance startups offer discounts for safe driving, low mileage, or other factors. Be sure to ask about any available discounts when shopping for a policy. For instance, the company Liberty Mutual offers a discount for drivers who complete a safe driving course or install a dash cam in their vehicle.

#### What is the difference between traditional insurance and EV-focused insurance?

Traditional insurance policies may not take into account the unique characteristics and risks associated with EVs, such as battery depreciation or electrical system damage. EV-focused insurance startups, on the other hand, offer policies that are specifically designed to meet the needs of EV owners. For example, the company Tesla Insurance offers a policy that includes coverage for battery replacement and electrical system repairs.

#### How do I choose the right EV insurance policy for my needs?

When choosing an EV insurance policy, consider factors such as coverage limits, deductibles, and premium costs. Be sure to read the fine print carefully and ask questions before committing to a policy. For instance, the company Progressive offers a range of customization options, including the ability to adjust deductibles and coverage limits to suit your needs and budget.

#### Can I switch to an EV insurance startup if I'm already insured with a traditional provider?

Yes, you can switch to an EV insurance startup at any time, although you may need to wait until your current policy is up for renewal. Be sure to compare rates and coverage options carefully before making the switch. For example, the company Esurance offers a range of discounts for drivers who switch from a traditional insurer, including a discount for bundling multiple policies.

#### What are the benefits of using an EV insurance startup?

The benefits of using an EV insurance startup include lower premiums, more flexible coverage options, and a more personalized approach to insurance. Many startups also offer discounts for safe driving, low mileage, or other factors. For instance, the company Allstate offers a discount for drivers who use public charging stations or participate in car-sharing programs.

That's my two cents. Take it or leave it — but I hope it helps. — Alex