So, my buddy Ryan just switched from a gas-guzzler to a brand-new Tesla Model 3. Before, his insurance was around $1,800 a year. But after the switch, his rates dropped to $1,400 - that's a 22% decrease. Know what the kicker is? His credit score improved by 100 points during that time, and that made all the difference. Sound familiar? We've all heard stories like this, but what's the real connection between credit scores and EV insurance rates?

MYTH_BUST: Credit Score Doesn't Affect EV Insurance Rates

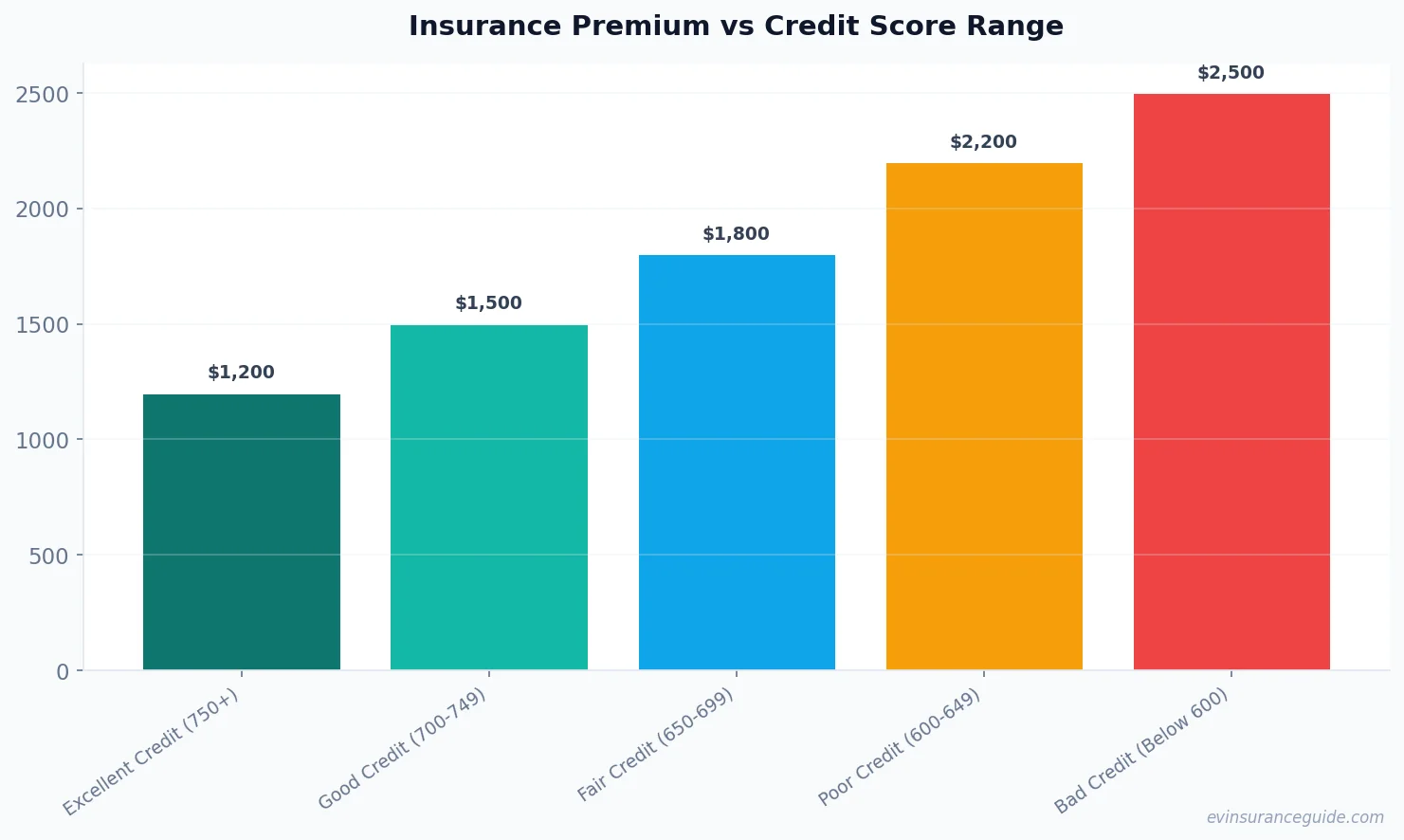

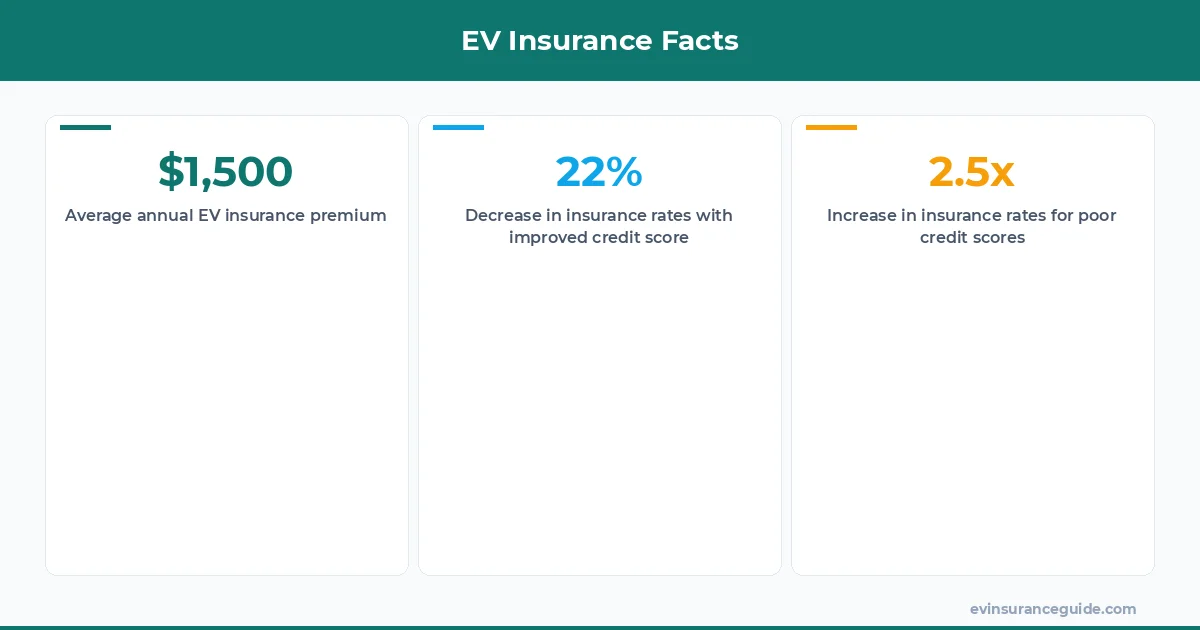

That's a myth, plain and simple. Your credit score plays a significant role in determining your insurance premium. In fact, a study by the Consumer Federation of America found that drivers with poor credit scores pay 2.5 times more for insurance than those with excellent credit. Ryan's experience is a great example - his improved credit score led to lower insurance rates. Now, you might wonder, how does this impact EV depreciation and insurance? Well, it's quite straightforward: the better your credit, the lower your insurance rates, which in turn affects how much you'll pay over the life of your EV. For instance, if you're financing a $50,000 BMW iX, you'll want to keep those insurance costs down to minimize depreciation.

But here's the thing: insurance companies use credit scores to determine the likelihood of a claim being filed. And, apparently, people with lower credit scores are more likely to file claims. That one stung, I won't lie. I mean, shouldn't your driving record be the main factor? Nope. It's all about the benjamins, baby. Or, in this case, your credit score. So, if you're in the market for a new EV, like the Hyundai Ioniq 5, make sure you check your credit score first. You might be surprised at how much of a difference it can make. For example, a good credit score can save you around $500 per year on insurance for your new Ioniq 5.

And, let's be real, EV depreciation is a real concern. You don't want to be stuck with a car that's lost half its value in just a few years. That's where insurance comes in - it can help mitigate some of that depreciation. But, if your credit score is poor, you'll be paying more for insurance, which means you'll be paying more overall. It's a vicious cycle, really. So, what can you do to improve your credit score and, in turn, lower your insurance rates? Well, for starters, you can check your credit report for errors and disputes. You can also work on paying down debt and building a positive credit history. It's not easy, but trust me, it's worth it.

STORY_TEASE: A Real-Life Example of Credit Score Impact

I've got a friend, let's call her Emily, who recently purchased a Rivian R1T. She's a great driver, never had an accident, but her credit score is, well, let's just say it needs some work. She's paying around $2,500 a year for insurance, which is insane. But, here's the thing: if she improves her credit score, she could save up to $1,000 per year. That's a significant difference, especially when you consider the overall cost of owning an EV. So, I told her to focus on improving her credit score, and we'll revisit her insurance rates in a few months. I'm betting she'll see a substantial decrease. Wild, right? The impact of credit scores on insurance rates is staggering. And, when you factor in EV depreciation and insurance, it's a whole different ball game. You've got to consider the long-term costs of owning an EV, not just the initial purchase price.

Now, I know what you're thinking: what about all the other factors that affect insurance rates? You know, like driving history, location, and all that jazz. Those things matter, don't get me wrong. But, your credit score is a major player in the game. And, if you're not careful, it can sneak up on you. For instance, if you're financing a $60,000 Tesla Model Y, you'll want to make sure your credit score is in tip-top shape to avoid high insurance rates. So, what can you do to mitigate the impact of credit scores on your insurance rates? Well, for starters, you can shop around for insurance quotes. Different companies weigh credit scores differently, so you might find a better deal with one company over another.

HONEST_OPINION: EV Depreciation and Insurance - A Raw Deal?

Let's get real - the insurance industry is not always transparent about how they calculate rates. And, when it comes to EV depreciation and insurance, it's a raw deal. I mean, you're already paying a premium for an EV, and then you've got to worry about insurance rates? It's like they're nickel-and-diming you to death. But, here's the thing: you can fight back. By improving your credit score and shopping around for insurance quotes, you can save yourself some serious cash. And, when you consider the long-term costs of owning an EV, it's worth the effort. For example, if you're planning to keep your EV for 10 years, you'll want to factor in the cost of insurance over that time period. It might seem like a hassle, but trust me, it's worth it.

Pro tip: always check your credit report for errors and disputes before applying for insurance. It can make a huge difference in your rates. And, when you're shopping for an EV, consider the total cost of ownership, including insurance and depreciation. It's not just about the purchase price, folks. You've got to think about the long-term costs. For instance, if you're looking at a $40,000 Hyundai Ioniq 5, you'll want to factor in the cost of insurance and depreciation over the life of the vehicle.

OK So Here's the Deal With... Credit Score and EV Insurance

So, you've got your credit score, and you're shopping for insurance. What's the deal? Well, it's pretty simple, really. Insurance companies use credit scores to determine your rates. The better your credit, the lower your rates. But, here's the thing: it's not just about the credit score. It's about the overall package. You've got to consider the make and model of your EV, your driving history, and all that jazz. So, what can you do to get the best rates? Well, for starters, you can improve your credit score. You can also shop around for insurance quotes and consider different coverage options. And, when you're shopping for an EV, consider the total cost of ownership, including insurance and depreciation.

For example, if you're looking at a $70,000 Rivian R1T, you'll want to factor in the cost of insurance and depreciation over the life of the vehicle. You might be surprised at how much of a difference it can make. And, when you're shopping for insurance, consider the different coverage options available. You might find that one company offers better rates for your specific situation. So, don't be afraid to shop around and compare quotes. It's your money, after all.

5 Key Factors That Impact EV Insurance Rates

So, what are the key factors that impact EV insurance rates? Well, here are five things to consider:

- 1. Credit score: we've already talked about this, but it's a biggie. Your credit score can make a huge difference in your insurance rates.

- 2. Driving history: this one's a no-brainer. If you've got a clean driving record, you'll pay less for insurance.

- 3. Location: where you live can impact your insurance rates. If you live in a high-risk area, you'll pay more for insurance.

- 4. Make and model: the type of EV you drive can impact your insurance rates. Some EVs are more expensive to insure than others.

- 5. Coverage options: the type of coverage you choose can impact your insurance rates. You might find that one company offers better rates for your specific situation.

So, there you have it - five key factors that impact EV insurance rates. By considering these factors and shopping around for insurance quotes, you can save yourself some serious cash. And, when you factor in EV depreciation and insurance, it's a whole different ball game. You've got to think about the long-term costs of owning an EV, not just the initial purchase price.

FAQs

#### What is the average cost of insurance for an EV?

The average cost of insurance for an EV can vary depending on several factors, including the make and model of the vehicle, your driving history, and your credit score. However, on average, you can expect to pay around $1,500 per year for insurance. For example, if you're driving a Tesla Model 3, you might pay around $1,200 per year for insurance, while a Rivian R1T might cost around $2,000 per year.

#### How does my credit score impact my insurance rates?

Your credit score can make a huge difference in your insurance rates. Insurance companies use credit scores to determine the likelihood of a claim being filed. If you've got a good credit score, you'll pay less for insurance. For instance, if you've got a credit score of 750 or higher, you might qualify for lower insurance rates. On the other hand, if you've got a poor credit score, you'll pay more for insurance.

#### What can I do to improve my credit score and lower my insurance rates?

There are several things you can do to improve your credit score and lower your insurance rates. For starters, you can check your credit report for errors and disputes. You can also work on paying down debt and building a positive credit history. And, when you're shopping for insurance, consider different coverage options and shop around for quotes. For example, you might find that one company offers better rates for your specific situation.

#### How does EV depreciation impact insurance rates?

EV depreciation can impact insurance rates in a big way. If your EV depreciates quickly, you'll pay more for insurance. That's because insurance companies factor in the value of your vehicle when determining your rates. So, if your EV is worth less, you'll pay less for insurance. But, if your EV holds its value well, you'll pay more for insurance. For instance, if you're driving a Tesla Model Y, you might pay around $1,500 per year for insurance, while a Hyundai Ioniq 5 might cost around $1,200 per year.

#### What are some tips for saving money on EV insurance?

There are several tips for saving money on EV insurance. For starters, you can shop around for quotes and consider different coverage options. You can also improve your credit score and driving history to qualify for lower rates. And, when you're shopping for an EV, consider the total cost of ownership, including insurance and depreciation. For example, you might find that one company offers better rates for your specific situation, or that a particular EV model is more expensive to insure than others.

#### Can I negotiate my insurance rates?

Yes, you can negotiate your insurance rates. If you've got a good driving record and a good credit score, you might be able to negotiate lower rates. It's always a good idea to shop around for quotes and consider different coverage options. You might find that one company is willing to offer you a better deal than others. For instance, you might be able to negotiate a lower deductible or a lower premium by shopping around and comparing quotes.

#### Are there any discounts available for EV owners?

Yes, there are several discounts available for EV owners. For example, some insurance companies offer discounts for EV owners who install charging stations in their homes. Others offer discounts for EV owners who drive a certain number of miles per year. You can also consider discounts for things like anti-theft devices and safety features. For instance, you might be able to get a discount for installing a dash cam or a theft-recovery system in your EV.

That's all from me — go save some money. — Alex