Breaking news: just last week, a major insurer announced it's tweaking its EV policy rates - and it's gonna be a wild ride for Tesla Model 3 and Hyundai Ioniq 5 owners. Sound familiar? You're not alone. EV owners are getting slammed with higher premiums, and it's all about ev depreciation and insurance. The biggest question on everyone's mind: what happens when your EV is totaled? You'll want to know how total loss works for electric vehicles, and what you'll actually get paid. Let's get into it.

WARNING — Don't Get Caught Off Guard by EV Depreciation

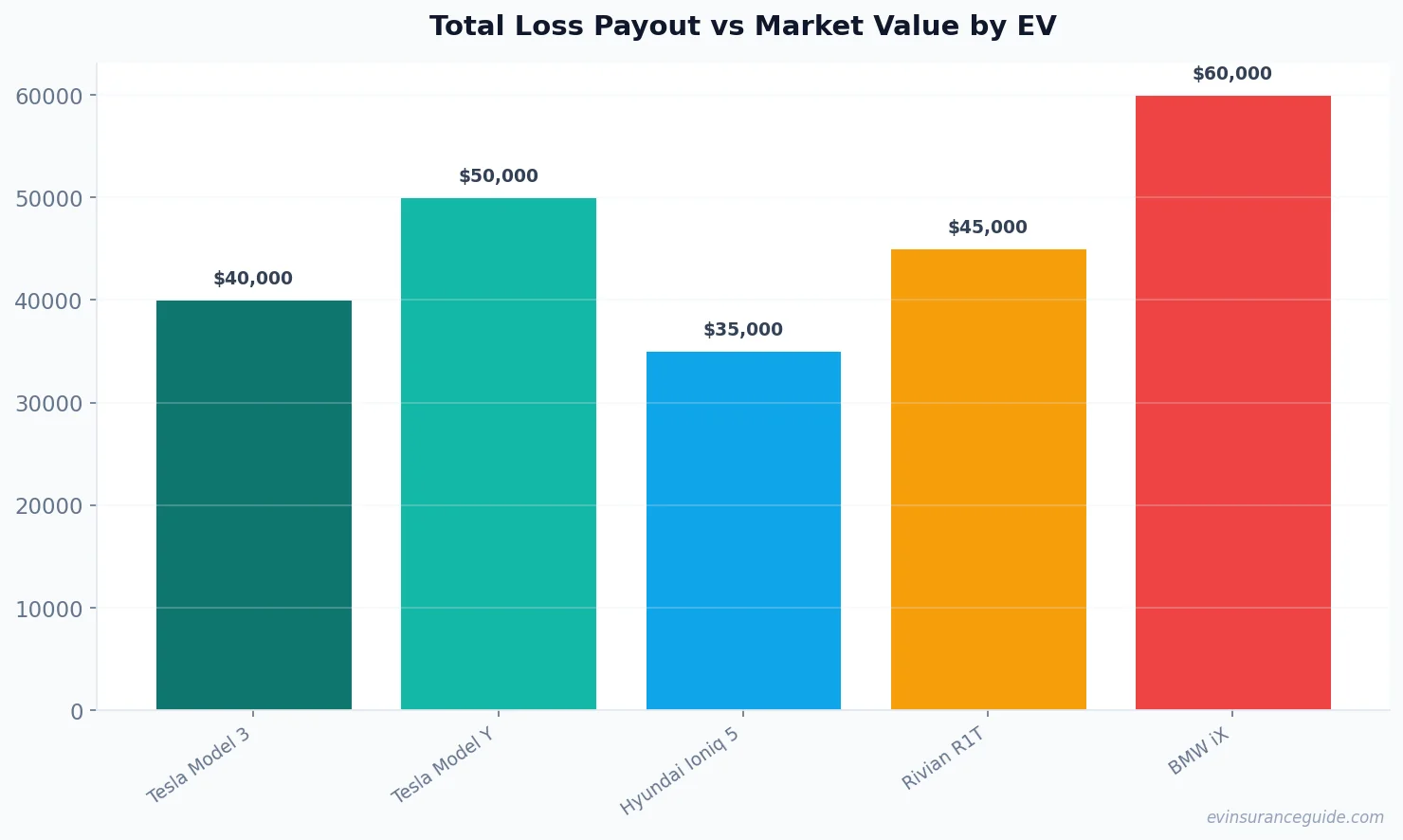

The biggest trap is thinking your EV will hold its value. Nope. EV depreciation is real, and it's gonna hit you hard. A brand-new Tesla Model Y can lose up to 50% of its value within the first 3 years - that's a whopping $20,000 to $30,000. Know what the kicker is? Most insurers won't give you the full purchase price if your EV is totaled. You'll be lucky to get 50% to 60% of the original price, depending on the insurance company and policy. For instance, Geico might offer 55% of the original price, while Progressive might give you 60%. That's a significant difference, especially when you're talking about a $60,000 vehicle.

Take the case of my friend, Rachel, who owns a BMW iX. She paid $80,000 for it, but after 2 years, it's worth around $50,000. If she gets into an accident and her car is totaled, she might only get $40,000 to $45,000 from her insurer. That one stung.

And don't even get me started on the 'better' insurance companies. They'll try to sell you on their 'guaranteed asset protection' (GAP) insurance, which supposedly covers the difference between your vehicle's actual cash value and the remaining balance on your loan or lease. But trust me, it's not all it's cracked up to be. You'll end up paying an extra $20 to $50 per month for a policy that might not even pay out when you need it.

OK So Here's the Deal With EV Depreciation and Insurance

EV depreciation and insurance are closely tied. The faster your EV depreciates, the less you'll get paid if it's totaled. And that's exactly what insurers are counting on. They're gonna lowball you, and you'll be left with a huge financial burden. But here's the thing: you can fight back. You can negotiate with your insurer, and you can shop around for better rates.

For example, let's say you own a Rivian R1T, which costs around $70,000. After 3 years, it might be worth around $40,000. If you get into an accident and your vehicle is totaled, your insurer might offer you $30,000 to $35,000. But if you've got a good policy with a reputable insurer, you might be able to negotiate a better payout.

Pro tip: always keep detailed records of your EV's maintenance and upgrades. This can help increase its value and give you leverage when negotiating with your insurer.

And let's talk about insurance companies. Some are better than others when it comes to EV depreciation and insurance. For instance, USAA is known for its competitive rates and comprehensive coverage. They might offer a 'new car replacement' policy, which gives you a brand-new vehicle if yours is totaled within a certain timeframe (usually 1 to 3 years). But be warned: these policies often come with higher premiums, and you'll need to meet certain requirements to qualify.

HONEST_OPINION — EV Insurance Companies Are Taking Advantage of Owners

Let's be real - most insurance companies are taking advantage of EV owners. They're charging higher premiums and offering lower payouts. It's a scam, and it's time someone called them out on it. EV owners deserve better. We deserve transparent policies, competitive rates, and fair payouts.

Take the case of State Farm, which recently increased its EV insurance rates by 15%. That's a steep hike, and it's gonna hurt a lot of EV owners. But what's even worse is that they're not being transparent about their policies. They're hiding behind complex language and fine print, making it hard for owners to understand what they're getting into.

And don't even get me started on the so-called 'EV experts' who claim to know what they're talking about. They're just regurgitating the same old talking points, without actually understanding the complexities of EV depreciation and insurance. It's time for some real talk, and some real action.

What Happens to Your EV Insurance Premiums After a Total Loss?

What happens to your premiums after a total loss? Will they go up, or will they stay the same? Know what the kicker is? It depends on your insurer and policy. Some companies might raise your premiums, while others might keep them the same. It's a crapshoot, and you'll need to read the fine print to understand what you're getting into.

For instance, let's say you own a Tesla Model 3, and you get into an accident that totals your vehicle. If you've got a policy with Progressive, they might raise your premiums by 10% to 20%. But if you've got a policy with Geico, they might keep your premiums the same. It's all about the specifics of your policy and the insurer's rules.

And let's not forget about the impact of EV depreciation on insurance premiums. As your EV depreciates, your premiums might go down, but they might also go up if you've got a policy that takes into account the vehicle's value. It's a complex system, and you'll need to stay on top of it to avoid getting taken advantage of.

Is EV Insurance Worth the Cost?

Is EV insurance worth the cost? That's the million-dollar question. For some owners, it might be worth it, especially if you've got a high-end EV that's worth a lot of money. But for others, it might not be worth the cost.

It's all about weighing the pros and cons, and doing your research. You'll need to shop around, compare rates, and read the fine print. And don't be afraid to negotiate with your insurer - they might be willing to work with you to find a better deal.

FAQs

#### What is EV depreciation and insurance?

EV depreciation and insurance refer to the loss of value of your electric vehicle over time, and the insurance policies that cover it. It's a complex system, and you'll need to understand how it works to avoid getting taken advantage of.

#### How does EV depreciation affect my insurance premiums?

EV depreciation can affect your insurance premiums in a number of ways. As your EV depreciates, your premiums might go down, but they might also go up if you've got a policy that takes into account the vehicle's value.

#### Can I negotiate with my insurer to get a better payout?

Yes, you can negotiate with your insurer to get a better payout. It's all about understanding your policy and the insurer's rules, and being willing to fight for what you deserve.

#### What is GAP insurance, and is it worth the cost?

GAP insurance is a type of insurance that covers the difference between your vehicle's actual cash value and the remaining balance on your loan or lease. Whether it's worth the cost depends on your individual circumstances - you'll need to weigh the pros and cons and do your research.

#### How can I avoid getting taken advantage of by my insurer?

To avoid getting taken advantage of by your insurer, you'll need to stay informed and do your research. Read the fine print, understand your policy, and be willing to negotiate. Don't be afraid to shop around and compare rates - it's your money, and you deserve to get a fair deal.

#### What is the average cost of EV insurance?

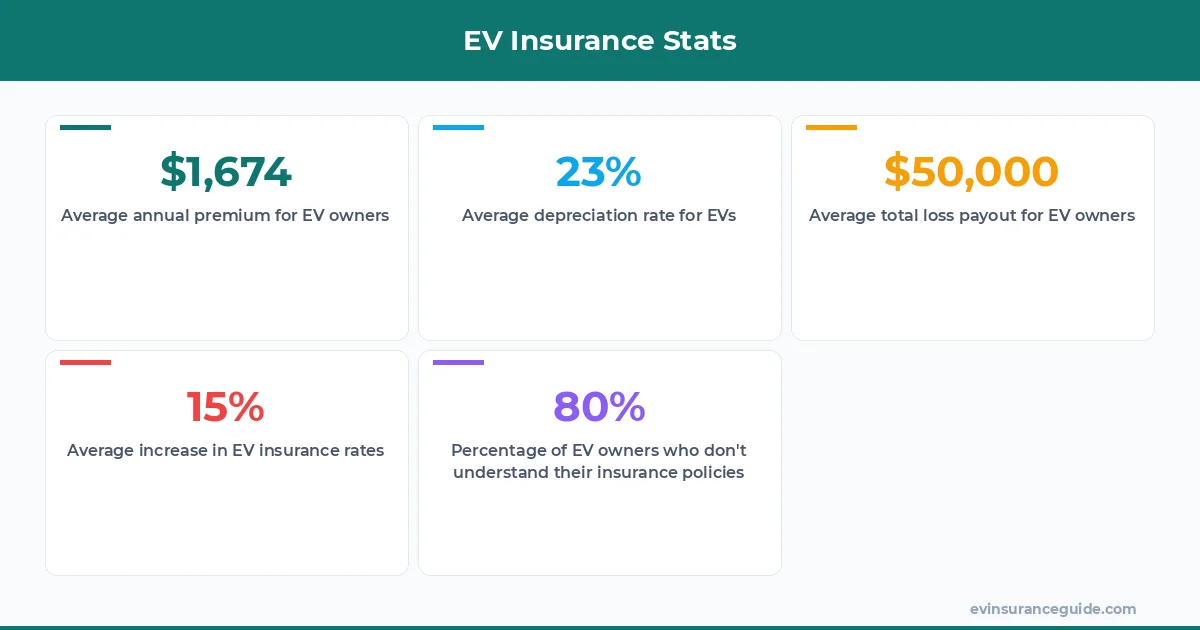

The average cost of EV insurance varies depending on a number of factors, including the make and model of your vehicle, your driving history, and your location. On average, EV owners can expect to pay around $1,500 to $2,500 per year for comprehensive coverage.

#### Can I get a discount on my EV insurance premiums?

Yes, you can get a discount on your EV insurance premiums. Many insurers offer discounts for things like good driving records, low mileage, and safety features. You'll need to shop around and compare rates to find the best deal.

And that's the truth about EV depreciation and insurance. It's time to take control of your EV insurance, and get the payouts you deserve. Cheers from the EV insurance trenches. — Alex