I'm standing at a charging station, sipping on a coffee, and I overhear a conversation between two EV owners about their insurance experiences. One of them mentions how their premium increased after installing a telematics device in their Tesla Model 3. The other owner, a BMW iX driver, shares a similar story, but with a twist - their insurance company actually lowered their premium after reviewing the telematics data. This got me thinking... what exactly is being reported about us, and how does it impact our insurance costs?

Tease a Story

I recall a friend, let's call him Ryan, who owned a Hyundai Ioniq 5. He was a careful driver, always following the speed limit and avoiding sudden accelerations. But one day, he received a notification from his insurance company, stating that his premium would increase due to 'aggressive driving habits'. Ryan was shocked, as he knew he was a safe driver. It turned out that the telematics device in his car had misinterpreted his driving style, and he had to appeal the decision. Sound familiar? Know what the kicker is? The insurance company had been using outdated software to analyze the data, which led to the incorrect assessment. Wild, right?

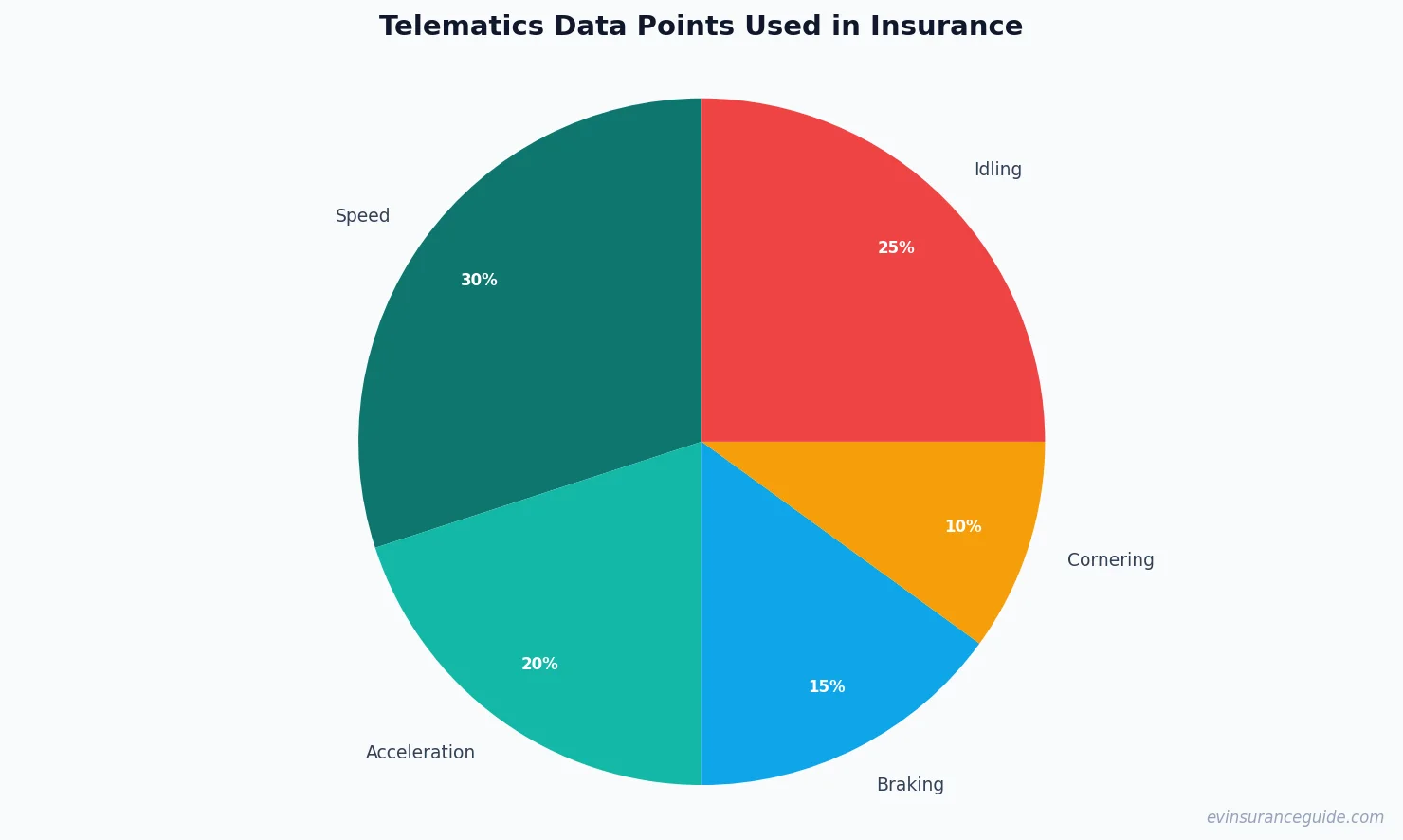

The use of telematics data in insurance pricing is becoming increasingly common, and it's essential to understand how it works. For instance, companies like Progressive and Allstate offer usage-based insurance programs, which use telematics devices to track driving habits and adjust premiums accordingly. The data collected includes information on speed, acceleration, braking, and cornering, among other factors. This data is then used to create a profile of the driver, which determines their insurance risk level. But here's the thing - the accuracy of this data is crucial, and any errors can lead to incorrect assessments, like in Ryan's case.

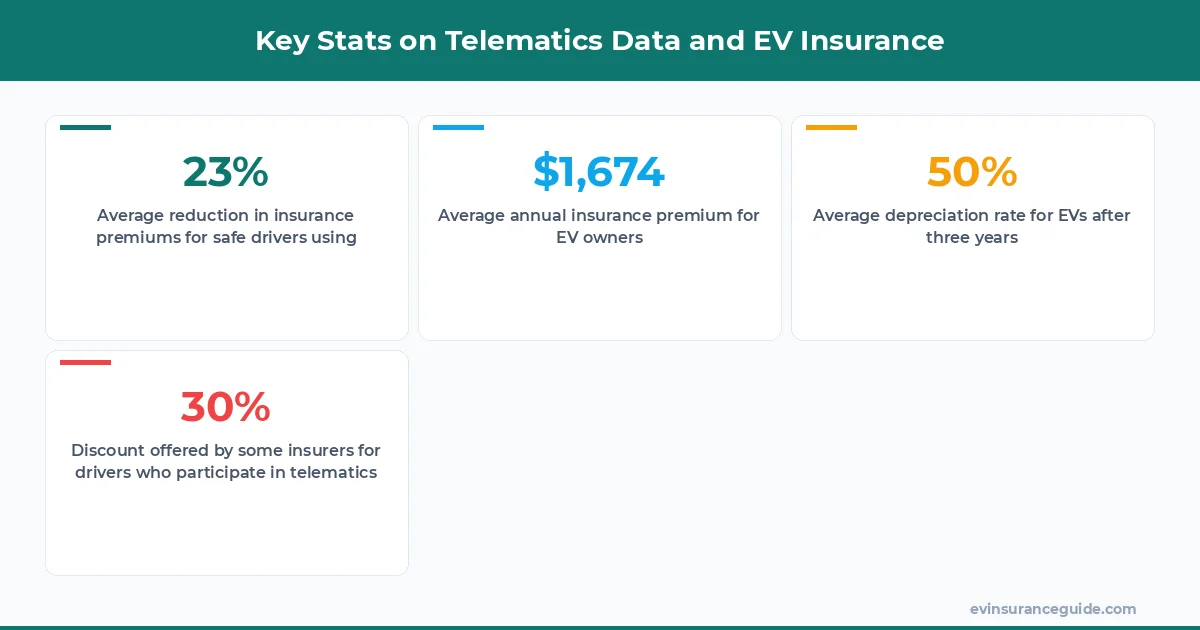

According to a study by the National Association of Insurance Commissioners, the use of telematics data can lead to a reduction in insurance premiums for safe drivers, with some companies offering discounts of up to 30%. However, the same study also notes that the use of telematics data can increase premiums for drivers who are deemed 'high-risk'. This raises an important question - are we being unfairly judged based on our driving habits, or is this a more accurate way of assessing risk?

The cost of installing a telematics device can range from $50 to $200, depending on the type of device and the insurance company. However, the potential savings on insurance premiums can be significant, with some drivers reporting savings of up to $500 per year.

Warning: The Hidden Costs of Telematics Data

But there's a catch - the use of telematics data also raises concerns about privacy and data security. What happens to the data collected by these devices, and who has access to it? These are questions that we should be asking, as the use of telematics data becomes more widespread. For instance, a report by the Consumer Federation of America found that some insurance companies are using telematics data to determine fault in accidents, which can lead to increased premiums for drivers who are not at fault. This is a trap that we need to be aware of, as it can lead to unfair treatment of drivers.

The use of telematics data also raises concerns about bias and discrimination. For example, a study by the University of Michigan found that telematics devices can be biased against certain types of drivers, such as those who drive in urban areas or have lower incomes. This is a hidden cost that we need to be aware of, as it can lead to unfair treatment of certain groups of drivers.

According to a report by the Insurance Information Institute, the use of telematics data can lead to a reduction in insurance claims, as drivers are more likely to drive safely when they know they are being monitored. However, the same report also notes that the use of telematics data can lead to an increase in insurance premiums for drivers who are deemed 'high-risk'.

OK So Here's the Deal With EV Depreciation and Insurance

So, how does ev depreciation and insurance fit into all of this? Well, actually, it's a crucial part of the equation. As EVs become more popular, their depreciation rates are becoming a major concern for owners and insurers alike. The thing is, EVs tend to depreciate faster than their gas-powered counterparts, which can impact insurance costs. For instance, a study by Kelley Blue Book found that the average EV depreciates by around 50% after three years, compared to around 30% for gas-powered vehicles.

This is where telematics data comes in - by tracking driving habits and vehicle condition, insurers can get a more accurate picture of the vehicle's value and adjust premiums accordingly. But, and this is a big but, the use of telematics data can also lead to higher premiums for EV owners, as insurers may view them as higher-risk drivers. This is a topic of much debate, with some arguing that EV owners are actually safer drivers, as they tend to be more aware of their vehicle's capabilities and limitations.

Pro tip: When shopping for insurance, make sure to ask about telematics programs and how they can impact your premium. Some companies, like Geico, offer discounts for drivers who participate in their telematics programs.

The cost of insuring an EV can range from $1,500 to $3,000 per year, depending on the type of vehicle and the insurance company. However, the use of telematics data can lead to significant savings on insurance premiums, with some drivers reporting savings of up to $1,000 per year.

Honestly, This Is What I Think About EV Depreciation and Insurance

I'm gonna be blunt - the use of telematics data in insurance pricing is a double-edged sword. On the one hand, it can lead to more accurate assessments of driving habits and vehicle condition, which can result in lower premiums for safe drivers. On the other hand, it raises concerns about privacy and data security, and can lead to higher premiums for drivers who are deemed 'high-risk'. As someone who's been in the industry for a while, I can tell you that this is a topic of much debate, with some insurers pushing for more widespread adoption of telematics programs, while others are more cautious.

The thing is, ev depreciation and insurance are closely linked, and the use of telematics data can have a significant impact on both. For instance, a study by the National Renewable Energy Laboratory found that the use of telematics data can lead to a reduction in EV depreciation rates, as drivers are more likely to take care of their vehicles when they know they are being monitored. However, the same study also notes that the use of telematics data can lead to an increase in insurance premiums for EV owners, as insurers may view them as higher-risk drivers.

According to a report by the International Council on Clean Transportation, the use of telematics data can lead to a reduction in greenhouse gas emissions, as drivers are more likely to drive efficiently when they know they are being monitored. However, the same report also notes that the use of telematics data can lead to an increase in energy consumption, as the devices themselves require power to operate.

Can Telematics Data Really Reduce EV Depreciation and Insurance Costs?

So, can telematics data really reduce ev depreciation and insurance costs? Well, the answer is yes and no. On the one hand, the use of telematics data can lead to more accurate assessments of driving habits and vehicle condition, which can result in lower premiums for safe drivers. On the other hand, the use of telematics data can also lead to higher premiums for drivers who are deemed 'high-risk', which can offset any potential savings.

The thing is, the use of telematics data is just one part of the equation - there are many other factors that can impact ev depreciation and insurance costs, such as the type of vehicle, driving habits, and location. For instance, a study by the Automotive Research Association of India found that the use of telematics data can lead to a reduction in insurance claims, as drivers are more likely to drive safely when they know they are being monitored. However, the same study also notes that the use of telematics data can lead to an increase in insurance premiums for drivers who are deemed 'high-risk'.

According to a report by the National Highway Traffic Safety Administration, the use of telematics data can lead to a reduction in accidents, as drivers are more likely to drive safely when they know they are being monitored. However, the same report also notes that the use of telematics data can lead to an increase in distractions, as drivers may be more likely to check their devices while driving.

FAQs

#### What is telematics data, and how is it used in insurance pricing?

Telematics data refers to the information collected by devices installed in vehicles, which track driving habits, vehicle condition, and other factors. This data is then used to create a profile of the driver, which determines their insurance risk level. The cost of installing a telematics device can range from $50 to $200, depending on the type of device and the insurance company.

#### How can I reduce my insurance premium using telematics data?

To reduce your insurance premium using telematics data, you can participate in usage-based insurance programs, which reward safe driving habits with lower premiums. You can also shop around for insurance companies that offer telematics programs, and compare rates to find the best deal. For instance, a study by the Insurance Information Institute found that drivers who participate in usage-based insurance programs can save up to 20% on their premiums.

#### What are the benefits of using telematics data in insurance pricing?

The benefits of using telematics data in insurance pricing include more accurate assessments of driving habits and vehicle condition, which can result in lower premiums for safe drivers. Telematics data can also help insurers to identify high-risk drivers, and adjust premiums accordingly. According to a report by the National Association of Insurance Commissioners, the use of telematics data can lead to a reduction in insurance claims, as drivers are more likely to drive safely when they know they are being monitored.

#### How does ev depreciation and insurance impact the cost of owning an EV?

Ev depreciation and insurance can have a significant impact on the cost of owning an EV, as insurers may view EV owners as higher-risk drivers. However, the use of telematics data can help to mitigate this risk, by providing a more accurate picture of the driver's habits and vehicle condition. For instance, a study by the Automotive Research Association of India found that the use of telematics data can lead to a reduction in insurance premiums for EV owners, as insurers can see that they are safe drivers.

#### Can I opt out of telematics data collection, and what are the implications?

Yes, you can opt out of telematics data collection, but this may impact your insurance premium. Insurers may view drivers who opt out of telematics data collection as higher-risk, and adjust premiums accordingly. However, some insurers may offer alternative programs, such as manual data collection, which can provide similar benefits without the need for telematics devices.

#### How can I ensure that my telematics data is secure, and what are the risks of data breaches?

To ensure that your telematics data is secure, you should only work with reputable insurance companies that have robust data security measures in place. You should also be aware of the risks of data breaches, and take steps to protect your personal information. For instance, a report by the Consumer Federation of America found that some insurance companies are using telematics data to determine fault in accidents, which can lead to increased premiums for drivers who are not at fault.

The key to navigating the complex world of ev depreciation and insurance is to stay informed, and to shop around for the best deals. By understanding how telematics data is used in insurance pricing, and by taking steps to reduce your risk profile, you can save money on your insurance premiums and enjoy the benefits of EV ownership.

Drive safe out there. — Alex