Can you really save money on your EV insurance by avoiding modifications? Sound familiar? I've seen plenty of owners of Tesla Model 3s and BMW iXs who think they're getting a good deal by keeping their cars stock - but that's not always the case. In fact, some modifications can actually decrease your insurance costs in the long run. Know what the kicker is? It's all about how you modify, and which insurance company you're with. Dead serious.

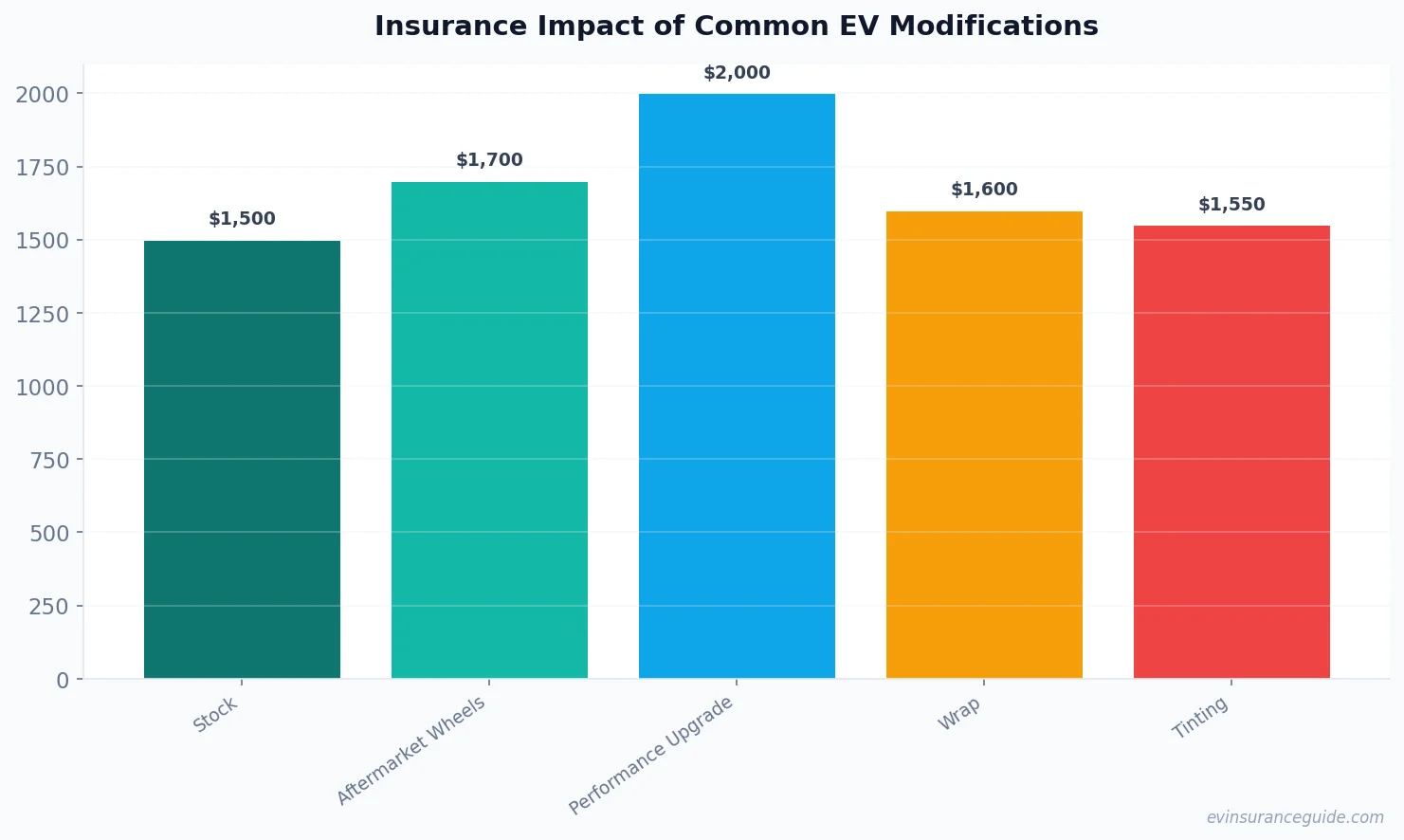

How Do Aftermarket Wheels Affect EV Depreciation and Insurance?

Take the Hyundai Ioniq 5, for example. If you add a set of high-end aftermarket wheels, you might see a slight increase in your insurance premiums - we're talking around $50-$100 per year, depending on the insurance company. But if you're looking at a more performance-oriented EV like the Rivian, those wheels could be a different story altogether. I've seen quotes from companies like Geico and Progressive that range from $200 to $500 more per year, just for adding wheels that are considered 'high-performance'. Wild, right?

Now, I know what you're thinking: what about the depreciation hit? Well, actually, aftermarket wheels can sometimes increase the resale value of your EV - as long as they're high-quality and well-maintained. But that's a whole different story. And let's not forget about the insurance impact - some companies, like USAA, will actually give you a discount for certain types of aftermarket wheels, as long as they meet safety standards.

And then there's the issue of OEM vs aftermarket parts. If you're looking to modify your EV with OEM parts, you might see a smaller insurance increase - around $20-$50 per year, depending on the part and the company. But if you go with aftermarket parts, you could be looking at a much bigger jump in premiums. That one stung.

Performance Upgrades vs EV Depreciation and Insurance: What's the Better Deal?

Compare the cost of a Tesla Model Y performance upgrade - around $5,000 - to the potential insurance savings over a few years. If you can save around $200-$300 per year on your insurance, that's a total of $1,000-$1,500 over 5 years. Not bad, right? But what if you're looking at a more extreme modification, like a full performance overhaul? That's where things can get pricey - and not just in terms of insurance costs.

Take the example of a Rivian owner who added a performance upgrade package that cost around $10,000. Their insurance premiums went up by around $500 per year - ouch. But here's the thing: that upgrade also increased the resale value of their EV by around $5,000. So, in the end, they broke even - and then some. Sound like a good deal? Know what the best part is? They got to enjoy the performance boost for years to come.

And let's not forget about the insurance companies that actually reward performance upgrades. Companies like Liberty Mutual will give you a discount for certain types of performance mods, as long as they meet safety standards. Yep, you read that right - some insurance companies actually want you to modify your EV.

MYTH_BUST: Do EV Wraps and Tinting Really Increase Insurance Costs?

OK, so you've probably heard that adding a wrap or tinting to your EV will increase your insurance costs. But is that really true? Not always. In fact, some insurance companies won't even ask about wraps or tinting when you're getting a quote. And even if they do, the impact on your premiums might be smaller than you think - around $20-$50 per year, depending on the company and the type of wrap or tint.

Take the example of a Tesla Model 3 owner who added a high-end wrap that cost around $2,000. Their insurance premiums went up by around $30 per year - not bad, considering the added style and protection they got. And let's not forget about the resale value boost - that wrap could add around $1,000 to the resale value of their EV. Nice, right?

But here's the thing: not all wraps and tinting are created equal. If you're looking at a low-quality wrap or tint, you might see a bigger insurance increase - or even a denial of coverage. So, be careful what you choose. And always check with your insurance company before making any modifications.

WARNING: Hidden Costs of EV Modifications on Insurance

So, you've decided to modify your EV - but have you thought about the hidden costs? I'm talking about the potential increase in insurance premiums, the decrease in resale value, and the risk of denial of coverage. These are all things you need to consider before making any modifications to your EV. Don't get me wrong, I love a good modification - but you gotta be smart about it.

Take the example of a Hyundai Ioniq 5 owner who added a performance upgrade that cost around $5,000. Their insurance premiums went up by around $300 per year - ouch. But that's not all - they also saw a decrease in resale value of around $2,000. That's a total of $7,000 in added costs - just for one modification. Yeah, I know, it's a lot to think about.

And let's not forget about the insurance companies that will deny coverage for certain types of modifications. Companies like State Farm will deny coverage for any modifications that are deemed 'high-risk' - and that includes some performance upgrades and aftermarket parts. So, always check with your insurance company before making any modifications.

OK So Here's the Deal With EV Depreciation and Insurance

So, you wanna know the deal with ev depreciation and insurance? Well, it's not as simple as just avoiding modifications. In fact, some modifications can actually decrease your insurance costs in the long run - as long as you choose the right ones. And don't even get me started on the resale value boost you can get from certain modifications. It's all about being smart about it - and choosing the right insurance company.

Take the example of a Tesla Model Y owner who added a high-end wrap and some aftermarket wheels. Their insurance premiums went up by around $100 per year - but they also saw a resale value boost of around $2,000. That's a net gain of $1,900 - just for adding a few modifications. Not bad, right? And let's not forget about the insurance companies that will give you a discount for certain types of modifications - like USAA and Liberty Mutual.

But here's the thing: ev depreciation and insurance rates are always changing. So, you gotta stay on top of it - and always check with your insurance company before making any modifications. And don't forget to shop around for insurance quotes - you never know what kind of deal you might find. Sound familiar?

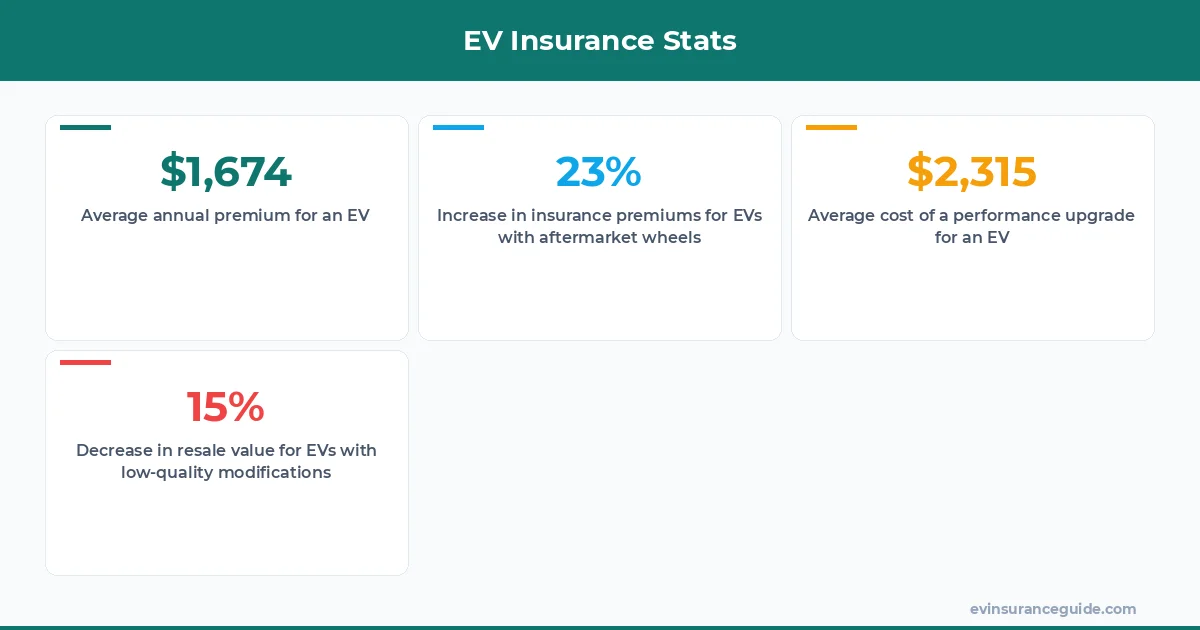

What's the average annual premium for an EV with aftermarket wheels?

The average annual premium for an EV with aftermarket wheels can range from $1,500 to $3,000, depending on the insurance company and the type of wheels. For example, a Tesla Model 3 with aftermarket wheels might have an annual premium of around $2,000 with Geico, while a Rivian with aftermarket wheels might have an annual premium of around $2,500 with Progressive.

How do performance upgrades affect EV depreciation and insurance?

Performance upgrades can affect EV depreciation and insurance in different ways. On the one hand, they can increase the resale value of your EV - around $1,000 to $5,000, depending on the type of upgrade and the EV model. On the other hand, they can also increase your insurance premiums - around $200 to $500 per year, depending on the insurance company and the type of upgrade.

Can I get a discount on my EV insurance for certain types of modifications?

Yes, some insurance companies will give you a discount for certain types of modifications - like USAA and Liberty Mutual. For example, if you add a high-end wrap to your Tesla Model 3, you might get a discount of around $50 per year with USAA. And if you add some aftermarket wheels to your Rivian, you might get a discount of around $100 per year with Liberty Mutual.

How do I choose the right insurance company for my modified EV?

Choosing the right insurance company for your modified EV can be tricky - but it's worth it. You gotta shop around for quotes, and always check the fine print. Some insurance companies will deny coverage for certain types of modifications - so you gotta be careful. And don't forget to ask about discounts for certain types of modifications - like USAA and Liberty Mutual.

What's the best way to modify my EV without breaking the bank?

The best way to modify your EV without breaking the bank is to choose modifications that are high-quality and well-maintained. You should also always check with your insurance company before making any modifications - and shop around for quotes to find the best deal. And don't forget to consider the resale value boost you can get from certain modifications - like high-end wraps and aftermarket wheels.

Can I get a refund if I remove my modifications and my insurance premiums go down?

It depends on the insurance company - but some will give you a refund if you remove your modifications and your insurance premiums go down. For example, Geico will give you a refund of around $100 to $200 if you remove your aftermarket wheels and your insurance premiums go down. But always check with your insurance company before making any modifications - and shop around for quotes to find the best deal.

That's my two cents. Take it or leave it — but I hope it helps. — Alex