Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. I told him it's not uncommon — EV depreciation can be a real kick in the teeth. Sound familiar? You buy a brand new Tesla Model 3, and a year later, it's worth significantly less. Know what the kicker is? Your insurance premium might not drop with it.

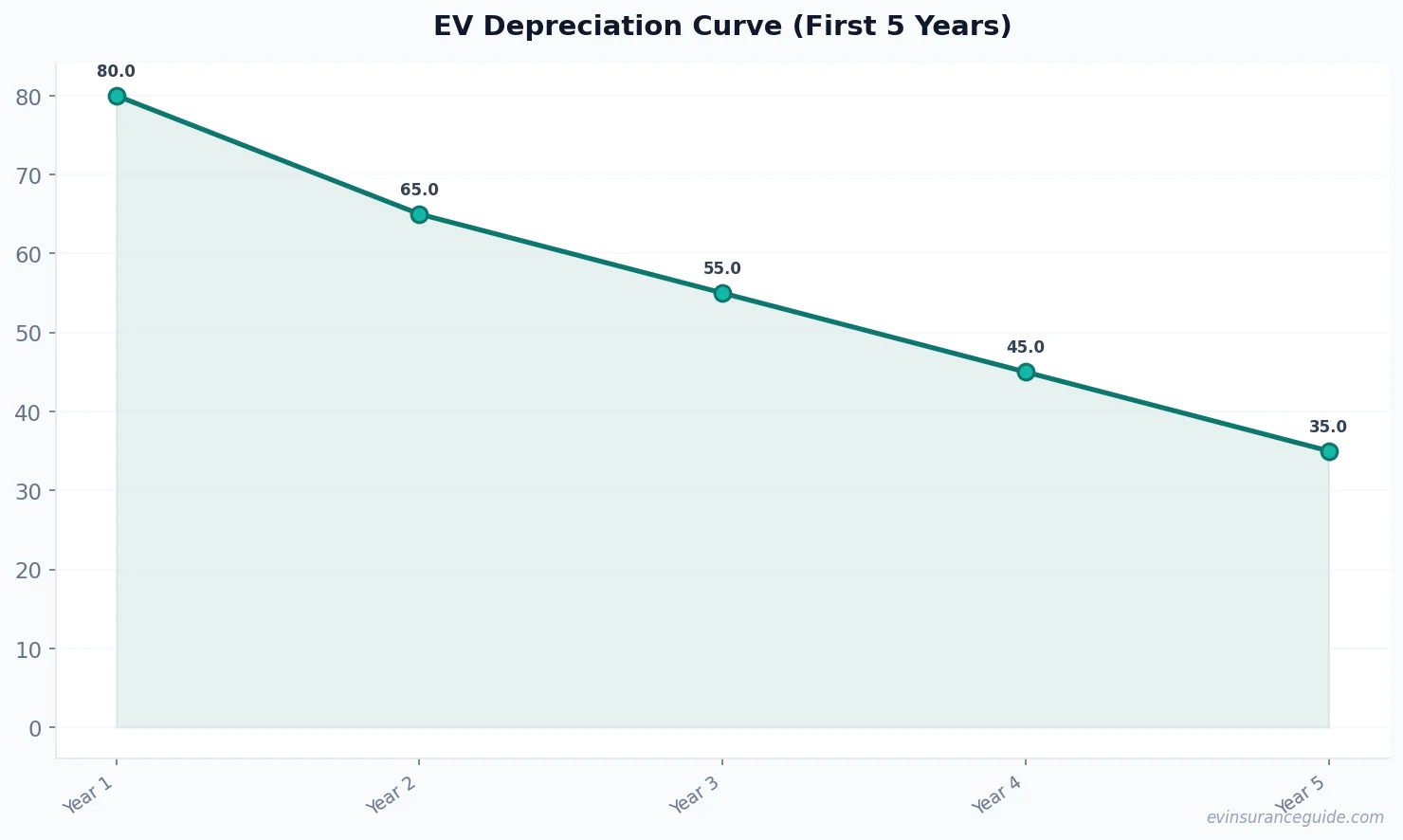

What's the Deal with EV Depreciation?

EV depreciation is a complex beast — it's not just about the car's value dropping over time. There are plenty of factors at play: battery health, software updates, government incentives... the list goes on. Take the BMW iX, for example. It's a fantastic car, but its residual value after 3 years is around 55% — that's a significant hit. And let's not forget the Rivian R1T, which has seen its value drop by as much as 25% in the first year alone. Wild, right?

But here's the thing: not all EVs depreciate at the same rate. The Hyundai Ioniq 5, for instance, has held its value surprisingly well — around 60% after 3 years. That's still a drop, but it's better than some of its competitors. So, what's the secret? Is it the car's design, its features, or something else entirely?

And then there's the issue of insurance premiums. If your car's value drops, you'd expect your premium to drop with it, right? Nope. That's not always the case. Insurers use all sorts of factors to determine your premium, including the car's original purchase price, its safety features, and even your driving history. So, even if your car's value takes a hit, your premium might not budge. That one stung.

Myth-Busting EV Depreciation

Let's bust a myth: EVs depreciate faster than gas-powered cars. Not necessarily true. While it's true that some EVs have seen significant depreciation, others have held their value remarkably well. Take the Tesla Model Y, for example. Its residual value after 3 years is around 65% — that's not much different from some gas-powered cars. And let's not forget that EVs often come with lower maintenance costs, which can help offset the initial purchase price.

But what about battery degradation? Doesn't that affect the car's value? Well, actually, most modern EVs have batteries that are designed to last — we're talking 8-10 years, easy. And even when they do degrade, it's not like the car becomes useless. You'll still get plenty of range, just not as much as you used to. So, while battery degradation is a factor, it's not the only one.

And then there's the issue of supply and demand. If there are more EVs on the market, won't that drive down their value? Maybe, but it's not that simple. See, EVs are still a relatively niche market, and there are plenty of buyers out there who are willing to pay a premium for a good EV. So, even if there are more EVs on the market, the demand is still there.

OK So Here's the Deal With EV Insurance

So, you've got your EV, and you're wondering how to insure it. Well, here's the thing: EV insurance can be tricky. You've got to navigate a complex web of premiums, deductibles, and coverage options. And let's not forget the cost — EV insurance can be pricey, especially if you've got a high-end model like the Porsche Taycan. But don't worry, I've got some tips for you.

First, shop around. Don't just go with the first insurer you find — compare quotes, and see what's out there. You might be surprised at the differences in premium. And don't be afraid to negotiate — insurers want your business, and they might be willing to work with you to get it.

Pro tip: Consider a usage-based insurance policy. These policies track your driving habits and adjust your premium accordingly. If you're a safe driver, you could save big time.

EV Depreciation vs Gas-Powered Cars: What's the Difference?

So, how does EV depreciation compare to gas-powered cars? Well, it's not exactly an apples-to-apples comparison. Gas-powered cars have their own set of depreciation factors — mileage, maintenance costs, fuel efficiency... the list goes on. But if we look at the numbers, EVs seem to be holding their value better than some gas-powered cars. Take the Toyota Camry, for example. Its residual value after 3 years is around 50% — that's lower than some EVs.

But here's the thing: gas-powered cars have a longer history, and their depreciation curves are more established. EVs, on the other hand, are still a relatively new market, and their depreciation curves are still being written. So, while we can compare the two, it's not exactly a fair fight.

And then there's the issue of maintenance costs. EVs are often cheaper to maintain than gas-powered cars, which can help offset the initial purchase price. But gas-powered cars have their own advantages — they're often cheaper to buy upfront, and they have a more established resale market. So, it's a trade-off, really.

Honest Opinion: EV Depreciation is a Real Concern

Let's be real — EV depreciation is a concern. It's not just about the car's value dropping over time; it's about the impact on your insurance premium, your maintenance costs, and your overall ownership experience. So, if you're in the market for an EV, do your research. Look at the depreciation curves, the insurance costs, and the maintenance requirements. It's not just about the car itself; it's about the whole package.

And don't even get me started on the so-called "experts" who claim that EVs are a bad investment. That's just not true. EVs have their advantages, and they're not going away anytime soon. In fact, I'd argue that EVs are the future of the automotive industry. So, if you're thinking of buying an EV, don't let the depreciation scare you off. Just do your research, and you'll be fine.

FAQs

What's the average depreciation rate for EVs?

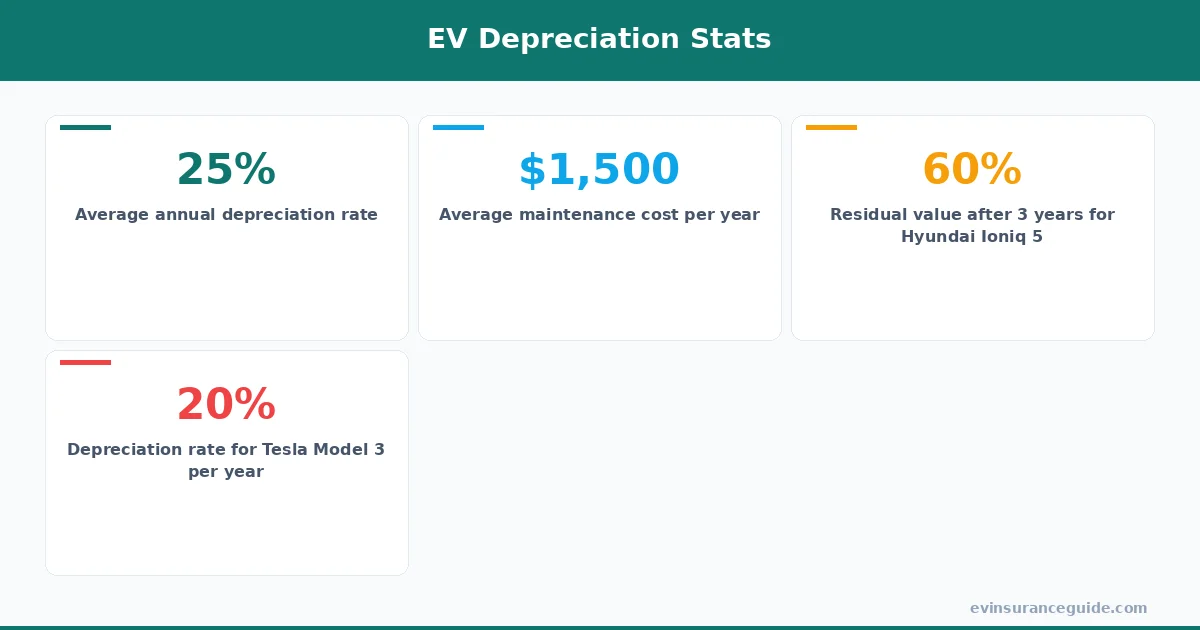

The average depreciation rate for EVs is around 20-30% per year, although this can vary depending on the model and manufacturer. For example, the Tesla Model 3 has a depreciation rate of around 25% per year, while the Hyundai Ioniq 5 has a depreciation rate of around 20% per year.

How does EV depreciation affect insurance premiums?

EV depreciation can affect insurance premiums in a few ways. If the car's value drops, the insurer may reduce the premium, but this is not always the case. Insurers use a variety of factors to determine premiums, including the car's original purchase price, safety features, and driving history.

Can I negotiate my EV insurance premium?

Yes, you can negotiate your EV insurance premium. Shop around, compare quotes, and don't be afraid to ask for a better deal. Some insurers may be willing to work with you to get your business.

What's the best way to mitigate EV depreciation?

The best way to mitigate EV depreciation is to do your research, choose a model with a good residual value, and maintain the car properly. Regular software updates, battery maintenance, and keeping the car in good condition can all help to reduce depreciation.

How does EV depreciation compare to gas-powered cars?

EV depreciation is similar to gas-powered cars in some ways, but there are also some key differences. Gas-powered cars have a longer history, and their depreciation curves are more established. EVs, on the other hand, are still a relatively new market, and their depreciation curves are still being written.

Are EVs a bad investment due to depreciation?

No, EVs are not a bad investment due to depreciation. While depreciation is a concern, EVs have many advantages, including lower maintenance costs, improved performance, and a more sustainable future. With the right research and planning, EVs can be a great investment for many buyers.

That's all from me — go save some money. — Alex