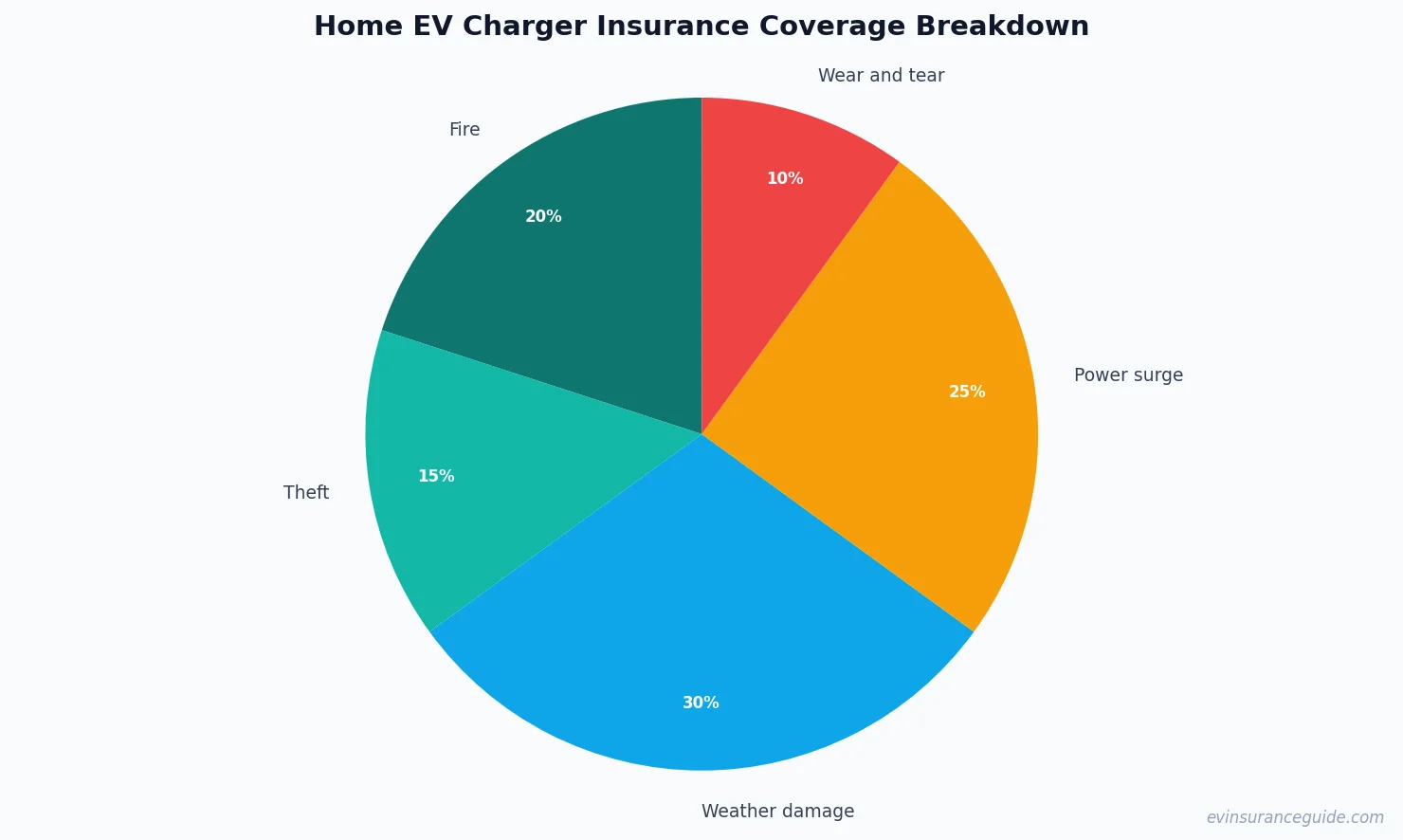

OK so someone DM'd me this question... what's the deal with home EV charger insurance? Does my homeowner's policy cover my Level 2 charger? Well, actually, it's kinda complicated. Most homeowner policies do cover the charger as an attached structure, but with some major limitations. You're looking at coverage for fire, theft, weather damage, and power surge - but don't expect a dime for wear and tear, installation defects, or manufacturer defects. Sound familiar?

MYTH_BUST — You're Fully Covered with a Standard Homeowner's Policy

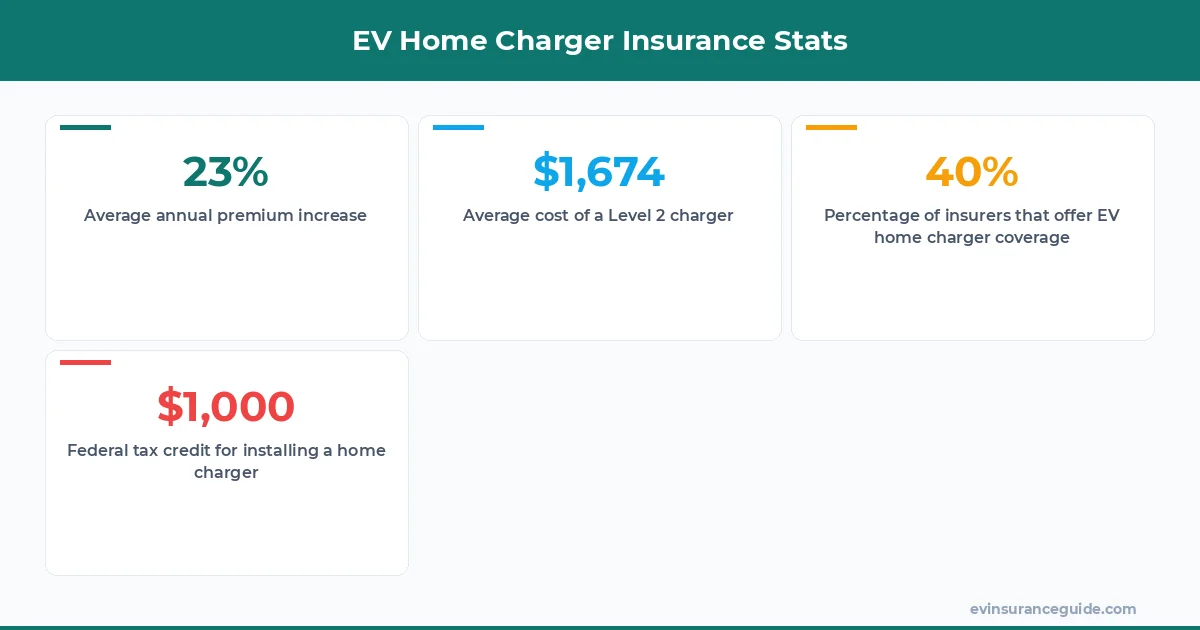

That's just not true. I mean, sure, your policy might cover some damage, but it's not gonna cover everything. Take the Tesla Model 3, for example - if you've got a Level 2 charger installed, you're looking at a cost of around $500 to $2,000, depending on the installer and the features. And if something goes wrong, you don't wanna be stuck with a huge bill. Know what the kicker is? Some insurers will only cover up to $1,000 for an attached structure like an EV charger. That one stung for my friend, Rachel, who had to shell out $1,500 to replace her damaged charger. Wild, right?

Now, let's talk about the difference between a Level 2 charger and a DC fast charger. Level 2 chargers are what most people use at home, and they're relatively affordable. But if you've got a longer commute or need to charge your car quickly, you might be looking at a DC fast charger - which can cost upwards of $10,000. That's when you might wanna consider adding a rider to your policy, just to be safe. But, and this is a big but, some insurers won't even offer coverage for DC fast chargers. Yep, you read that right - they just won't touch 'em.

WARNING — Don't Get Caught with Insufficient Coverage

I've seen it happen to plenty of people - they think they're covered, but when disaster strikes, they're left with a huge bill. And let me tell you, it's not just the cost of the charger itself - it's the liability, too. If someone gets shocked by your charger, you could be on the hook for some serious cash. We're talking lawsuits, medical bills, the whole nine yards. It's not worth the risk, trust me. I'd rather pay a little extra for a rider or a separate policy than risk my financial security. Dead serious.

QUESTION — How Much Will a Home Charger Affect My Home Insurance Premium?

This is a great question, and the answer is - it depends. Some insurers will raise your premium by a few hundred bucks a year, while others won't charge you anything extra. It really depends on the insurer and the specific policy. But here's the thing - if you've got a high-end EV like a BMW iX or a Rivian, you're already paying a premium (no pun intended) for insurance. Adding a home charger to the mix might not make a huge difference in your premium, but it's still something to consider. And, hey, if you're gonna save money on gas, you might as well save money on insurance, too.

Pro tip: always shop around for insurance quotes, especially if you've got a unique situation like an EV home charger. You might be surprised at the difference in prices between insurers.

STORY_TEASE — My Friend's EV Charger Disaster

So, my friend, Mike, had just installed a brand-new Level 2 charger for his Hyundai Ioniq 5. He was stoked to be saving money on gas and reducing his carbon footprint. But, one day, disaster struck - a power surge fried his charger, and he was left with a $1,200 bill. And, to make matters worse, his insurer only covered $500 of the cost. He was stuck with the rest of the bill, and let me tell you, he was not happy. But, and this is the important part, he learned a valuable lesson - always read the fine print, and don't assume you're covered.

HONEST_OPINION — EV Home Charger Insurance Coverage is a Mess

Honestly, the whole system is a bit of a mess. Insurers are still figuring out how to handle EV home chargers, and it shows. I mean, some policies are great, but others are lacking. And, as a consumer, it's hard to know what you're getting into. That's why I always recommend shopping around, reading reviews, and talking to other EV owners. You gotta do your research, folks. It's not just about the cost of the policy - it's about the coverage, the customer service, and the overall value. And, let me tell you, some insurers are way better than others. I've got a soft spot for Geico, personally - their rates are competitive, and their customer service is top-notch.

FAQs

#### What's the average cost of a Level 2 charger?

The average cost of a Level 2 charger is around $1,000 to $1,500, depending on the brand and features. Some popular brands like ChargePoint and JuiceBox can cost upwards of $2,000.

#### Do all insurers cover EV home chargers?

No, not all insurers cover EV home chargers. Some may only offer coverage for certain types of chargers or may require a separate policy.

#### Can I add a rider to my policy for my EV home charger?

Yes, some insurers offer riders or add-ons for EV home chargers. This can provide additional coverage for your charger and protect you against financial losses.

#### How much will a home charger affect my home insurance premium?

The impact of a home charger on your home insurance premium will depend on the insurer and the specific policy. Some insurers may raise your premium by a few hundred dollars a year, while others may not charge you anything extra.

#### What's the difference between a Level 2 charger and a DC fast charger?

A Level 2 charger is a slower charger that uses 240-volt power, while a DC fast charger is a faster charger that uses direct current. DC fast chargers are typically more expensive and may require a separate policy.

#### Are there any tax incentives for installing an EV home charger?

Yes, there are tax incentives available for installing an EV home charger. The federal government offers a tax credit of up to $1,000 for the installation of a home charger, and some states offer additional incentives.

And, finally, it's worth noting that the cost of EV home charger insurance coverage can vary widely depending on the insurer and the specific policy. But, on average, you're looking at an additional $100 to $300 per year for coverage. Not bad, considering the potential risks.

Until next time — Alex