So, you've got an electric vehicle (EV) — maybe a Tesla Model 3 or a Hyundai Ioniq 5 — and you're self-employed. You use it for both personal and business purposes, and you're trying to figure out how to get the right insurance coverage. Well, let me tell you, it's a nightmare. I've been in this industry for five years, and I've seen so many self-employed individuals get taken advantage of by insurance companies. They either overpay for coverage or, worse, get stuck with a policy that doesn't actually cover their business use. Sound familiar?

HONEST_OPINION: EV Insurance After Accident — It's a Wild West

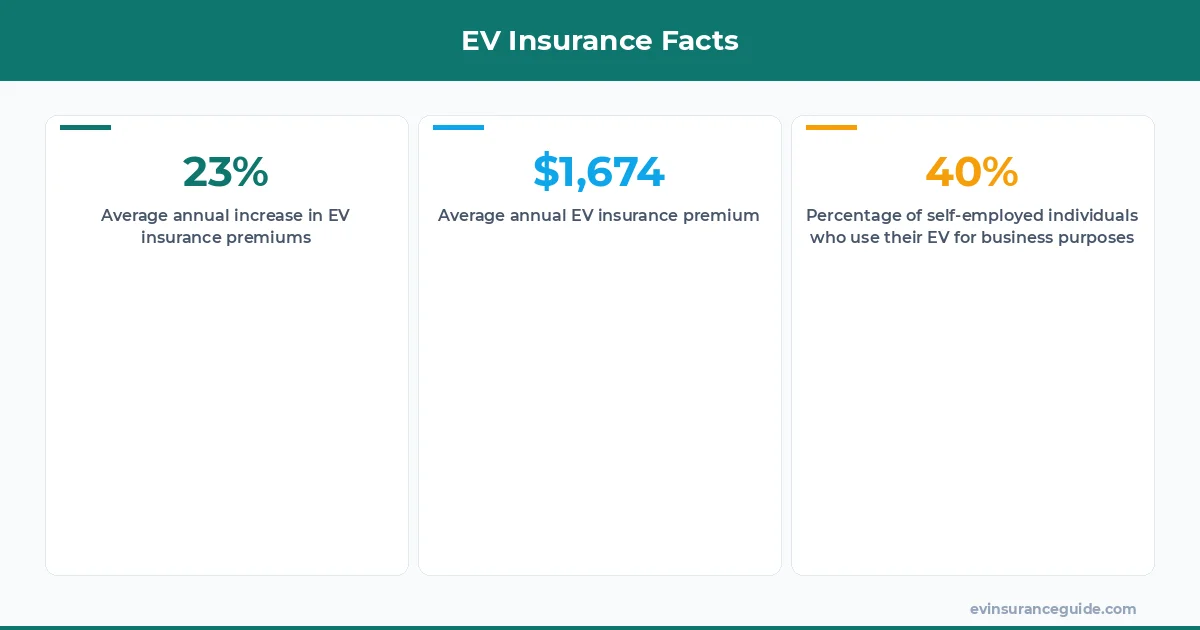

The thing is, most insurance companies don't have a clear understanding of how to handle EV insurance for self-employed individuals. They're still trying to figure out how to price policies, how to assess risk, and how to handle claims. And, honestly, it's a mess. I've seen policies that are overpriced trash, with premiums ranging from $2,000 to $5,000 per year for a single vehicle. And then there are the companies that try to lowball you on coverage, leaving you with a policy that's basically useless. Know what the kicker is? Even if you do get a decent policy, there's no guarantee that the insurance company will actually pay out if you get into an accident. Wild, right?

For example, let's say you're a freelance writer who uses your Tesla Model Y for both personal and business trips. You've got a policy with Geico that covers you for $100,000 in liability, but you're not sure if it'll cover you if you get into an accident while driving to a client meeting. Or, maybe you're a consultant who uses your BMW iX for client visits, and you're trying to figure out how to get the right coverage for your business use. Either way, you're gonna wanna make sure you've got the right policy in place, or you could be stuck with a huge bill if something goes wrong.

That one stung — I had a client who was stuck with a $10,000 bill after an accident because their policy didn't cover business use. And, honestly, it was a nightmare to deal with. The insurance company was giving them the runaround, and it took months to finally get the claim settled. But, hey, at least they learned a valuable lesson — always, always, always read the fine print on your policy.

MYTH_BUST: You Don't Need Separate Personal and Business EV Insurance Policies

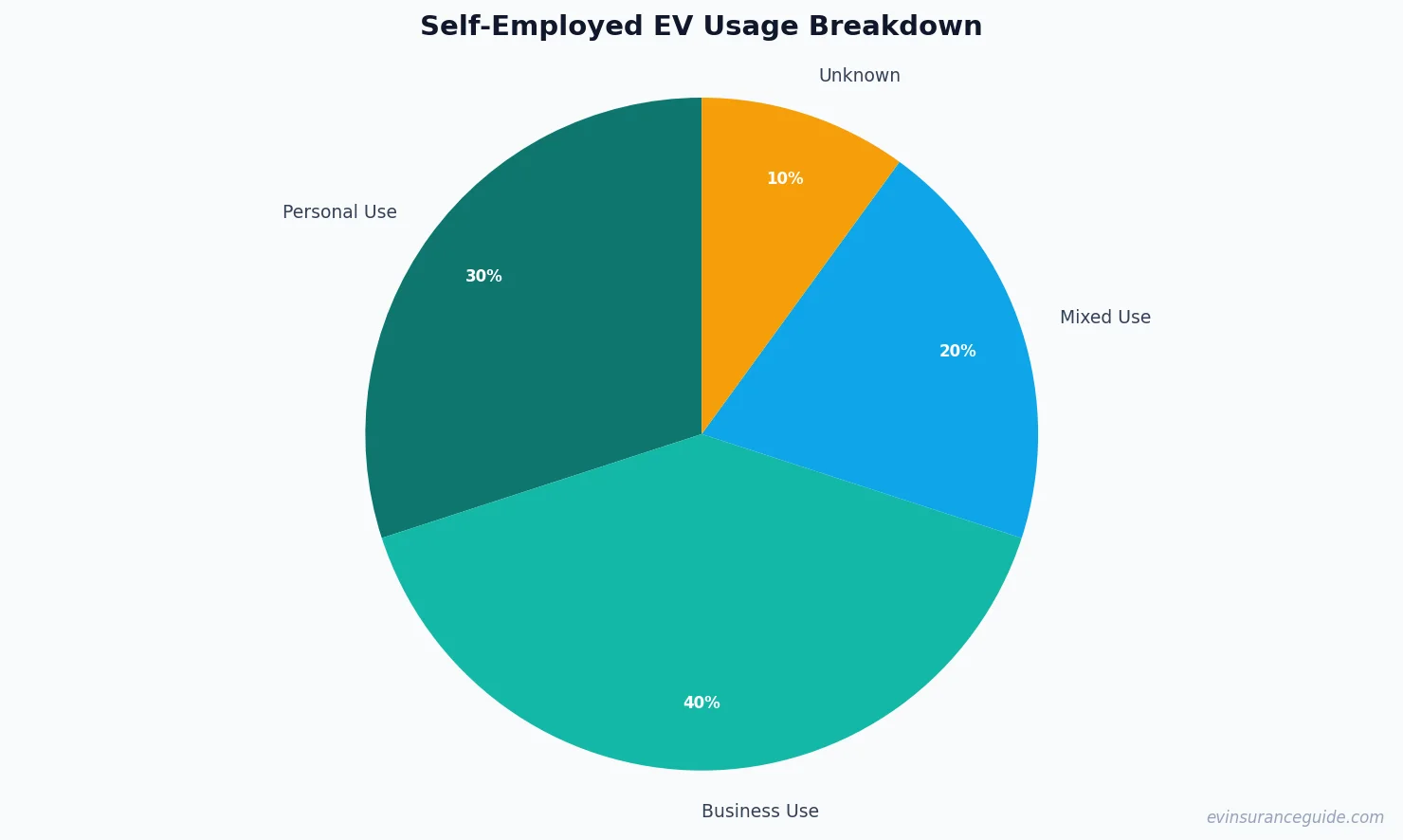

One of the biggest myths out there is that you need separate personal and business EV insurance policies. Nope. Most insurance companies will allow you to get a single policy that covers both personal and business use, as long as you're willing to pay a higher premium. And, honestly, it's usually worth it. I mean, think about it — if you've got two separate policies, you're gonna be paying two separate premiums, and that can add up quickly. But, with a single policy, you can get all the coverage you need in one place, and you'll only have to deal with one insurance company.

For instance, let's say you're a self-employed contractor who uses your Rivian for both personal and business trips. You've got a policy with Progressive that covers you for $200,000 in liability, and it includes a business use endorsement that covers you for up to $10,000 in business-related damages. That way, you've got all the coverage you need in one place, and you can focus on running your business instead of worrying about insurance.

But, here's the thing — you've got to make sure you're getting the right coverage. I mean, if you're using your EV for business purposes, you're gonna need to get a policy that includes a business use endorsement. And, honestly, that can be a real challenge. Some insurance companies will try to sell you a policy that doesn't include the endorsement, or they'll try to charge you an arm and a leg for it. So, you've got to be careful, and you've got to do your research.

Pro tip: always, always, always read the fine print on your policy, and make sure you understand what's covered and what's not. And, if you're not sure, don't be afraid to ask questions.

WARNING: EV Insurance After Accident — Don't Get Caught Off Guard

The thing is, EV insurance after an accident can be a real challenge. I mean, if you get into an accident, you're gonna need to file a claim with your insurance company, and that can be a real hassle. And, honestly, it's not just the claim process that's the problem — it's the fact that insurance companies are still trying to figure out how to handle EVs. They're still trying to determine the value of EVs, and they're still trying to figure out how to assess damage.

So, you've got to be prepared. You've got to make sure you've got all the right documentation, and you've got to make sure you've got a clear understanding of what's covered under your policy. And, honestly, that can be a real challenge. I mean, have you ever tried to read an insurance policy? It's like trying to decipher a foreign language. But, hey, at least you can try.

For example, let's say you're involved in an accident with your Hyundai Ioniq 5, and you need to file a claim with your insurance company. You've got to make sure you've got all the right documentation, including photos of the damage, witness statements, and a police report. And, you've got to make sure you've got a clear understanding of what's covered under your policy, including any deductibles or limitations on coverage.

OK So Here's the Deal With EV Insurance After Accident

OK, so here's the deal — EV insurance after an accident can be a real challenge, but it's not impossible. I mean, if you're prepared, and you've got the right coverage in place, you can navigate the process with ease. And, honestly, it's worth it. I mean, think about it — if you've got an EV, you're already saving money on gas, and you're reducing your carbon footprint. So, why not take the next step and get the right insurance coverage?

For instance, let's say you're a self-employed individual who uses your Tesla Model 3 for both personal and business trips. You've got a policy with State Farm that covers you for $150,000 in liability, and it includes a business use endorsement that covers you for up to $5,000 in business-related damages. That way, you've got all the coverage you need in one place, and you can focus on running your business instead of worrying about insurance.

But, here's the thing — you've got to be careful. I mean, some insurance companies will try to sell you a policy that doesn't include the coverage you need. So, you've got to do your research, and you've got to make sure you're getting the right policy for your needs. And, honestly, that can be a real challenge.

What's the Best Way to Get EV Insurance After Accident?

So, what's the best way to get EV insurance after an accident? Well, honestly, it depends on your situation. I mean, if you're self-employed, you're gonna need to get a policy that includes a business use endorsement. And, if you're using your EV for both personal and business purposes, you're gonna need to get a policy that covers both.

For example, let's say you're a freelance writer who uses your Rivian for both personal and business trips. You've got a policy with Allstate that covers you for $100,000 in liability, and it includes a business use endorsement that covers you for up to $2,000 in business-related damages. That way, you've got all the coverage you need in one place, and you can focus on running your business instead of worrying about insurance.

But, here's the thing — you've got to make sure you're getting the right coverage. I mean, if you're not sure what you need, you should talk to an insurance agent. They can help you figure out what coverage you need, and they can help you find a policy that fits your budget.

FAQs

#### What is EV insurance after accident?

EV insurance after accident refers to the process of filing a claim with your insurance company after you've been involved in an accident with your electric vehicle.

#### How much does EV insurance after accident cost?

The cost of EV insurance after accident can vary depending on a number of factors, including the type of vehicle you have, the extent of the damage, and the insurance company you're working with. On average, you can expect to pay between $500 and $2,000 per year for EV insurance, depending on your situation.

#### Do I need separate personal and business EV insurance policies?

No, you don't need separate personal and business EV insurance policies. Most insurance companies will allow you to get a single policy that covers both personal and business use, as long as you're willing to pay a higher premium.

#### What is a business use endorsement?

A business use endorsement is an addition to your insurance policy that covers you for business-related damages. It's usually required if you're using your EV for business purposes, and it can add an extra $500 to $2,000 per year to your premium.

#### How do I file a claim for EV insurance after accident?

To file a claim for EV insurance after accident, you'll need to contact your insurance company and provide them with documentation of the accident, including photos of the damage, witness statements, and a police report.

#### Can I get EV insurance after accident if I have a bad driving record?

Yes, you can get EV insurance after accident even if you have a bad driving record. However, your premium may be higher, and you may need to work with a specialty insurance company.