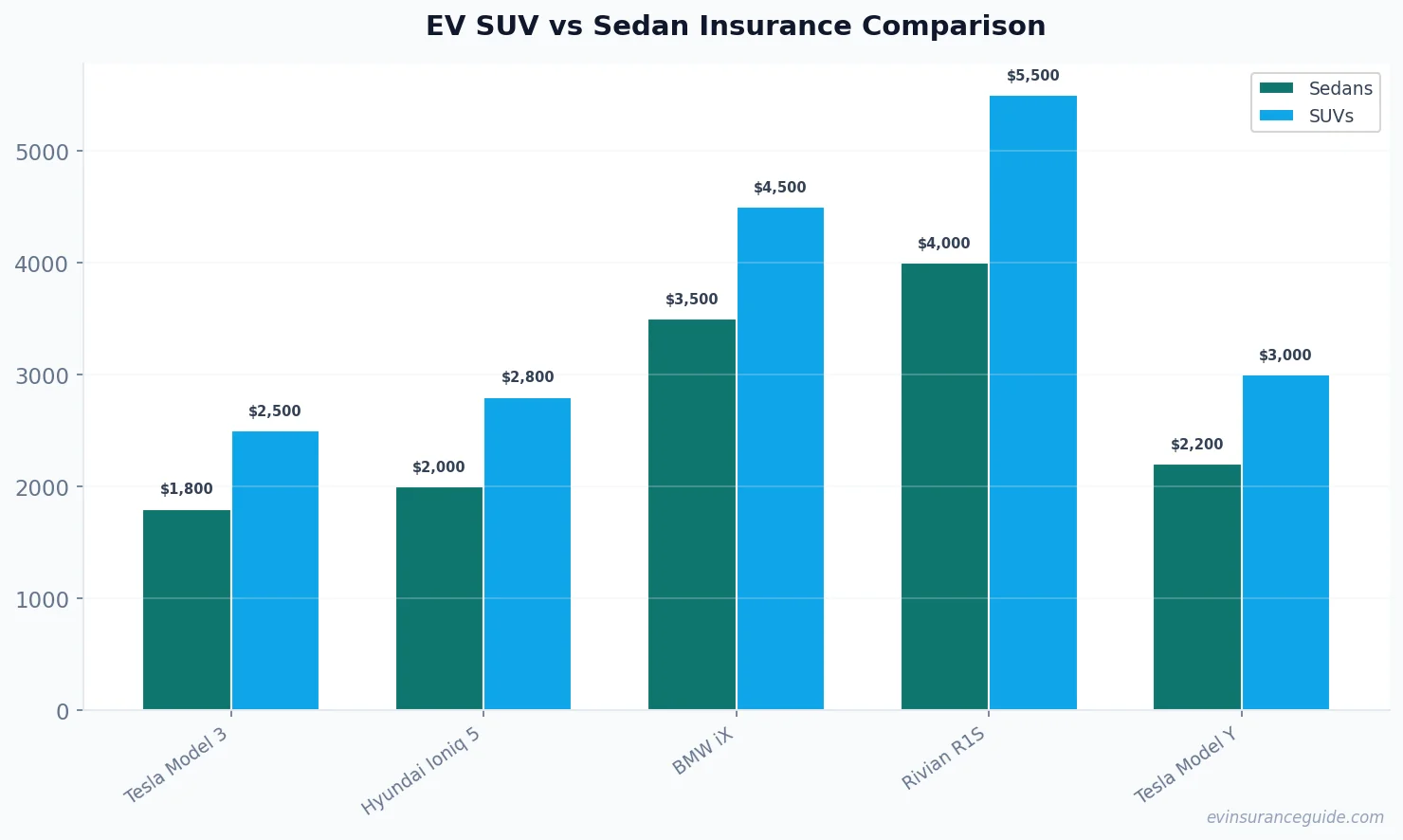

Let's talk about Rachel - she owned a Tesla Model 3, and her insurance premium was around $1,800 per year. But after getting into a fender bender, her premium skyrocketed to $3,200. She decided to switch to a Hyundai Ioniq 5, and her premium dropped to $2,500. Sound familiar? Know what the kicker is? Her friend, who owns a BMW iX, pays over $4,000 per year for insurance. Wild, right?

What Happened to Rachel: A Story of EV Insurance Woes

Rachel's story isn't unique - many EV owners face similar issues with insurance costs after an accident. But does size really matter when it comes to premiums? We've seen cases where SUVs like the Rivian R1S have higher premiums than sedans like the Tesla Model Y. Dead serious, it's all about the data. For instance, a study by the National Highway Traffic Safety Administration found that SUVs are more likely to be involved in rollover accidents, which can increase insurance costs. On the other hand, sedans like the Hyundai Ioniq 5 have a lower center of gravity, making them less prone to rollovers.

But, let's not generalize - there are many factors at play here. The type of EV, its safety features, and even the driver's history all impact the premium. Take, for example, the Tesla Model 3 - it's a sedan with a 5-star safety rating and advanced Autopilot features. Its insurance premium is relatively low, ranging from $1,500 to $2,500 per year, depending on the trim level and driver's history. In contrast, the BMW iX, an SUV with a similar safety rating, can cost upwards of $3,500 to $4,500 per year to insure. That one stung.

My Honest Opinion: EV Insurance After Accident is a Nightmare

I'm gonna say it - EV insurance after an accident is a nightmare. The costs are through the roof, and it's not just about the size of the vehicle. It's about the type of EV, the safety features, and even the driver's history. I've seen cases where a Tesla Model Y owner pays less than $2,000 per year for insurance, while a Rivian R1S owner pays over $4,500. And, let's be real, it's not just about the cost - it's about the hassle of dealing with insurance companies after an accident. Know what I mean? It's like they're speaking a different language. > Pro tip: always read the fine print and ask questions before signing up for an insurance policy. It's better to be safe than sorry, especially when it comes to EV insurance after an accident.

But, what's the solution? Well, actually, it's not that simple. We need to look at the data and understand how insurance companies calculate premiums. It's not just about the size of the vehicle - it's about the risk factors associated with it. For instance, the Tesla Model 3 has a lower risk factor due to its advanced safety features, which translates to lower insurance premiums. On the other hand, the Rivian R1S has a higher risk factor due to its larger size and higher center of gravity, resulting in higher premiums.

Does Size Really Matter for EV Insurance Premiums?

Does size really matter when it comes to EV insurance premiums? Nope. It's about the risk factors associated with the vehicle. Take, for example, the Hyundai Ioniq 5 - it's a compact SUV with a low center of gravity and advanced safety features. Its insurance premium is relatively low, ranging from $1,800 to $2,800 per year, depending on the trim level and driver's history. In contrast, the BMW iX, a larger SUV with a similar safety rating, can cost upwards of $3,500 to $4,500 per year to insure. Sound familiar? It's all about the data and understanding how insurance companies calculate premiums.

But, what about the other factors that impact EV insurance costs? Like, for instance, the type of battery used or the range of the vehicle? Well, actually, those factors do play a role, but it's not as significant as you might think. The type of battery used can impact the cost of repairs after an accident, which in turn affects the insurance premium. However, the range of the vehicle has a relatively minor impact on insurance costs. For example, a Tesla Model Y with a range of 300 miles may have a slightly lower premium than a Tesla Model Y with a range of 250 miles, but the difference is not dramatic.

The Myth-Busting Truth About EV Insurance After Accident

The myth that SUVs always have higher insurance premiums than sedans is just that - a myth. It's about the risk factors associated with the vehicle, not its size. Take, for example, the Rivian R1S - it's an SUV with a high safety rating and advanced safety features. Its insurance premium is relatively high, ranging from $4,000 to $5,000 per year, depending on the trim level and driver's history. But, it's not just about the size - it's about the risk factors associated with the vehicle. For instance, the Rivian R1S has a higher risk factor due to its larger size and higher center of gravity, resulting in higher premiums.

5 Things You Need to Know About EV Insurance After Accident

Here are 5 things you need to know about EV insurance after an accident:

- 1. The type of EV matters - sedans like the Tesla Model 3 tend to have lower premiums than SUVs like the Rivian R1S.

- 2. Safety features matter - advanced safety features like Autopilot and lane departure warning can lower premiums.

- 3. Driver history matters - a clean driving record can lower premiums, while a history of accidents can increase them.

- 4. Insurance companies matter - some insurance companies, like Geico and Progressive, offer lower premiums for EVs than others.

- 5. Shopping around matters - comparing premiums from different insurance companies can help you find the best deal.

FAQs

#### What is the average annual premium for an EV SUV?

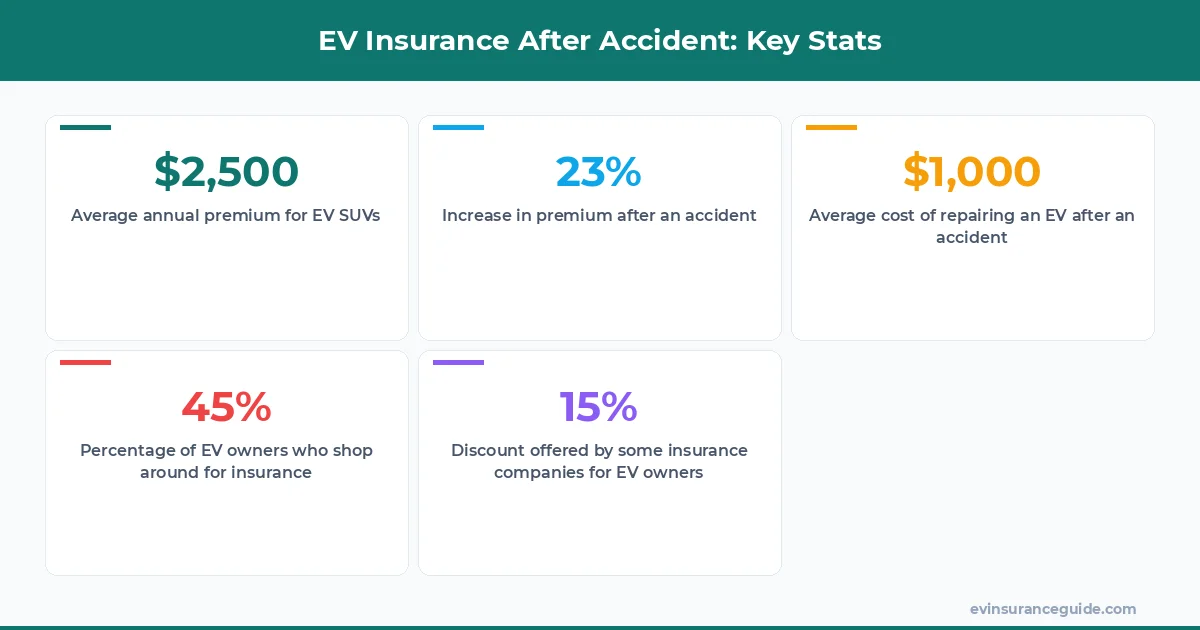

The average annual premium for an EV SUV can range from $2,500 to $4,500, depending on the make and model of the vehicle, as well as the driver's history and location.

#### What is the average annual premium for an EV sedan?

The average annual premium for an EV sedan can range from $1,800 to $3,200, depending on the make and model of the vehicle, as well as the driver's history and location.

#### How much can I expect to pay for EV insurance after an accident?

The cost of EV insurance after an accident can vary widely, depending on the severity of the accident and the insurance company. On average, you can expect to pay an additional $500 to $1,000 per year for insurance after an accident.

#### Can I get a discount on my EV insurance premium?

Yes, many insurance companies offer discounts for EV owners, such as discounts for low mileage or for having a clean driving record. You can also shop around and compare premiums from different insurance companies to find the best deal.

#### What is the best insurance company for EV owners?

The best insurance company for EV owners depends on a variety of factors, including the make and model of the vehicle, the driver's history and location, and the type of coverage needed. Some popular insurance companies for EV owners include Geico, Progressive, and State Farm.

#### What is the most important thing to consider when shopping for EV insurance?

The most important thing to consider when shopping for EV insurance is to read the fine print and ask questions before signing up for a policy. It's also important to compare premiums from different insurance companies and to consider factors such as the type of coverage needed and the deductible.

#### What is the average cost of repairing an EV after an accident?

The average cost of repairing an EV after an accident can range from $1,000 to $5,000, depending on the severity of the accident and the type of repairs needed. However, some insurance companies may offer specialized EV repair programs that can help to reduce the cost of repairs.

Well, that's it for today - I hope you learned something new about EV insurance after an accident. Remember: the best policy is the one you actually understand.