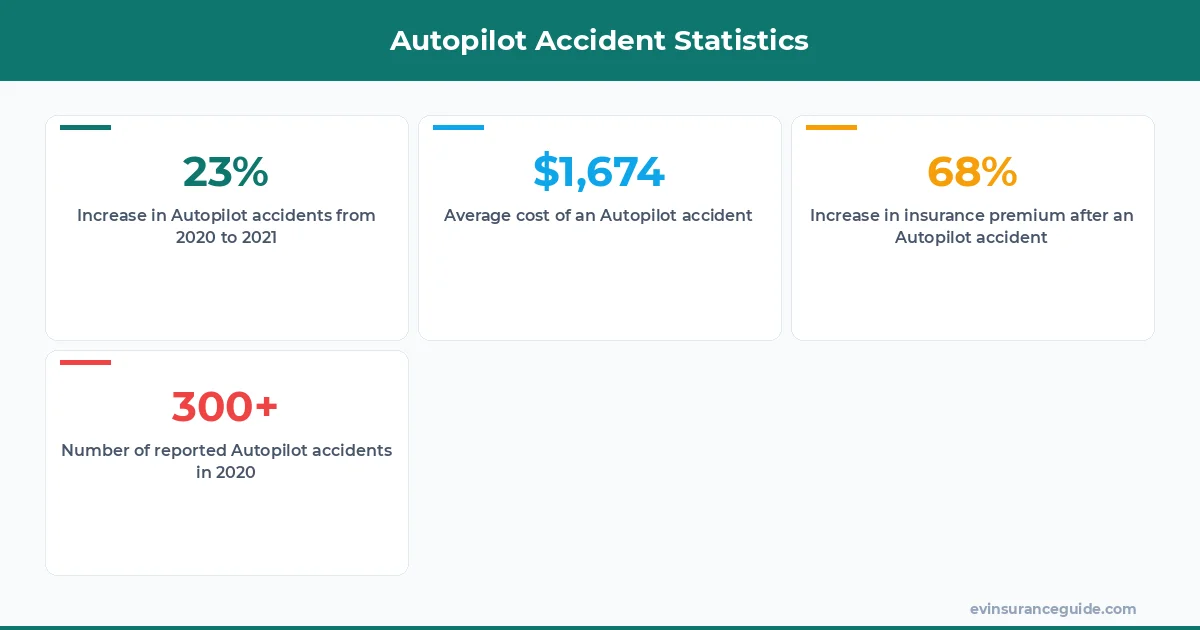

So my buddy, Rachel, she's a huge Tesla fan - had a Model 3, then upgraded to the Model Y. She's all about that Autopilot life. Before she switched to an EV insurance provider that actually understands Autopilot, her premium was around $2,500 a year. And then she had an accident - not even her fault, but the other driver wasn't paying attention. Fast forward, her premium jumped to $4,200. That's an 68% increase, just like that. But then she switched to a provider that specializes in EV insurance and Autopilot accidents... and her premium dropped to $2,800. Still higher than before, but way better than what she was paying. That's the kinda difference the right insurance can make.

A Tesla Autopilot Story Tease

You know, people always ask me: what's the worst that could happen with Autopilot? Well, let me tell you - I've seen some pretty wild cases. Like the time a Tesla Model S on Autopilot rear-ended a parked fire truck... or when a Model 3 on Autopilot crashed into a concrete divider. Sound familiar? These accidents are rare, but they do happen. And when they do, it's a whole different ball game - liability-wise, I mean. Know what the kicker is? The current legal framework still puts the blame on the driver, even if the car was driving itself. That's right - with Level 2 systems like Tesla Autopilot or GM Super Cruise, the driver is still responsible. But for how long?

The thing is, as Autopilot technology improves, we're gonna see more and more accidents where the car was driving itself. And that's when things get complicated. I mean, who's liable then? The manufacturer? The driver? It's a gray area, and one that's gonna be decided in court, mark my words. Take the case of a Tesla Model 3 owner who was using Autopilot when his car crashed into a tree. The driver claimed the Autopilot system was at fault, but Tesla said the driver was still responsible. That one stung - the driver ended up with a $10,000 repair bill.

OK So Here's the Deal With EV Insurance and Autopilot Accidents

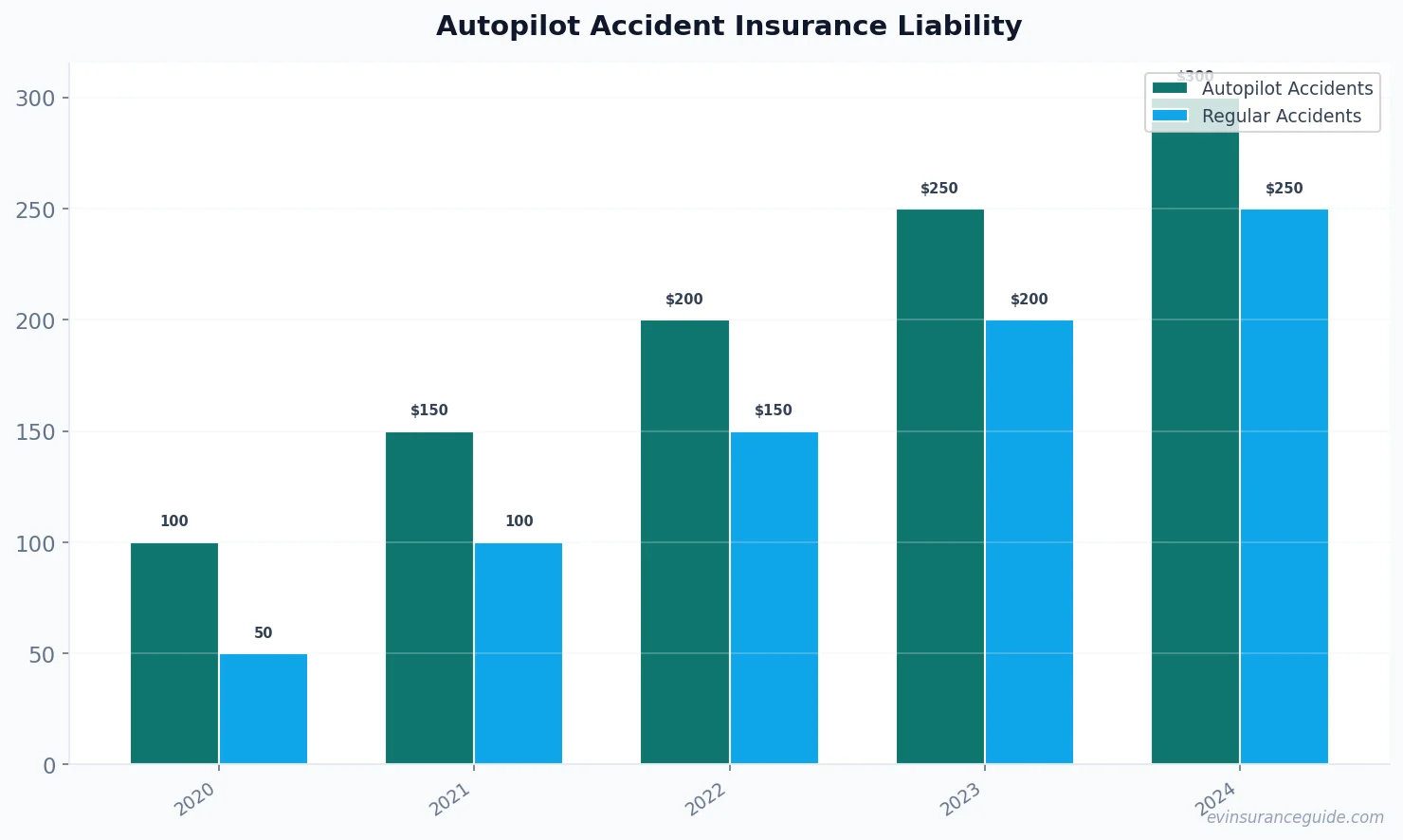

So, you're probably wondering: how do Autopilot-involved accidents affect your premium? Well, it's not pretty. According to Tesla's own insurance claims data, Autopilot accidents are more expensive to repair than regular accidents. Like, a lot more expensive - we're talking $5,000 to $10,000 more, on average. And that's because Autopilot-related accidents often involve more severe damage to the car's advanced safety features, like sensors and cameras. For example, a study by the Insurance Institute for Highway Safety found that Tesla vehicles equipped with Autopilot had a higher claim frequency for certain types of accidents, like rear-end collisions.

Now, I know what you're thinking: but Alex, I've got a BMW iX with Active Driving Assistant - that's basically the same thing as Autopilot, right? Nope. While it's true that both systems use a combination of cameras, sensors, and mapping data to enable semi-autonomous driving, there are some key differences. For one, BMW's system is more limited in its capabilities - it can't change lanes or merge onto highways like Autopilot can. And two, the insurance implications are different - at least, for now. That's because BMW's system is still considered a Level 2 system, just like Autopilot, but with some key differences in how it's implemented.

But here's the thing: as EVs become more mainstream, we're gonna see more and more insurance providers specializing in EV insurance and Autopilot accidents. And that's a good thing - it means more competition, better rates, and more expertise. For example, some insurance providers are now offering discounts for EV owners who use Autopilot or other semi-autonomous driving systems. It's a win-win - the driver gets a safer, more convenient driving experience, and the insurance provider gets a lower-risk customer.

Warning: The Current Legal Framework is a Trap

So, you're driving along, Autopilot engaged, and suddenly - crash. The other driver wasn't paying attention, but your car was driving itself. Who's liable? You are, according to the current legal framework. That's right - even if the car was driving itself, the driver is still responsible. And that's a problem, because it means that drivers are on the hook for accidents that aren't entirely their fault. For example, a study by the National Highway Traffic Safety Administration found that in 2020, there were over 300 reported accidents involving vehicles with semi-autonomous driving systems like Autopilot. And in many of those cases, the driver was not at fault - but they still ended up with higher insurance premiums.

But it gets worse. Because if you're in an accident while using Autopilot, your insurance premium is gonna go up - way up. Like, $1,000 to $2,000 more per year, easy. And that's because insurance providers see Autopilot accidents as higher-risk - even if the accident wasn't your fault. It's like, you're being penalized for using a safety feature that's supposed to make driving safer. Wild, right? And it's not just the premium increase - it's also the potential long-term effects on your insurance rates. For example, if you have a history of Autopilot-related accidents, you may find it harder to get insurance in the future - or you may have to pay more for it.

Pro tip: if you're in an Autopilot accident, make sure to document everything - including the Autopilot log data. This can help establish that the accident wasn't your fault, and may even help reduce your insurance premium increase.

A Comparison: Level 2 vs Level 3+ Autopilot Systems

So, what's the difference between Level 2 and Level 3+ Autopilot systems? Well, it's pretty simple - Level 2 systems, like Tesla Autopilot or GM Super Cruise, are considered semi-autonomous. They can handle some driving tasks, like steering and acceleration, but the driver is still responsible for monitoring the road and taking control if needed. Level 3+ systems, on the other hand, are considered fully autonomous - they can handle all driving tasks, without any human intervention. And that changes everything - liability-wise, I mean.

For example, the Hyundai Ioniq 5 has a Level 2 Autopilot system, while the Rivian R1T has a more advanced Level 3 system. And that's a key difference - because with Level 3+ systems, the manufacturer is more likely to be held liable in the event of an accident. In fact, some manufacturers are already taking steps to address this issue - like Tesla, which has announced plans to introduce a new, more advanced Autopilot system that will be capable of fully autonomous driving.

An Honest Opinion: The Future of Liability

So, what's the future of liability when it comes to EV insurance and Autopilot accidents? In my opinion, it's clear - manufacturers are gonna be held more accountable. I mean, if a car is driving itself, and it gets into an accident, who's responsible? The manufacturer, that's who. It's like, they're the ones who designed the system, they're the ones who tested it - they're the ones who should be held liable. And that's gonna change the game - it's gonna make manufacturers more careful, more diligent, when it comes to testing and implementing Autopilot systems.

And it's not just about liability - it's also about safety. I mean, if manufacturers are held accountable for Autopilot accidents, they're gonna be more likely to invest in safety features, like better sensors and cameras. And that's a win-win - it's a win for drivers, who get a safer, more convenient driving experience, and it's a win for manufacturers, who get to reduce their liability and improve their reputation.

FAQs

#### What is the current legal framework for EV insurance and Autopilot accidents?

The current legal framework still puts the blame on the driver, even if the car was driving itself. However, this is likely to change as Autopilot technology improves and more accidents occur.

#### How do Autopilot-involved accidents affect my premium?

Autopilot accidents are more expensive to repair than regular accidents, and your premium is likely to increase - by $1,000 to $2,000 more per year, easy.

#### What's the difference between Level 2 and Level 3+ Autopilot systems?

Level 2 systems, like Tesla Autopilot or GM Super Cruise, are considered semi-autonomous, while Level 3+ systems are considered fully autonomous.

#### Can I get a discount on my EV insurance premium if I use Autopilot?

Some insurance providers are now offering discounts for EV owners who use Autopilot or other semi-autonomous driving systems. It's a win-win - the driver gets a safer, more convenient driving experience, and the insurance provider gets a lower-risk customer.

#### How can I protect myself legally and financially in the event of an Autopilot accident?

Make sure to document everything, including the Autopilot log data, and consider investing in a dash cam or other safety features. You should also review your insurance policy carefully to understand what's covered and what's not.

#### What's the future of liability when it comes to EV insurance and Autopilot accidents?

In my opinion, manufacturers are gonna be held more accountable - they're the ones who designed the system, they're the ones who tested it, and they're the ones who should be held liable.

Cheers from the EV insurance trenches.

— Alex