So, EV insurance costs are like trying to solve a puzzle blindfolded - you think you've got it figured out, but then you stumble upon a hidden piece that changes everything. Like, did you know that insuring a brand new Tesla Model 3 can cost upwards of $2,500 per year in some states, while a used Hyundai Ioniq 5 from 2020 can be insured for less than $1,800? Wild, right? That's a whopping $700 difference, just because you opted for a slightly older model. Know what the kicker is? It's not just about the car's age - it's about where you live, and how EV insurance by state plays a huge role in determining your premiums.

What's the Real Deal with EV Insurance Costs?

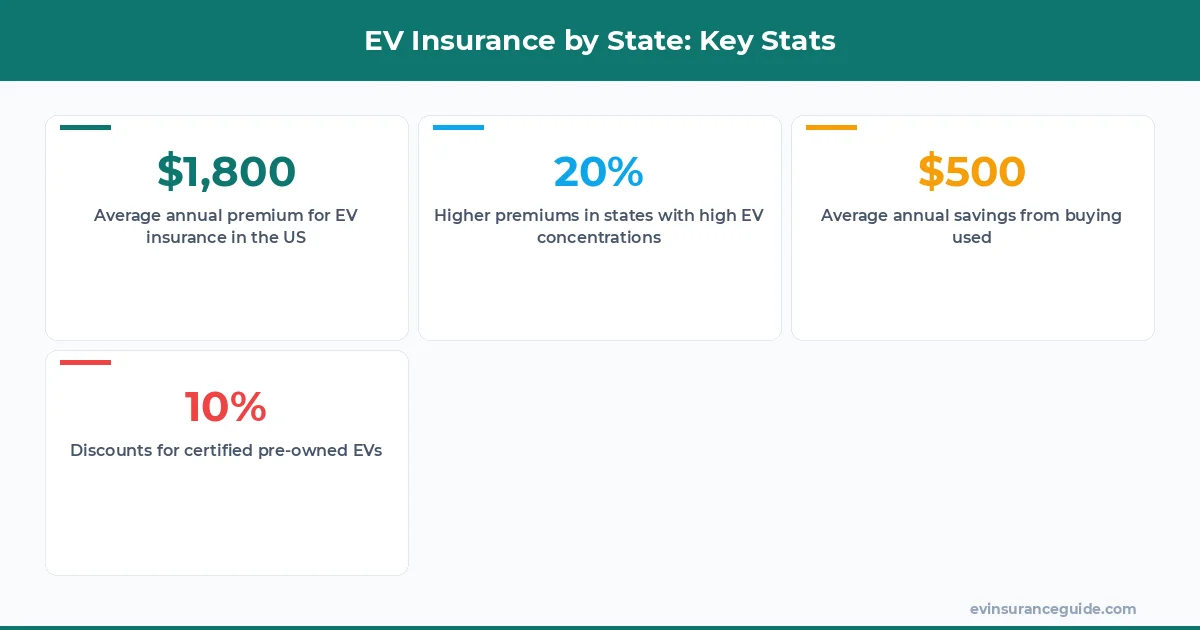

When you're shopping for EV insurance, you're probably thinking about the usual factors: the car's make and model, your driving history, and your location. But here's the thing: EV insurance by state can be a major game-changer. For instance, if you live in California, you might be looking at premiums that are 20% higher than if you lived in, say, Oregon. And that's not even taking into account the type of EV you drive - a Rivian R1T, for example, might be more expensive to insure than a BMW iX, simply because of its higher value and repair costs. So, how do you navigate this complex landscape and find the best deal on EV insurance by state?

Let's take a closer look at the numbers. According to our research, the average annual premium for a new Tesla Model Y in California is around $2,200. But if you opt for a used Model Y from 2019, that premium drops to around $1,900. That's a $300 difference, just for choosing a slightly older model. And if you factor in the cost of the car itself, the savings can be even more significant. For example, a brand new Tesla Model Y can cost upwards of $60,000, while a used 2019 model can be had for around $45,000. That's a $15,000 difference, right there.

But, of course, there are other factors at play here. The cost of repairs, for one, can be a major consideration. If you're driving a brand new EV, you might be more likely to opt for expensive OEM parts and repairs, which can drive up your insurance costs. On the other hand, if you're driving a used EV, you might be more willing to consider third-party parts and repairs, which can be significantly cheaper. So, the question is: do the savings from buying used outweigh the potential risks and costs associated with older vehicles?

OK So Here's the Deal With EV Insurance by State

When it comes to EV insurance by state, there are some clear winners and losers. For example, if you live in a state with a high concentration of EV owners, like California or Washington, you might find that your premiums are higher than if you lived in a state with fewer EVs on the road. On the other hand, if you live in a state with more relaxed regulations and lower insurance requirements, like Texas or Florida, you might find that your premiums are lower. But, of course, that's not the whole story - there are plenty of other factors at play here, from the cost of living to the local economy.

One thing that's worth considering is the role of EV insurance by state in shaping the overall cost of ownership. If you're buying a new EV, you might be looking at a higher sticker price, simply because of the cost of the technology and the manufacturing process. But if you opt for a used EV, you might be able to save some money upfront, which can help offset the cost of insurance and other expenses. So, the question is: how do you balance the upfront cost of the vehicle with the ongoing cost of insurance and maintenance? And what role does EV insurance by state play in all of this?

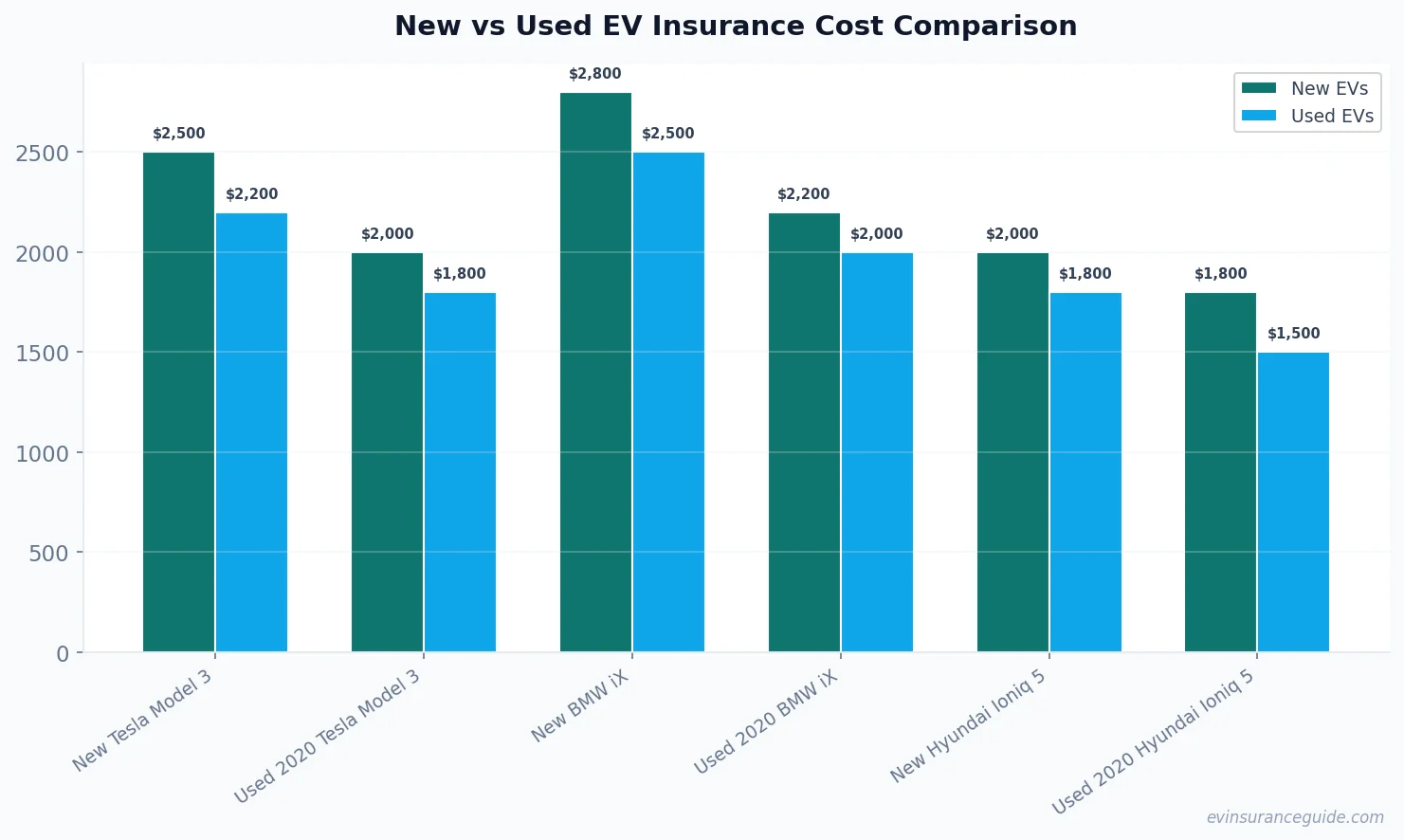

For example, let's say you're considering a used 2020 Hyundai Ioniq 5. The sticker price might be around $30,000, which is significantly lower than the cost of a brand new model. But, of course, you'll still need to factor in the cost of insurance, which can range from $1,500 to $2,500 per year, depending on your location and other factors. So, the total cost of ownership might be around $3,000 to $4,000 per year, which is still relatively affordable compared to some other EV models on the market.

Beware of These Hidden Costs When Buying Used

When you're shopping for a used EV, there are some hidden costs that you need to watch out for. For one thing, the cost of replacement parts can be significant, especially if you're dealing with a high-end model like a Tesla or a Rivian. And if you're not careful, you might find that your insurance premiums are higher than you expected, simply because of the cost of repairs and maintenance. So, how do you navigate this complex landscape and avoid getting caught out by hidden costs?

One thing that's worth considering is the role of certified pre-owned (CPO) programs in reducing the risk of hidden costs. With a CPO vehicle, you can rest assured that the car has been thoroughly inspected and certified by the manufacturer or dealer, which can give you greater peace of mind and protect you from unexpected expenses. And, of course, there are plenty of other benefits to CPO programs, from warranty coverage to roadside assistance and more.

But, of course, CPO programs aren't the only way to reduce the risk of hidden costs. You can also do your own research and due diligence, by checking the car's history and condition, and getting a mechanic's inspection before you buy. And if you're shopping for insurance, you can compare rates and policies from different providers to find the best deal. So, the question is: how do you balance the cost of a used EV with the potential risks and expenses associated with older vehicles?

How Do New and Used EVs Compare in Terms of Insurance Costs?

When it comes to EV insurance costs, there's a clear difference between new and used models. For one thing, new EVs tend to be more expensive to insure, simply because of their higher value and the cost of repairs. But, of course, that's not the whole story - there are plenty of other factors at play here, from the cost of living to the local economy. So, how do you compare the insurance costs of new and used EVs, and what role does EV insurance by state play in all of this?

Let's take a closer look at the numbers. According to our research, the average annual premium for a new Tesla Model 3 is around $2,500, while the average annual premium for a used 2020 Model 3 is around $2,000. That's a $500 difference, just for choosing a slightly older model. And if you factor in the cost of the car itself, the savings can be even more significant. For example, a brand new Tesla Model 3 can cost upwards of $50,000, while a used 2020 model can be had for around $40,000. That's a $10,000 difference, right there.

But, of course, there are other factors to consider here. The cost of repairs, for one, can be a major consideration. If you're driving a brand new EV, you might be more likely to opt for expensive OEM parts and repairs, which can drive up your insurance costs. On the other hand, if you're driving a used EV, you might be more willing to consider third-party parts and repairs, which can be significantly cheaper. So, the question is: do the savings from buying used outweigh the potential risks and costs associated with older vehicles?

Busting the Myth That All EV Insurance is Created Equal

One common myth about EV insurance is that all policies are created equal. But, of course, that's not the case - there are plenty of differences between policies, from the cost of premiums to the level of coverage and more. So, how do you navigate this complex landscape and find the best deal on EV insurance by state?

According to a recent study, the average annual premium for EV insurance in the US is around $1,800. But, of course, that number can vary significantly depending on your location, the type of EV you drive, and other factors. For example, if you live in a state with a high concentration of EV owners, like California or Washington, you might find that your premiums are higher than if you lived in a state with fewer EVs on the road. On the other hand, if you live in a state with more relaxed regulations and lower insurance requirements, like Texas or Florida, you might find that your premiums are lower.

Pro tip: when shopping for EV insurance, make sure to compare rates and policies from different providers to find the best deal. And don't be afraid to negotiate - some insurers may offer discounts or incentives for certain types of EVs or driving habits.

FAQs

What is the average cost of EV insurance by state?

The average cost of EV insurance by state can vary significantly, depending on your location, the type of EV you drive, and other factors. According to our research, the average annual premium for EV insurance in the US is around $1,800. But, of course, that number can vary significantly depending on your location and other factors.

How do I find the best deal on EV insurance by state?

To find the best deal on EV insurance by state, you'll want to compare rates and policies from different providers. You can start by checking out online insurance marketplaces, or by contacting local insurers directly. And don't be afraid to negotiate - some insurers may offer discounts or incentives for certain types of EVs or driving habits.

What are the benefits of buying a used EV?

There are plenty of benefits to buying a used EV, from the cost savings to the reduced environmental impact. For one thing, used EVs tend to be cheaper than new models, which can be a major consideration for budget-conscious buyers. And, of course, there's the added benefit of reducing waste and supporting sustainable transportation.

How does EV insurance by state affect the cost of ownership?

EV insurance by state can play a significant role in shaping the overall cost of ownership. If you live in a state with high insurance requirements or expensive premiums, you might find that your costs are higher than if you lived in a state with more relaxed regulations. On the other hand, if you live in a state with low insurance costs, you might be able to save some money on your overall cost of ownership.

What are the most expensive states for EV insurance?

According to our research, some of the most expensive states for EV insurance include California, New York, and Florida. These states tend to have higher insurance requirements and more expensive premiums, which can drive up the cost of ownership for EV buyers.

Can I save money on EV insurance by driving a hybrid or plug-in hybrid?

Yes, you might be able to save some money on EV insurance by driving a hybrid or plug-in hybrid. These vehicles tend to be cheaper to insure than full EVs, simply because of their lower value and repair costs. So, if you're looking to save some money on insurance, a hybrid or plug-in hybrid might be worth considering.

How does the age of my EV affect my insurance costs?

The age of your EV can play a significant role in shaping your insurance costs. Newer EVs tend to be more expensive to insure, simply because of their higher value and repair costs. On the other hand, older EVs might be cheaper to insure, simply because of their lower value and reduced risk.

And that's a wrap, folks. So, does buying used actually save you on premiums? Well, that depends on a variety of factors, from the cost of the vehicle to the insurance requirements in your state. But one thing's for sure: EV insurance by state is a complex and nuanced topic, and it's worth doing your research to find the best deal.

Cheers from the EV insurance trenches.

— Alex,