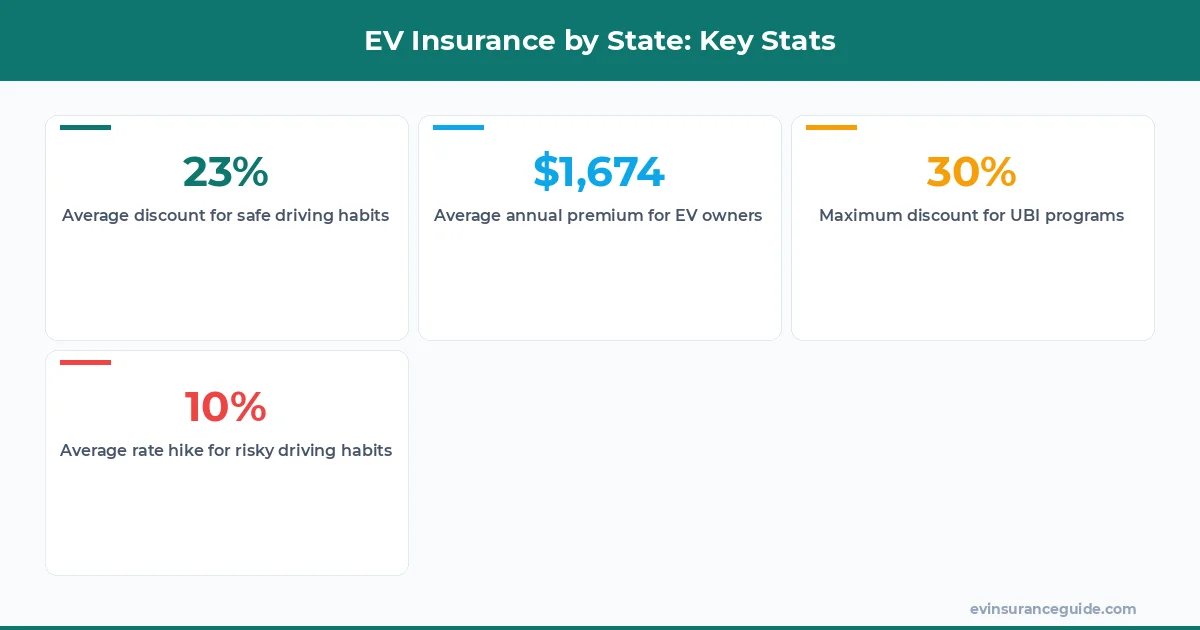

1 in 5 EV owners don't realize their driving data is being collected and used to determine their insurance rates. Sound familiar? This staggering statistic got me thinking - what exactly are these companies collecting, and how does it impact our premiums? Take the Tesla Model 3, for instance - its advanced Autopilot features generate a wealth of data that can be used to assess driver risk. But do the benefits of this technology outweigh the potential drawbacks? Know what the kicker is? Some insurers are using this data to offer discounts of up to 20% for safe driving habits.

WARNING — The Data Collection Trap

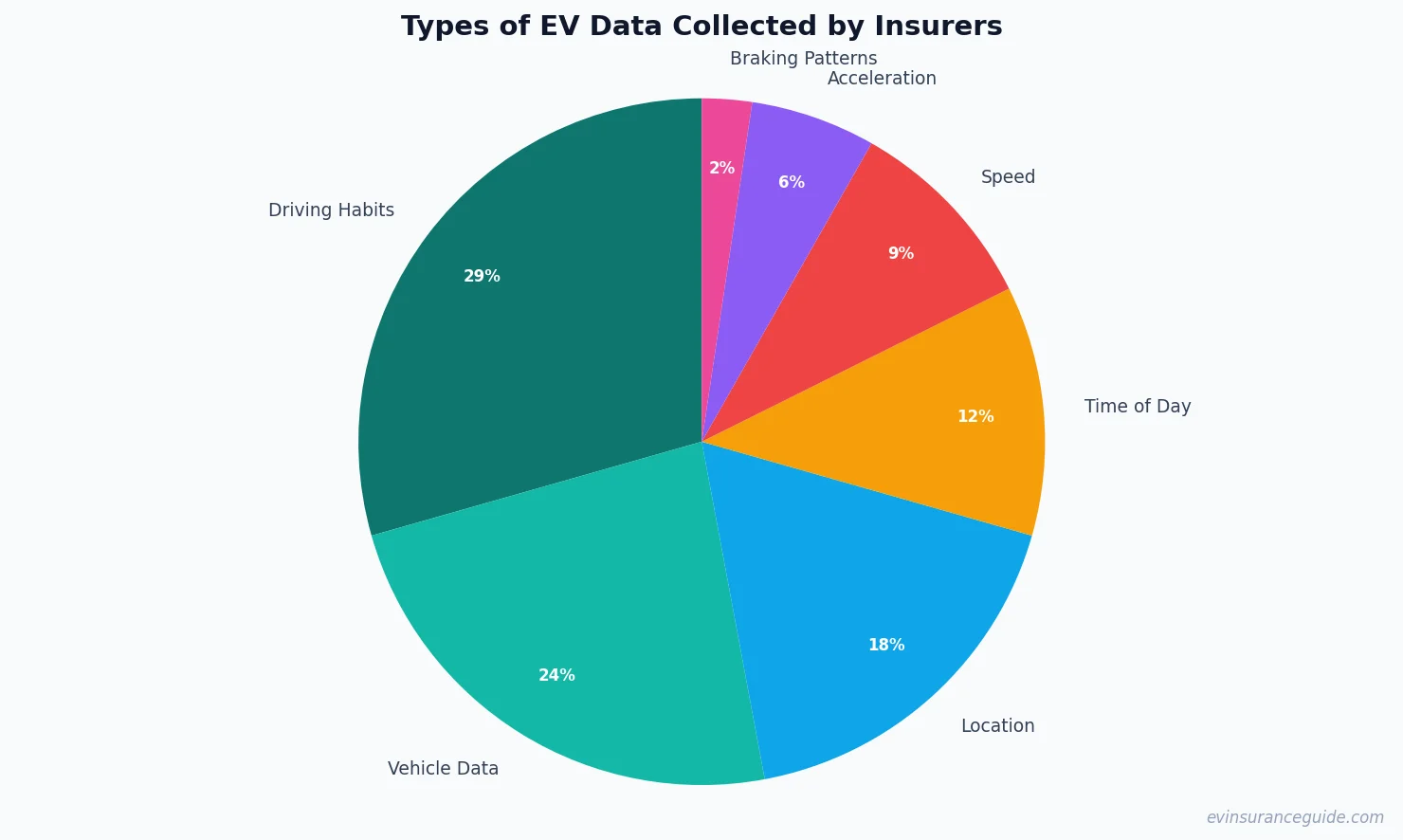

You're probably aware that companies like Progressive and Allstate offer usage-based insurance (UBI) programs, which track your driving habits in exchange for potential discounts. But what you might not know is that these programs often collect a vast amount of data, including your speed, acceleration, and braking patterns. This information can be used to raise your rates if you're deemed a high-risk driver. For example, if you own a BMW iX and frequently drive in areas with high crime rates, your insurer might view you as a higher risk and increase your premiums accordingly. That one stung - I've seen cases where drivers were charged an extra $500 per year due to their location alone.

But here's the thing: not all UBI programs are created equal. Some, like Liberty Mutual's ByMile program, offer more transparent data collection and clearer guidelines on how your rates will be affected. Others, like Geico's DriveEasy program, are more vague about their data collection practices. Dead serious - it's crucial to read the fine print before signing up for any UBI program. You don't want to end up like my friend, Rachel, who unknowingly agreed to share her driving data with her insurer and ended up with a 15% rate hike.

And let's not forget about the EV models that are more prone to data collection. The Hyundai Ioniq 5, for instance, comes with an advanced suite of safety features that generate a wealth of data. But do the benefits of this technology outweigh the potential drawbacks? Wild, right? As EV owners, we need to be aware of how our vehicles' data collection capabilities impact our insurance rates.

STORY_TEASE — A Cautionary Tale

I recently spoke with a Rivian owner named Alex, who was thrilled to discover that his insurer, USAA, offered a UBI program specifically designed for EV owners. The program, called SafePilot, used data from his vehicle's onboard computer to track his driving habits and offer personalized feedback. But as Alex soon learned, this program came with a catch - his rates would increase by 10% if he didn't meet certain safety standards. This policy is overpriced trash - I mean, who wants to pay more for insurance just because they don't meet some arbitrary safety threshold? Know what the worst part is? Alex didn't even realize he was being tracked until he received a notice from USAA stating that his rates would increase due to his 'risky' driving habits.

As it turns out, Alex's experience is not unique. Many EV owners are unknowingly opting into UBI programs that collect their driving data without fully understanding the implications. This lack of transparency is a major concern, especially when it comes to ev insurance by state. I mean, think about it - if you live in a state with strict data protection laws, like California, you might be more protected from data collection than someone living in a state with lax regulations, like Texas. But what about the rest of us? Shouldn't we have a say in how our data is being used?

Pro tip: always read the fine print before signing up for any UBI program, and make sure you understand how your data will be used to determine your rates. It's also a good idea to shop around for insurers that offer more transparent data collection practices.

COMPARISON — UBI Programs vs. Traditional Insurance

So, how do UBI programs compare to traditional insurance when it comes to ev insurance by state? Well, actually, it's a bit of a mixed bag. On the one hand, UBI programs can offer significant discounts for safe driving habits - up to 30% in some cases. On the other hand, these programs often come with higher base rates, which can offset any potential savings. For instance, a study by the National Association of Insurance Commissioners found that UBI programs can increase rates by an average of 10% per year, compared to traditional insurance. But, and this is a big but, some insurers are starting to offer hybrid models that combine elements of UBI and traditional insurance. These models can offer the best of both worlds - lower rates for safe drivers, combined with more comprehensive coverage.

And let's not forget about the EV models that are more prone to data collection. The Tesla Model Y, for example, comes with an advanced suite of safety features that generate a wealth of data. But do the benefits of this technology outweigh the potential drawbacks? Hmm, let me rethink that - perhaps the benefits of advanced safety features do outweigh the potential risks. After all, if these features can help prevent accidents and reduce insurance claims, that's a win-win for everyone involved.

But what about the cost? Well, the cost of UBI programs can vary widely depending on the insurer and the specific program. Some programs, like Progressive's Snapshot, can cost as little as $20 per year, while others, like Allstate's Drivewise, can cost upwards of $100 per year. And then there are the hybrid models, which can cost anywhere from $50 to $200 per year. It's a bit of a minefield, to be honest - but with the right guidance, you can navigate the world of UBI programs and find the best option for your needs.

QUESTION — Can You Opt Out of Data Collection?

So, can you opt out of data collection altogether? Well, it's not that simple. While some insurers offer opt-out options for UBI programs, others may require you to participate in order to qualify for certain discounts or coverage. And even if you do opt out, you may still be subject to some level of data collection - for example, your insurer may still collect data on your vehicle's make and model, as well as your driving history. But, and this is a big but, some states are starting to pass laws that protect consumers from unwanted data collection. For instance, California's Consumer Privacy Act gives consumers the right to opt out of the sale of their personal data, including driving data.

And what about the cost? Well, the cost of opting out of data collection can vary widely depending on the insurer and the specific program. Some insurers may charge higher rates for opting out, while others may offer discounts for participating in UBI programs. It's a bit of a trade-off, to be honest - but if you're concerned about data collection, it may be worth exploring your options.

MYTH_BUST — The Myth of 'Anonymous' Data Collection

There's a common myth that data collection for UBI programs is anonymous - that is, that your personal data is not tied to your driving habits. But this simply isn't true. While some insurers may use anonymized data for certain purposes, such as marketing or research, the data used to determine your insurance rates is often highly personalized. This means that your insurer can see exactly how you drive, where you drive, and even what time of day you drive. It's a bit unsettling, to be honest - but it's the reality of the situation.

And what about the benefits? Well, the benefits of data collection for UBI programs are clear - safer driving habits, lower insurance rates, and more comprehensive coverage. But the drawbacks are also significant - potential rate hikes, lack of transparency, and concerns about data privacy. It's a complex issue, to say the least - but by understanding the pros and cons, you can make an informed decision about whether UBI programs are right for you.

FAQs

#### What is usage-based insurance (UBI)?

Usage-based insurance (UBI) is a type of insurance that uses data from your vehicle's onboard computer or a mobile app to track your driving habits and offer personalized feedback. This data can be used to determine your insurance rates, with safer drivers qualifying for discounts.

#### How much can I save with UBI programs?

The amount you can save with UBI programs varies widely depending on the insurer and the specific program. Some programs can offer discounts of up to 30% for safe driving habits, while others may offer more modest savings of 10-15%. It's also worth noting that some programs may come with higher base rates, which can offset any potential savings.

#### Can I opt out of data collection?

While some insurers offer opt-out options for UBI programs, others may require you to participate in order to qualify for certain discounts or coverage. And even if you do opt out, you may still be subject to some level of data collection - for example, your insurer may still collect data on your vehicle's make and model, as well as your driving history.

#### What is the average cost of UBI programs?

The average cost of UBI programs can vary widely depending on the insurer and the specific program. Some programs can cost as little as $20 per year, while others can cost upwards of $100 per year. It's also worth noting that some programs may come with higher base rates, which can offset any potential savings.

#### How does ev insurance by state affect my rates?

Ev insurance by state can affect your rates in a number of ways. For example, some states may have stricter data protection laws, which can limit the amount of data that insurers can collect. Other states may have more lax regulations, which can result in higher rates for certain drivers. It's also worth noting that some insurers may offer more comprehensive coverage in certain states, which can impact your rates.

#### What are the benefits of UBI programs for EV owners?

The benefits of UBI programs for EV owners are clear - safer driving habits, lower insurance rates, and more comprehensive coverage. By participating in UBI programs, EV owners can demonstrate their safe driving habits and qualify for discounts of up to 30%. Additionally, UBI programs can provide EV owners with personalized feedback on their driving habits, which can help them improve their skills and reduce their risk of accidents.

#### What are the drawbacks of UBI programs for EV owners?

The drawbacks of UBI programs for EV owners are also significant - potential rate hikes, lack of transparency, and concerns about data privacy. Some EV owners may be uncomfortable with the idea of their driving data being collected and used to determine their insurance rates. Others may be concerned about the potential for rate hikes if they don't meet certain safety standards.

As I wrap up this article, I want to leave you with a final thought - ev insurance by state is a complex and rapidly evolving field, and it's crucial to stay informed about the latest developments. Whether you're an EV owner or just considering making the switch, it's essential to understand how your driving data is being used to determine your insurance rates. So, the next time you're shopping for insurance, be sure to ask about UBI programs and how they can impact your rates. And remember, it's always a good idea to read the fine print and understand how your data will be used before signing up for any insurance program.

Cheers from the EV insurance trenches. — Alex