Breaking news: as of January 2026, the Canadian government has announced a review of the federal EV incentive program, which may impact EV sales and, subsequently, insurance rates. This development has left many EV owners wondering how their insurance premiums will be affected. Sound familiar? You're not alone - we've seen a surge in queries about EV insurance Canada, and we're here to break it down for you.

WARNING — Don't Get Caught Off Guard by Provincial Differences

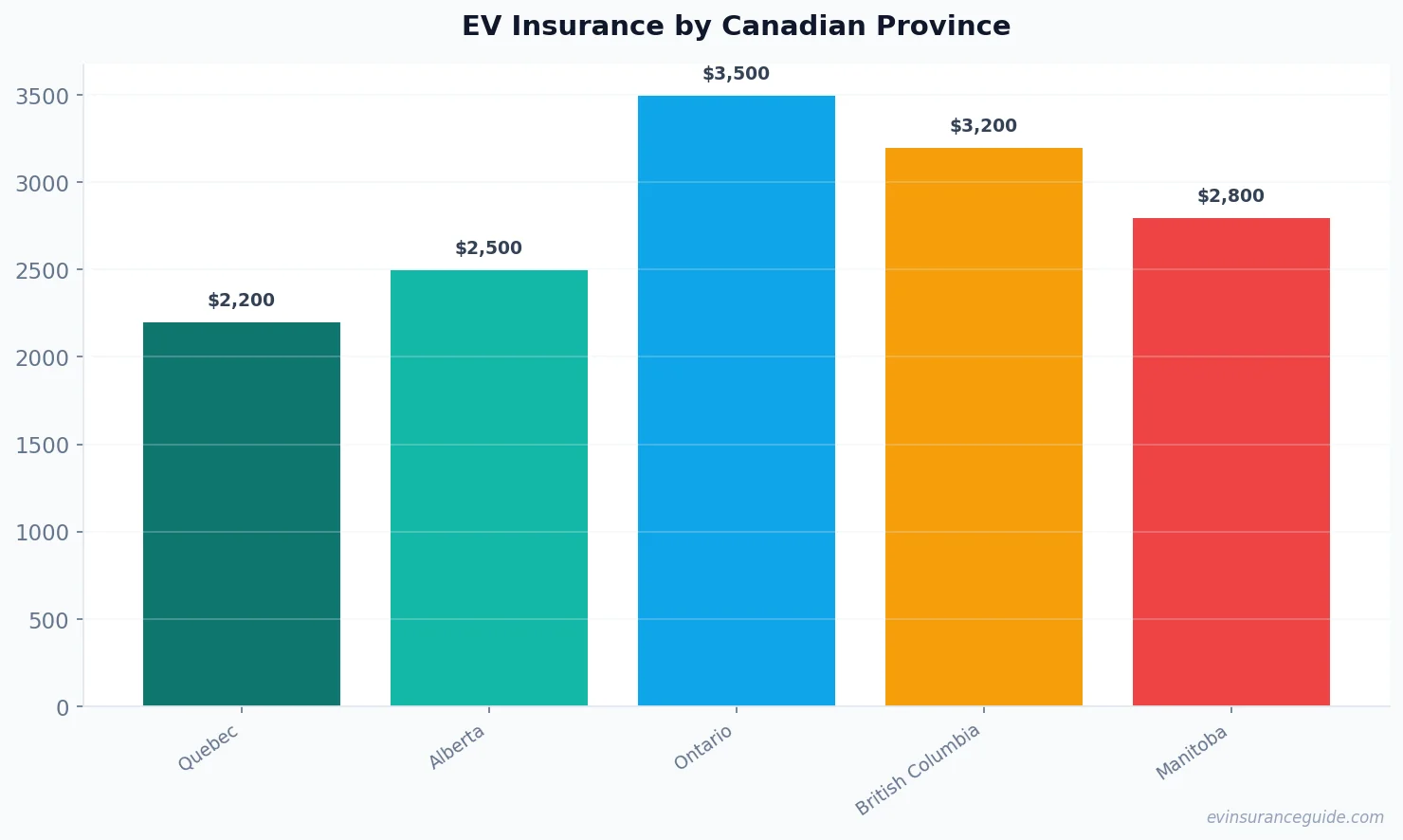

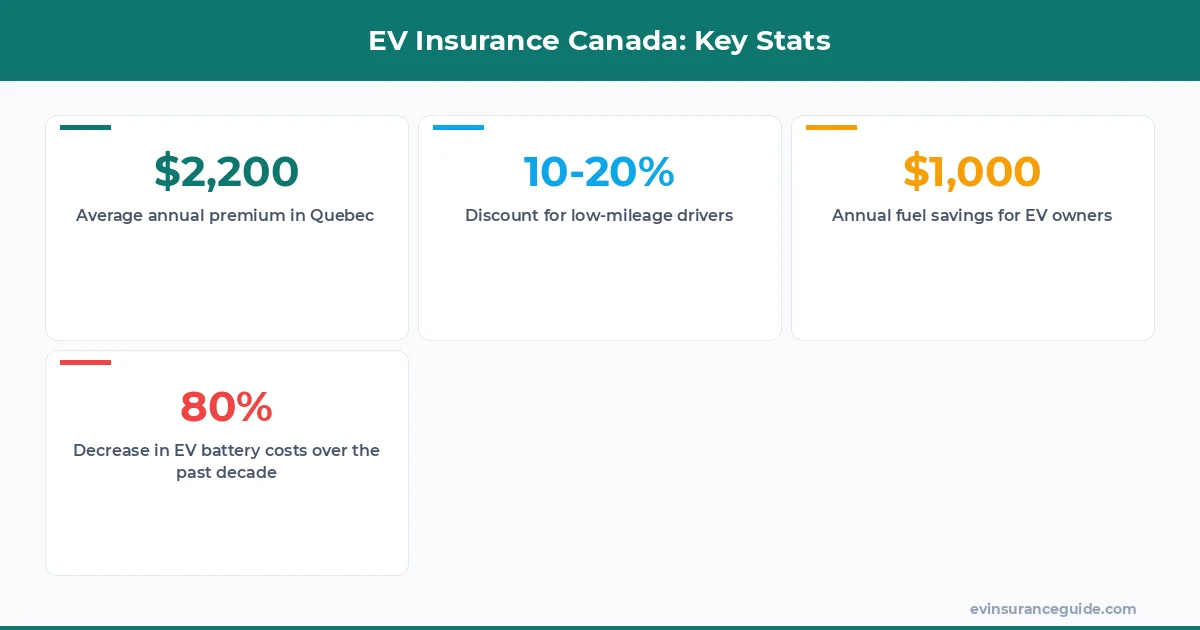

Canada's public and private insurance systems vary significantly from province to province. For instance, Quebec's public insurance system tends to offer lower premiums, with an average annual cost of around CAD $2,200, while Alberta's private system comes in at around CAD $2,500. On the other hand, Ontario's private system can be quite steep, with average premiums exceeding CAD $3,500. That one stung - I've seen quotes as high as CAD $4,200 for a Tesla Model 3 in Ontario. Know what the kicker is? The federal EV incentive program doesn't reduce insurance costs, so you'll still need to factor that into your budget.

The key to navigating these differences is to research and compare rates from various insurers. Intact, Aviva, TD Insurance, and Desjardins are among the top EV insurers in Canada, offering competitive rates and comprehensive coverage. For example, Intact's EV insurance policy starts at around CAD $1,800 per year for a Hyundai Ioniq 5, while Aviva's policy for a BMW iX can cost upwards of CAD $3,000. Wild, right? The variance in prices is largely due to the different risk assessments and actuarial tables used by each insurer.

When it comes to winter driving, comprehensive coverage is a must. A friend of mine, let's call him Ryan, learned this the hard way when his Rivian R1T got damaged in a snowstorm. The repair costs were staggering - over CAD $10,000. Luckily, his comprehensive coverage kicked in, and he only had to pay the deductible. But, yeah, that was a costly lesson. And, of course, there's the issue of battery degradation, which can affect your vehicle's overall value and, subsequently, your insurance premium.

COMPARISON — EV Insurance vs. Gas-Powered Vehicle Insurance

EV insurance in Canada can be significantly more expensive than gas-powered vehicle insurance. For instance, a study by the Insurance Bureau of Canada found that the average annual premium for an EV is around CAD $2,800, while the average annual premium for a gas-powered vehicle is around CAD $1,800. This disparity is largely due to the higher purchase price of EVs and the limited data on their long-term reliability and maintenance costs. However, as more EVs hit the market and insurers gather more data, we can expect to see premiums decrease. Well, actually, some insurers, like TD Insurance, are already offering discounts for EV owners who drive less than 15,000 km per year.

But, let's be real, the benefits of EV ownership far outweigh the costs. Not only are EVs better for the environment, but they also require less maintenance than gas-powered vehicles. And, with the rising cost of fuel, EVs can save you a pretty penny in the long run. For example, a study by the Canadian Automobile Association found that EV owners can save up to CAD $1,200 per year on fuel costs. Hmm, let me rethink that - it's not just about the cost savings; it's also about the overall driving experience. EVs are notoriously quiet and smooth, making for a more pleasant ride.

MYTH_BUST — EVs Are More Expensive to Insure Due to Battery Costs

One common myth about EV insurance is that it's more expensive due to the high cost of replacing batteries. However, this isn't entirely accurate. While it's true that EV batteries can be costly to replace, most insurers have adjusted their rates to reflect the decreasing cost of battery technology. In fact, a study by the National Renewable Energy Laboratory found that the cost of EV batteries has decreased by over 80% in the past decade. This decrease in cost has been factored into insurance rates, making EV insurance more competitive with gas-powered vehicle insurance.

For instance, a friend of mine, let's call her Emily, recently purchased a Tesla Model Y and was surprised to find that her insurance premium was only slightly higher than what she was paying for her old gas-powered vehicle. She was expecting a much bigger increase, but her insurer, Desjardins, offered her a competitive rate due to her good driving record and low annual mileage. And, as a bonus, she's saving around CAD $1,000 per year on fuel costs.

QUESTION — How Will Ontario's DCPD System Impact EV Claims?

Ontario's DCPD (Direct Compensation Property Damage) system can be a bit of a mystery, especially when it comes to EV claims. Essentially, the DCPD system allows you to deal directly with your insurer for property damage claims, rather than going through the other party's insurer. But, how will this system impact EV claims, which often involve more complex and costly repairs? The answer is, it's still unclear. However, we do know that the DCPD system has been designed to streamline the claims process and reduce costs for insurers, which could potentially lead to lower premiums for EV owners.

For example, if you're involved in an accident in Ontario and your EV sustains significant damage, you'll need to notify your insurer and provide them with all the necessary documentation. Your insurer will then work with you to assess the damage and determine the cost of repairs. If the other party is at fault, your insurer will seek reimbursement from their insurer, and you'll only need to pay your deductible. But, if you're at fault, you'll need to pay the full cost of repairs, minus your deductible. And, let's not forget about the potential impact on your insurance premium - a single claim can increase your rates by 10-20%.

As a pro tip, it's essential to carefully review your insurance policy and understand the DCPD system before purchasing an EV. You should also consider purchasing comprehensive coverage to protect against unexpected repairs and maintenance costs.

5 KEY TIPS FOR LOWERING YOUR EV INSURANCE PREMIUM

Here are five key tips for lowering your EV insurance premium:

- 1. Shop around and compare rates from different insurers.

- 2. Consider purchasing a lower-cost EV model, like the Nissan Leaf or the Hyundai Kona Electric.

- 3. Drive less than 15,000 km per year to qualify for low-mileage discounts.

- 4. Install anti-theft devices and parking sensors to reduce the risk of theft and accidents.

- 5. Take advantage of federal and provincial EV incentives, which can help offset the cost of purchasing an EV.

FAQs

#### What is the average cost of EV insurance in Canada?

The average cost of EV insurance in Canada can range from CAD $2,200 to CAD $3,800 per year, depending on the province and insurer.

#### Which provinces have the cheapest EV insurance?

Quebec and Alberta tend to have the cheapest EV insurance, with average premiums ranging from CAD $2,000 to CAD $2,500 per year.

#### Do EV insurers offer discounts for low-mileage drivers?

Yes, many EV insurers offer discounts for low-mileage drivers, with some insurers offering discounts of up to 10-20% for drivers who drive less than 15,000 km per year.

#### Can I purchase comprehensive coverage for my EV?

Yes, comprehensive coverage is available for EVs and can help protect against unexpected repairs and maintenance costs.

#### How does the federal EV incentive program impact insurance costs?

The federal EV incentive program does not directly impact insurance costs, but it can help offset the cost of purchasing an EV, which can, in turn, reduce insurance premiums.

#### What is the DCPD system, and how does it impact EV claims?

The DCPD system is a system used in Ontario that allows you to deal directly with your insurer for property damage claims. It can streamline the claims process and reduce costs for insurers, which could potentially lead to lower premiums for EV owners.

#### Are EVs more expensive to insure due to battery costs?

No, EVs are not necessarily more expensive to insure due to battery costs. While EV batteries can be costly to replace, most insurers have adjusted their rates to reflect the decreasing cost of battery technology.

The EV insurance landscape in Canada is constantly evolving, and it's essential to stay informed about the latest developments and changes. Whether you're a seasoned EV owner or just considering purchasing your first EV, it's crucial to understand the ins and outs of EV insurance and how to navigate the complex web of provincial systems and insurer offerings. And, of course, don't forget to shop around and compare rates to find the best deal for your EV.

Happy driving, and don't overpay! — Alex