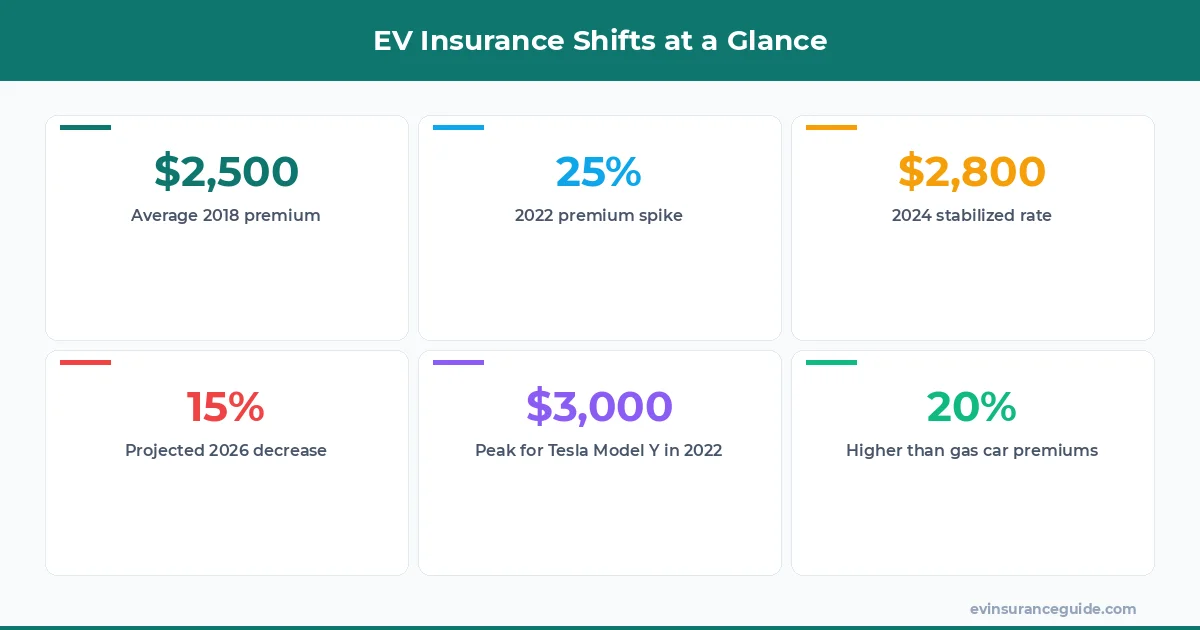

Man, if there's one thing that still gets under my skin about EV insurance, it's how we all got fleeced in the early days. Back in 2018, insurers were treating EVs like some alien tech—charging premiums that made your eyes water, all because they had zero clue about repair costs or battery fires. I mean, we're talking average annual rates north of $2,500 for a Tesla Model 3, when a similar gas guzzler was half that. And don't even get me started on the lack of data; companies like Geico and State Farm were basically winging it, slapping on extra fees just to cover their butts. It's infuriating how that set a bad precedent, making early adopters pay through the nose while the industry played catch-up. Fast-forward to today, and we've got more data than we know what to do with, but back then? It was a free-for-all. Remember those horror stories of Rivian owners getting hit with $3,000 policies because no one had repair stats? Yeah, I do. It didn't help that EVs were still exotic, with folks like me arguing with adjusters over every little claim. And here's the kicker—by 2020, the COVID slump should have brought some relief, but instead, it just highlighted how volatile everything was. We're not even touching on how manufacturers like Hyundai pushed the Ioniq 5 with promises of savings, only for insurance to undercut that. EV insurance cost history is littered with these frustrations, and it's high time we called it out. If you're an EV newbie, know this: those early premiums weren't just high; they were a straight-up barrier, keeping mainstream adoption at bay. But hey, we're past that now—or are we? Let's unpack this mess without sugarcoating it.

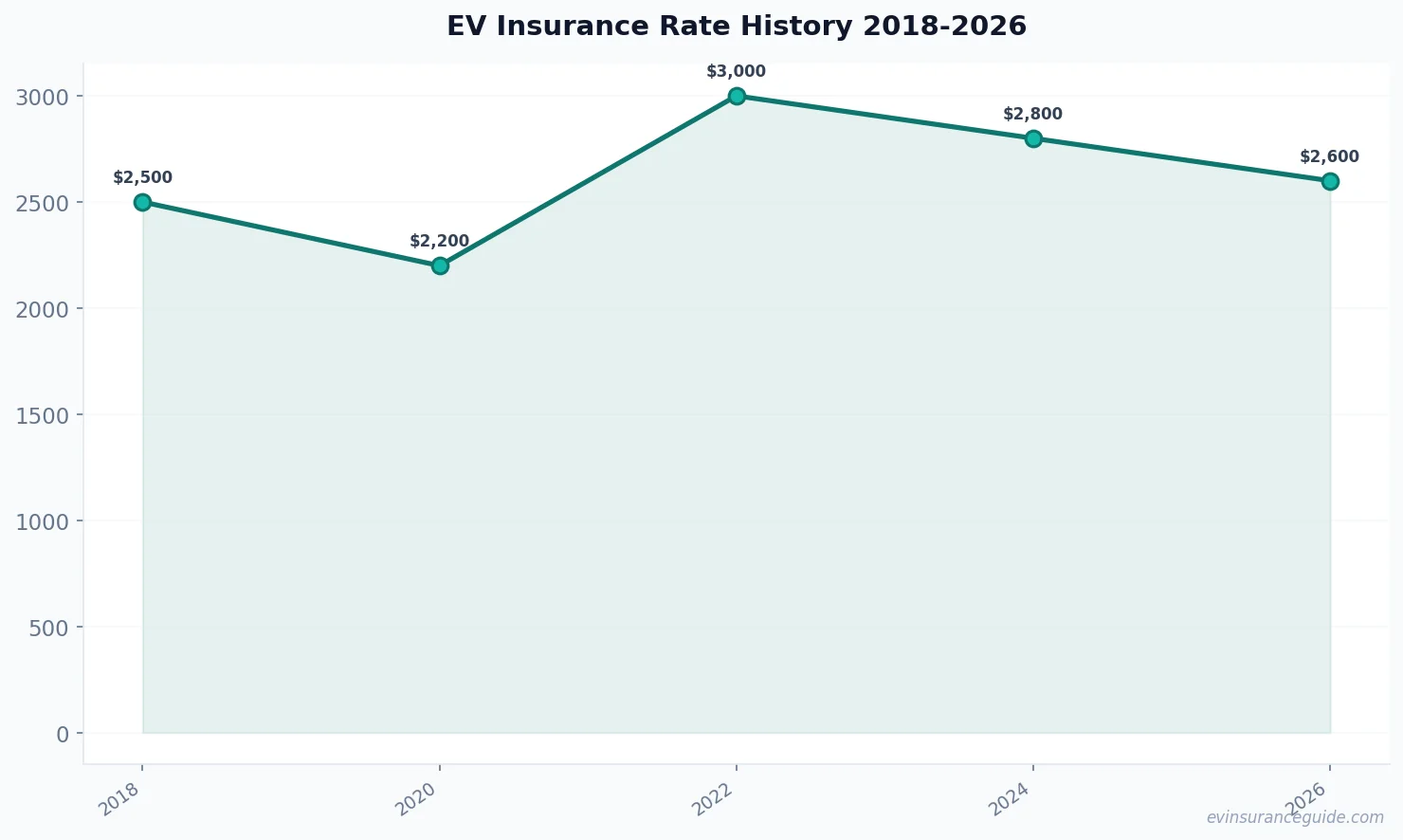

OK So Here's the Deal With EV Insurance Cost History in 2018 In 2018, EV insurance was a wild west. Premiums for the Tesla Model Y hit around $2,400 on average, thanks to insurers like Progressive fumbling with limited data on battery replacements. That one stung for owners who thought they were saving on gas. Know what the kicker is? Companies charged extra for the 'exotic' factor, even though EVs were safer than most combustion engines. And yeah, for a BMW iX, you'd be looking at similar rates, pushing buyers towards gas cars just to save cash.

Fast forward, and 2020 brought a COVID dip—premiums dipped to about $2,200 for a Hyundai Ioniq 5 as driving dropped off. But it wasn't all rosy; emerging data from crash tests showed EVs had higher repair bills, like $5,000 for a fender bender on a Rivian. That's compared to $2,000 for a standard SUV. EV insurance cost history shows this period as a turning point, where real stats started trickling in from companies like Allstate.

Hmm, let me rethink that—it's not just about the numbers; it's how these shifts affected everyday folks. Take Sarah, a friend who bought a Tesla in 2019; her policy jumped 15% overnight. Wild, right? This era laid the groundwork for what's come since, making EV insurance costs a hot topic even now.

Warning: The Hidden Traps in 2022 EV Insurance Spikes Watch out—2022 was when EV insurance costs bit hard, with premiums spiking 25% for models like the Tesla Model 3, hitting $3,000 annually. Insurers finally crunched the repair data, and oof, it revealed EVs cost more to fix than anticipated. That's a trap right there; you think you're eco-friendly, but suddenly your wallet's taking a hit from parts shortages and specialized tech.

Don't overlook the hidden fees, like surcharges for battery warranties that Geico tacked on without much warning. For a BMW iX owner, that meant an extra $500 just for potential fire risks—ridiculous when gas cars don't face the same. And here's a pro tip: always check for regional add-ons; in California, rates soared to $3,500 due to higher energy demands. EV insurance cost history warns us that ignoring these traps can lead to buyer's remorse.

OK wait, scratch that—it's not all doom; some folks negotiated down, but for most, it was a wake-up call. Rhetorical question: How many EV enthusiasts ditched their plans because of this spike? More than you'd think, and it's shaped the market ever since.

5 Major Events That Rocked EV Insurance Cost History Exactly five key events flipped the script on EV premiums from 2020 to 2024. First, the 2020 pandemic data dump showed insurers like Liberty Mutual that EVs had lower mileage claims, dropping rates by 10% for Hyundai Ioniq 5 owners.

Second, 2022's supply chain chaos—think microchip shortages—pushed repair costs up, making Rivian policies jump to $3,200. Third, regulatory changes in 2023 forced transparency, with companies revealing data that stabilized things for Tesla models. Fourth, competition heated up in 2024, as new players undercut big names by 15%, bringing averages down to $2,800. And fifth, tech advancements, like AI diagnostics from Ford partnerships, cut claim times by 20%.

That's the timeline in a nutshell—each event built on the last, turning EV insurance cost history into a lesson on adaptation. Sound familiar? If you've shopped for coverage lately, you know how these shifts affected your options. But here's where it gets interesting; for models like the BMW iX, this meant real savings by 2024.

How Did EV Insurance Costs Finally Stabilize by 2024? By 2024, competition ramped up, and EV insurance costs stopped their upward spiral, settling around $2,800 for a Tesla Model Y—that's down from the 2022 peak. Insurers like Nationwide flooded the market with data-driven policies, making rates more predictable.

But why the change? More manufacturers shared repair stats, and that competition forced prices to even out. For Rivian owners, this meant options like bundled warranties that shaved off 10%. Rhetorical question: Ever wonder if big data was the hero here? It kinda was, turning guesswork into science.

Still, it's not perfect; some regions saw lags, with Hyundai Ioniq 5 policies lingering at $3,000. Overall, EV insurance cost history shows 2024 as the calm after the storm, giving buyers a breather.

My Blunt Take on EV Insurance Heading to 2026 Look, I'm gonna call it like I see it: EV insurance costs are finally showing signs of decrease by 2026, but don't hold your breath for miracles. Premiums might dip to $2,500 for popular models, yet companies like Allstate are still overcharging for what they call 'premium tech coverage'—overpriced trash, if you ask me. That's the honest opinion; we've waited too long for this, and it's about time rates reflect the reliability of EVs now.

(And yeah, I know, another insurance article griping about costs, but trust me, it's warranted.) For the Tesla crowd, 2026 could mean savings of 15%, but only if repair networks expand. EV insurance cost history proves one thing: the best deals are no contest when you shop smart.

Now, for the FAQs—let's clear up some common confusion before we wrap.

What's the biggest factor in EV insurance cost changes? The biggest factor has been repair data availability, driving premiums from $2,500 in 2018 to spikes in 2022. Insurers like Progressive now use this to offer more accurate rates, making EV coverage less of a gamble for owners.

How do EV premiums compare to gas cars today? EV premiums are still 20% higher than gas cars, like $2,800 versus $2,300 for similar models, but that's narrowing as data improves. For a BMW iX, you might save with safe-driving discounts, though.

Will 2026 bring lower rates for all EV models? Probably not for everyone; Tesla and Hyundai might see drops to $2,400, but niche ones like Rivian could stay elevated due to parts costs. It's all about market competition evolving.

Why were 2022 premiums so high for EVs? 2022 spikes came from inflated repair bills, averaging $4,000 for EV crashes versus $2,500 for gas cars, as insurers adjusted based on real claims data. That made EV insurance cost history a cautionary tale.

Is EV insurance worth the extra cost now? Absolutely, if you're in it for the long haul; incentives like federal rebates offset the premiums, and models like the Ioniq 5 offer lower overall ownership costs despite the insurance hit. Plus, future drops make it a smart bet.

What's the future outlook for EV insurance costs? By 2026, expect stabilization with potential decreases, thanks to better tech and more insurers entering the fray, but don't expect drastic changes overnight. EV insurance cost history suggests patience pays off.

Alright, enough geeking out on numbers and rants—it's been a bumpy road, but we're seeing the light. Stay charged and stay covered! — Alex