Breaking news: as of January 2026, several major insurers have updated their EV policy requirements for business use. If you're using your personal EV for work, you'll want to know how these changes affect you. Sound familiar? You're not alone - thousands of self-employed EV owners are navigating this complex landscape.

HONEST_OPINION

Let's get real - EV insurance for business use can be a total minefield. You've got personal policies, commercial policies, and mixed-use coverage options to consider. And don't even get me started on the varying requirements from insurer to insurer. That one stung - I've seen self-employed EV owners get caught out with hefty premiums or even policy cancellations due to incorrect classification.

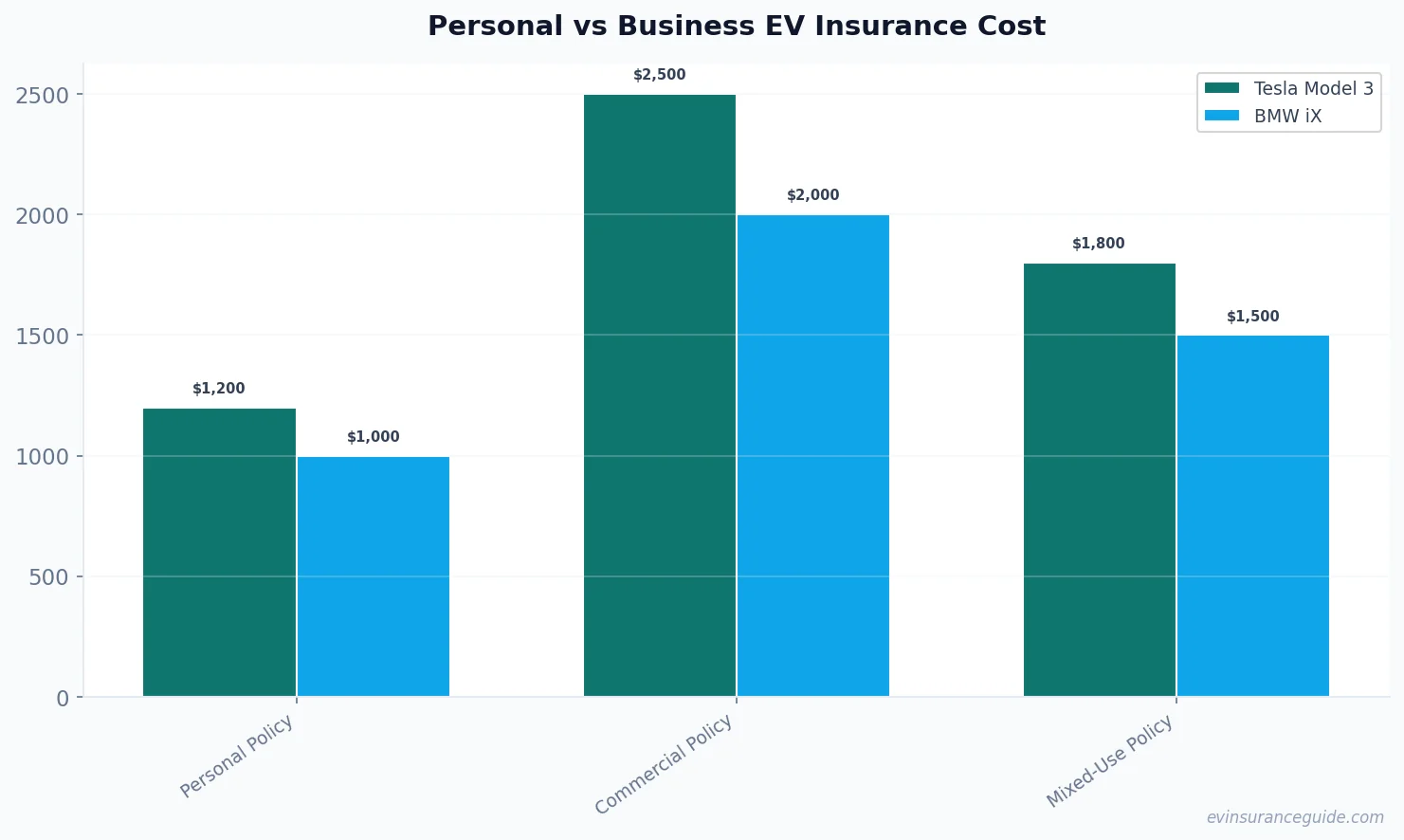

For example, if you're using your Tesla Model 3 for both personal and business use, you might need a commercial policy if you're driving more than 50% of the time for work. But what if you're using your BMW iX for a mix of personal and business trips? The rules get murky fast. Know what the kicker is? Some insurers won't even offer mixed-use coverage, leaving you to choose between a personal or commercial policy.

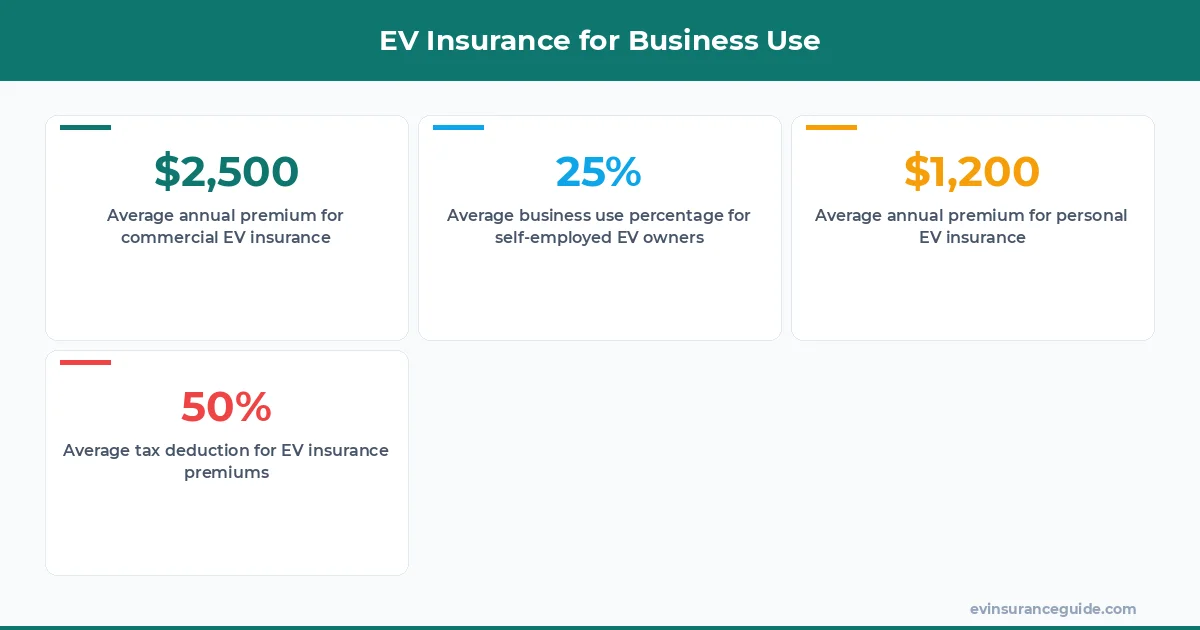

Dead serious - this can have major implications for your business's bottom line. A commercial policy for your Hyundai Ioniq 5 could cost upwards of $2,500 per year, while a personal policy might be closer to $1,200. That's a $1,300 difference - not exactly chump change. And what about the tax implications? Can you deduct your EV insurance premiums as a business expense?

STORY_TEASE

I've got a friend, let's call her Rachel, who's a freelance consultant. She uses her Rivian for both personal and business trips, and she's been struggling to find an insurer that offers mixed-use coverage. Her current insurer is threatening to cancel her policy if she doesn't switch to a commercial policy, which would more than double her premiums. Wild, right? I've been helping her navigate the options, and we're exploring everything from usage-based insurance to pay-per-mile policies.

One thing we're looking at is the cost of commercial policies versus personal policies. For Rachel's Rivian, a commercial policy would cost around $3,000 per year, while a personal policy would be closer to $1,500. But what if she could get a mixed-use policy that covers both personal and business use? That could be a game-changer. And what about the cost of insurance for other EV models, like the Tesla Model Y or the Audi e-tron?

We've been researching different insurers, including Geico, Progressive, and State Farm. Each has its own set of rules and requirements for EV insurance, and it's been a challenge to find one that fits Rachel's needs. But we're getting close - I think we've found an insurer that offers a mixed-use policy that could work for her.

COMPARISON

OK, let's compare apples to oranges - or in this case, personal EV insurance to commercial EV insurance. If you're using your EV solely for personal use, you can expect to pay around $1,000 to $1,500 per year for insurance, depending on the model and your location. But if you're using your EV for business use, even part-time, you'll need to consider a commercial policy. This can cost anywhere from $2,000 to $5,000 per year, depending on the insurer and your specific circumstances.

For example, if you're using your Tesla Model 3 for business use, you might need to pay around $2,500 per year for insurance. But if you're using your BMW iX for personal use only, you might pay closer to $1,200 per year. That's a big difference - and it's not just the cost of the policy itself, but also the tax implications. Can you deduct your EV insurance premiums as a business expense?

The answer is yes - but only if you're using your EV for business use. If you're self-employed, you can deduct the business use percentage of your EV insurance premiums on your tax return. For example, if you're using your Hyundai Ioniq 5 for 80% business use and 20% personal use, you can deduct 80% of your insurance premiums as a business expense. That could be a significant tax savings - around $1,000 to $1,500 per year, depending on your premium costs.

7 Things to Know

About EV insurance for business use - and how to navigate the complex world of personal and commercial policies. First, know that some insurers offer usage-based insurance or pay-per-mile policies, which can be a great option for self-employed EV owners. Second, be aware that the cost of commercial policies can vary widely depending on the insurer and your specific circumstances.

Third, don't assume that a personal policy will cover you for business use - it's unlikely, and you could be left with a hefty bill if you're involved in an accident while driving for work. Fourth, shop around - different insurers offer different rates and coverage options, so it's worth comparing policies to find the best fit for your needs.

Fifth, consider the tax implications - can you deduct your EV insurance premiums as a business expense? Sixth, be aware of the requirements for commercial policies - some insurers may require you to have a certain level of business use or to meet specific criteria. Seventh, don't be afraid to ask questions - your insurer should be able to guide you through the process and help you find the right policy for your needs.

CASUAL_DIRECT

OK So Here's the Deal With EV Insurance for Business Use - it's complicated, but it's not impossible to navigate. You just need to know what you're looking for - and be willing to shop around to find the best policy for your needs. For example, if you're using your Rivian for business use, you might want to consider a commercial policy from an insurer like Geico or Progressive.

But if you're using your Tesla Model 3 for personal use only, you might be able to get away with a personal policy from an insurer like State Farm. And what about the cost of insurance for other EV models, like the Audi e-tron or the Hyundai Kona Electric? We've got the details - and we're breaking it down for you.

For instance, the cost of insurance for a Tesla Model Y can range from $1,500 to $2,500 per year, depending on the insurer and your location. But the cost of insurance for a BMW iX can range from $1,200 to $2,000 per year. That's a big difference - and it's not just the cost of the policy itself, but also the tax implications.

FAQs

#### What is the difference between personal and commercial EV insurance?

The main difference between personal and commercial EV insurance is the level of coverage and the cost of the policy. Personal policies typically cover personal use only, while commercial policies cover business use. The cost of commercial policies can be significantly higher than personal policies - around $2,000 to $5,000 per year, depending on the insurer and your specific circumstances.

#### Can I deduct my EV insurance premiums as a business expense?

Yes, you can deduct your EV insurance premiums as a business expense if you're using your EV for business use. You'll need to keep records of your business use percentage and your insurance premiums, and you can deduct the business use percentage of your premiums on your tax return.

#### What is the cost of EV insurance for business use?

The cost of EV insurance for business use can vary widely depending on the insurer, your location, and your specific circumstances. For example, a commercial policy for a Tesla Model 3 could cost around $2,500 per year, while a personal policy for the same vehicle could cost around $1,200 per year.

#### What are the requirements for commercial EV insurance policies?

The requirements for commercial EV insurance policies vary depending on the insurer, but typically include a certain level of business use or specific criteria. You may need to provide documentation of your business use, such as a business license or tax returns.

#### Can I get a mixed-use policy for my EV?

Yes, some insurers offer mixed-use policies that cover both personal and business use. These policies can be a great option for self-employed EV owners who use their vehicles for both personal and business trips.

#### How do I choose the best EV insurance policy for my business use?

To choose the best EV insurance policy for your business use, you'll need to shop around and compare policies from different insurers. Consider the cost of the policy, the level of coverage, and the requirements for commercial policies. You may also want to consider usage-based insurance or pay-per-mile policies, which can be a great option for self-employed EV owners.

#### What are the tax implications of EV insurance for business use?

The tax implications of EV insurance for business use depend on your specific circumstances, but you can typically deduct your EV insurance premiums as a business expense if you're using your EV for business use. You'll need to keep records of your business use percentage and your insurance premiums, and you can deduct the business use percentage of your premiums on your tax return.

Pro tip: Keep accurate records of your business use percentage and your insurance premiums to maximize your tax deductions.

##

And that's a wrap - almost. Just remember, EV insurance for business use is a complex landscape, but it's not impossible to navigate. You just need to know what you're looking for - and be willing to shop around to find the best policy for your needs. Sound familiar? You're not alone - thousands of self-employed EV owners are out there, navigating the same challenges and opportunities.

Cheers from the EV insurance trenches.

— Alex