Are you prepared for the shock of seeing your EV insurance rates skyrocket after a divorce? Sound familiar? I've seen it happen to friends, and it's a harsh reality check. You're already dealing with the emotional fallout, and then you get hit with a premium increase. That one stung.

A Story of Divorce and EV Insurance

Take the case of my friend, Rachel, who owned a Tesla Model 3 with her ex-husband. They had a joint policy with GEICO, which cost them around $1,800 per year. After the divorce, Rachel decided to keep the car, but her rates went up to $2,500 per year. She was shocked and didn't understand why her rates had increased so much. Know what the kicker is? She was still driving the same car, with the same safety features, but her marital status had changed. Wild, right?

When Rachel called GEICO to inquire about the rate increase, they explained that she had lost the multi-car discount, which had been applied to their joint policy. This discount had saved them around $300 per year. Now, as a single policyholder, Rachel didn't qualify for this discount anymore. Okay, wait, scratch that — it's not just about the multi-car discount. There are other factors at play here.

For instance, some insurance companies, like State Farm, offer a discount for married couples. This discount can range from 5% to 10% of the total premium. When you get divorced, you lose this discount, which can lead to a significant increase in your rates. But here's the thing: not all insurance companies offer this discount, and the amount of the discount can vary greatly. You gotta do your research, folks.

Busting the Myth of Standardized EV Insurance Rates

One common myth about EV insurance is that all companies charge the same rates. Nope. That's just not true. I've seen quotes from different companies for the same car, and the prices can vary by hundreds of dollars. For example, a friend of mine, who owns a BMW iX, got a quote from Allstate for $2,200 per year. But when he checked with USAA, he got a quote for $1,800 per year. That's a difference of $400 per year. Dead serious, folks — you need to shop around.

When it comes to EV insurance for divorced drivers, it's essential to understand that rates can vary significantly depending on the company and the specific circumstances. For instance, if you're the one keeping the EV, you might see an increase in your rates due to the loss of the multi-car discount. But if you're the one who's not keeping the EV, you might see a decrease in your rates, since you're no longer responsible for insuring the car. Know what I mean? It's all about the specifics.

Pro tip: When shopping for EV insurance after a divorce, make sure to ask about any discounts you might be eligible for, such as a low-mileage discount or a discount for being a good student. These discounts can add up and help you save on your premiums.

Honest Opinion: EV Insurance for Divorced Drivers is a Mess

I'm gonna be blunt here — EV insurance for divorced drivers is a complex and often confusing topic. There are so many factors at play, and it's hard to predict how your rates will change after a divorce. But here's the thing: you can't just sit back and accept whatever rates you're given. You need to be proactive and shop around for the best deals. Don't be afraid to negotiate with your insurance company, either. If you're not happy with your rates, it's time to switch to a different company.

For example, my friend, Mike, who owns a Hyundai Ioniq 5, was paying $2,000 per year with Progressive. After his divorce, his rates went up to $2,500 per year. But when he switched to Liberty Mutual, he got a quote for $2,000 per year. That's a savings of $500 per year. Not bad, right? And the best part is, he didn't have to sacrifice any coverage or features to get that lower rate.

But what about rebuilding insurance history after a divorce? That's a great question. If you're the one who's not keeping the EV, you might be worried about losing your insurance history. Don't be. Most insurance companies will allow you to transfer your insurance history to a new policy, even if you're not keeping the same car. Just make sure to ask about this when you're shopping for a new policy.

Comparing EV Insurance Rates for Divorced Drivers

Let's compare the EV insurance rates for divorced drivers across different companies. I've seen quotes from companies like GEICO, State Farm, and Allstate, and the prices can vary significantly. For instance, a friend of mine, who owns a Rivian, got a quote from GEICO for $2,800 per year. But when he checked with State Farm, he got a quote for $2,200 per year. That's a difference of $600 per year. Wow, right?

But here's the thing: these rates are not just based on the car itself. They're also based on your driving history, your credit score, and other factors. So, even if you're driving the same car, your rates can vary depending on these other factors. For example, if you have a poor driving history, you might see higher rates, regardless of the company you choose.

Warning: Hidden Costs of EV Insurance for Divorced Drivers

There are some hidden costs to watch out for when it comes to EV insurance for divorced drivers. For instance, some companies might charge a fee for cancelling or changing a policy. This fee can range from $50 to $200, depending on the company. And if you're not careful, you might end up paying more in the long run.

Another thing to watch out for is the potential for rate increases after a divorce. As I mentioned earlier, some companies offer discounts for married couples, which can lead to higher rates after a divorce. But there are other factors at play here, too. For example, if you're the one keeping the EV, you might see an increase in your rates due to the loss of the multi-car discount. But if you're the one who's not keeping the EV, you might see a decrease in your rates, since you're no longer responsible for insuring the car.

FAQs

#### What happens to my EV insurance policy after a divorce?

After a divorce, you'll need to separate your EV insurance policy from your ex-spouse's. This can be a complex process, so it's essential to work with your insurance company to make sure everything is done correctly. You might need to provide documentation, such as a divorce decree, to prove that you're no longer married.

#### How much will my EV insurance rates increase after a divorce?

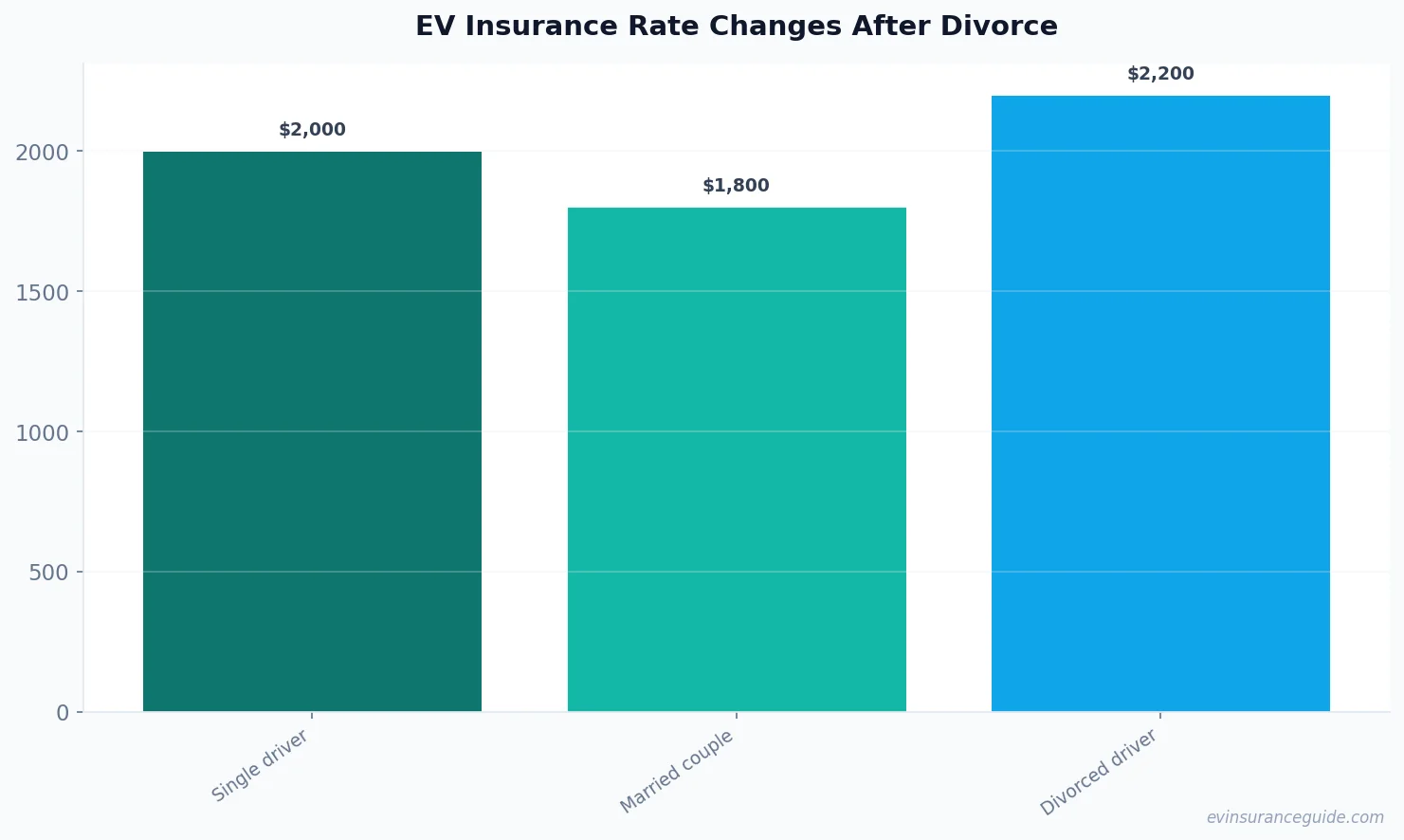

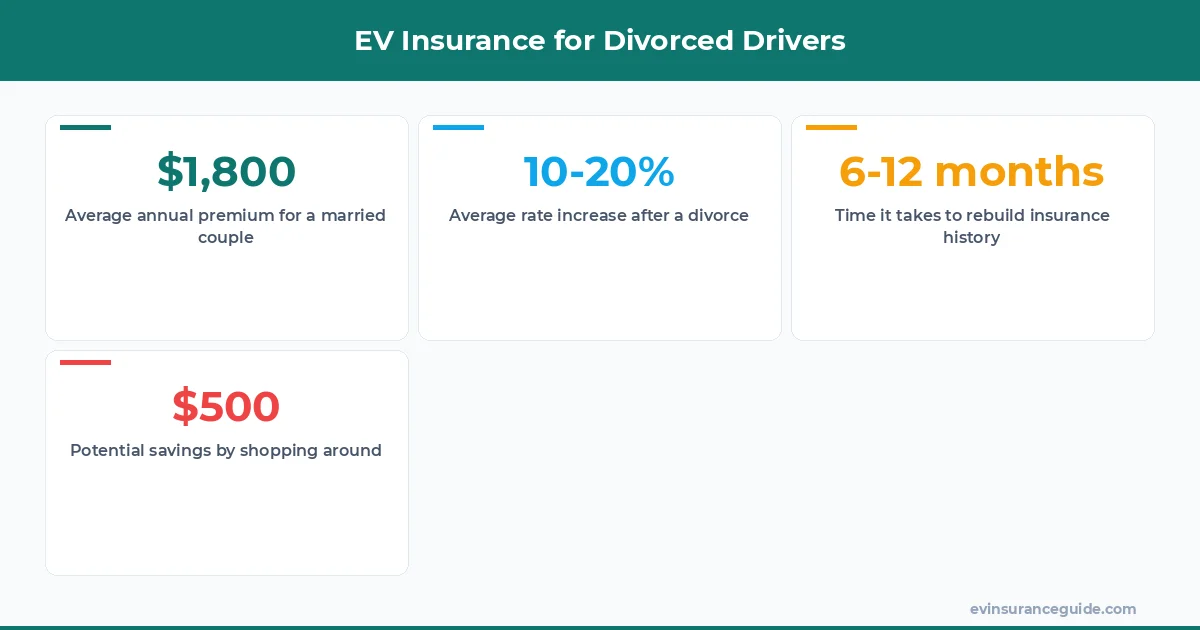

The amount of the rate increase will depend on various factors, including the company you're with, the type of car you drive, and your driving history. On average, you can expect to see an increase of around 10% to 20% after a divorce. But this can vary greatly, so it's essential to shop around and compare quotes from different companies.

#### Can I keep my EV insurance policy after a divorce?

Yes, you can keep your EV insurance policy after a divorce, but you'll need to remove your ex-spouse from the policy. This can be done by contacting your insurance company and providing the necessary documentation. You might need to update your policy to reflect the changes in your marital status and driving habits.

#### How do I rebuild my insurance history after a divorce?

Rebuilding your insurance history after a divorce can be challenging, but it's not impossible. You can start by shopping around for new quotes and comparing rates from different companies. You might also consider working with an insurance broker who can help you find the best deals.

#### What are some tips for saving on EV insurance after a divorce?

Some tips for saving on EV insurance after a divorce include shopping around for quotes, asking about discounts, and considering a usage-based insurance policy. You might also consider bundling your EV insurance with other policies, such as homeowners or renters insurance, to save on premiums.

#### Can I get a discount on my EV insurance if I'm a divorced driver?

Yes, you might be eligible for discounts on your EV insurance as a divorced driver. Some companies offer discounts for low-mileage drivers, good students, or drivers who have completed a defensive driving course. Be sure to ask about these discounts when shopping for quotes.

#### How long does it take to rebuild my insurance history after a divorce?

Rebuilding your insurance history after a divorce can take time, but it's not impossible. You can start by shopping around for new quotes and comparing rates from different companies. You might also consider working with an insurance broker who can help you find the best deals. On average, it can take around 6-12 months to rebuild your insurance history, but this can vary depending on your specific circumstances.

The best policy is the one you actually understand. — Alex