Sarah used to pay $2,150 a year for her Tesla Model Y while commuting 18,000 miles to the office. After switching to full remote work her mileage dropped to 3,200 miles and she called Progressive for a fresh quote. They knocked it down to $1,180 with a pay-per-mile add-on and a home charging discount. That one change freed up nearly a grand she now spends on weekend trips instead of insurance.

Remote setups like hers are reshaping ev insurance for remote workers in 2026. Lower annual miles slash risk calculations and insurers are finally catching on with targeted discounts. But not every company plays fair on the details.

WARNING: Home Charging Setup Can Hide a Premium Trap

Plenty of remote workers assume plugging in at home automatically lowers rates. Some policies treat Level 2 chargers as an extra risk factor because of potential electrical faults. State Farm added a $180 surcharge last year for certain installs on Hyundai Ioniq 5 owners who skipped certified electrician checks. Know what the kicker is? You could end up paying more than a standard commuter if you skip the paperwork.

Check your wiring inspection receipts before renewal season. One Rivian driver in Oregon got hit with an extra $240 because his charger wasn't documented properly. That stung.

Does your current policy even list home charging discounts? Most do but you have to ask specifically or they stay buried in fine print.

COMPARISON: Remote Workers Versus Weekend Warriors on BMW iX Coverage

Compare a remote worker driving a BMW iX under 4,000 miles against a hybrid commuter who piles on 12,000 miles. The remote setup often beats the hybrid on total cost even though the BMW iX starts higher. Geico quoted $1,950 for the low-mileage iX owner versus $2,400 for the hybrid driver last quarter. Wild right?

The gap widens with usage-based tracking. Remote workers log steady short trips while commuters hit rush-hour variables that bump collision odds. Insurers like Allstate factor those patterns hard.

Still not convinced? Run both scenarios side by side on the same vehicle. The numbers flip expectations every time.

OK So Here's the Deal With Pay-Per-Mile Savings for Remote Lifestyles

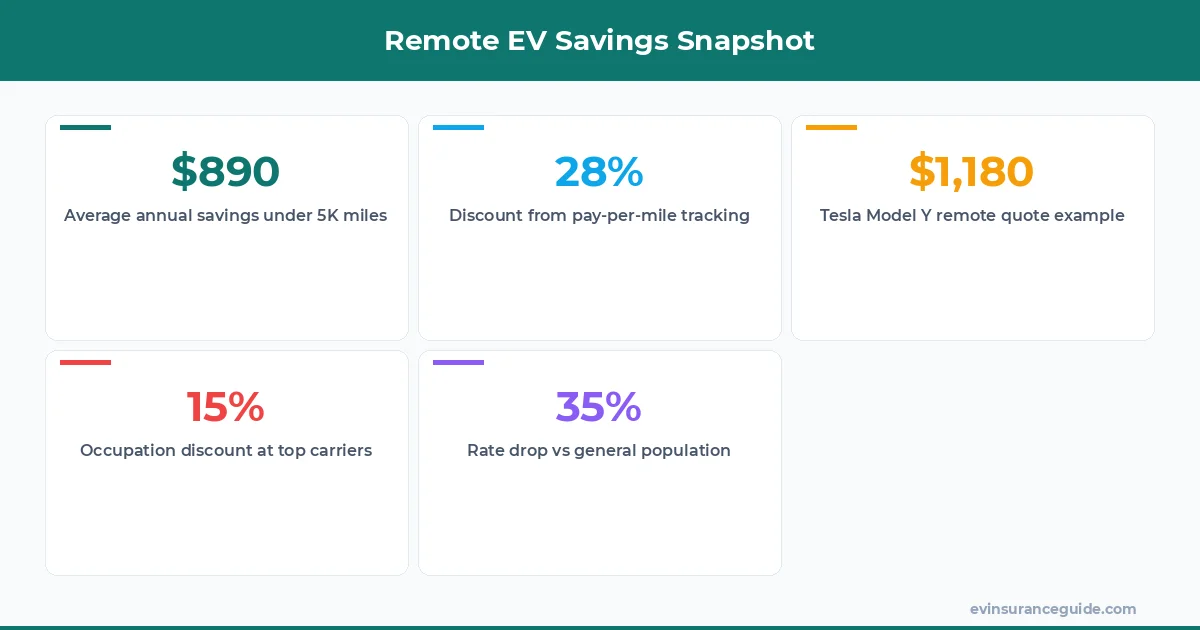

Pay-per-mile programs shine brightest when you barely crack 5,000 miles. Progressive and Metromile both cap base rates low then charge pennies per mile tracked. One Tesla Model 3 owner saved $890 last year by staying under 4,800 miles total.

Work from home schedules let you batch errands on one day instead of spreading risk across the week. That pattern triggers better renewal offers.

Why stick with flat-rate policies when your calendar already supports minimal driving? The math favors the flexible route.

How Much Does Ultra-Low Mileage Really Cut Your EV Insurance for Remote Workers?

Ultra-low mileage under 5,000 miles typically shaves 25-35% off standard EV premiums. For a Hyundai Ioniq 5 that drops average costs from $1,650 to around $1,120 with most major carriers. Occupation-specific discounts for remote workers add another 8-12% on top at companies like USAA.

Driving patterns matter more than raw totals. Short daily loops under 10 miles each keep claims low. Insurers reward that predictability.

Would you rather keep overpaying or adjust your quote to match your actual schedule?

5 Insurers Leading the Pack for Remote EV Drivers

Progressive tops the list with flexible mileage tracking and a 15% remote worker discount on Tesla Model 3 policies. State Farm follows closely offering home charging credits up to $200 annually. Geico ranks third thanks to quick pay-per-mile enrollment for Hyundai Ioniq 5 owners. Allstate provides solid occupation discounts for fully remote employees. USAA closes the top five with the deepest cuts for qualifying military remote workers.

Shop all five in one afternoon. The spread between best and worst quote often hits $700 on the same Rivian.

Pro tip: Bundle your EV with home insurance through the same carrier and watch another 10% disappear from the total bill.

Does switching to remote work automatically lower my rates?

Not automatically. You must notify the insurer and provide proof of mileage drop or updated commute status. Most companies require at least 60 days notice before renewal to lock in new ev insurance for remote workers pricing.

Can I get discounts for home charging only?

Yes. Several carriers now offer 5-10% credits when you prove exclusive home charging. Submit your charger installation invoice and utility statements showing no public station use.

What mileage threshold triggers the biggest savings?

Staying below 5,000 miles per year unlocks the steepest cuts. Progressive and similar providers drop rates sharply once you cross under that mark with consistent tracking data.

Are occupation discounts still available in 2026?

They remain strong for remote employees. Ask specifically for work-from-home or telecommuter classifications when quoting Tesla Model Y or BMW iX coverage.

How do pay-per-mile plans compare for EVs?

They often beat traditional policies by 20-30% for low-mileage drivers. Track your actual usage for three months and the savings become obvious on popular models like the Hyundai Ioniq 5.

Should I bundle with homeowners insurance?

Almost always. Bundling cuts another 8-15% and pairs nicely with home charging discounts already in place for remote setups.

Is usage-based tracking worth the privacy trade-off?

For most remote workers yes. The discount usually outweighs the data sharing and you can opt out after the first policy year if the numbers disappoint.

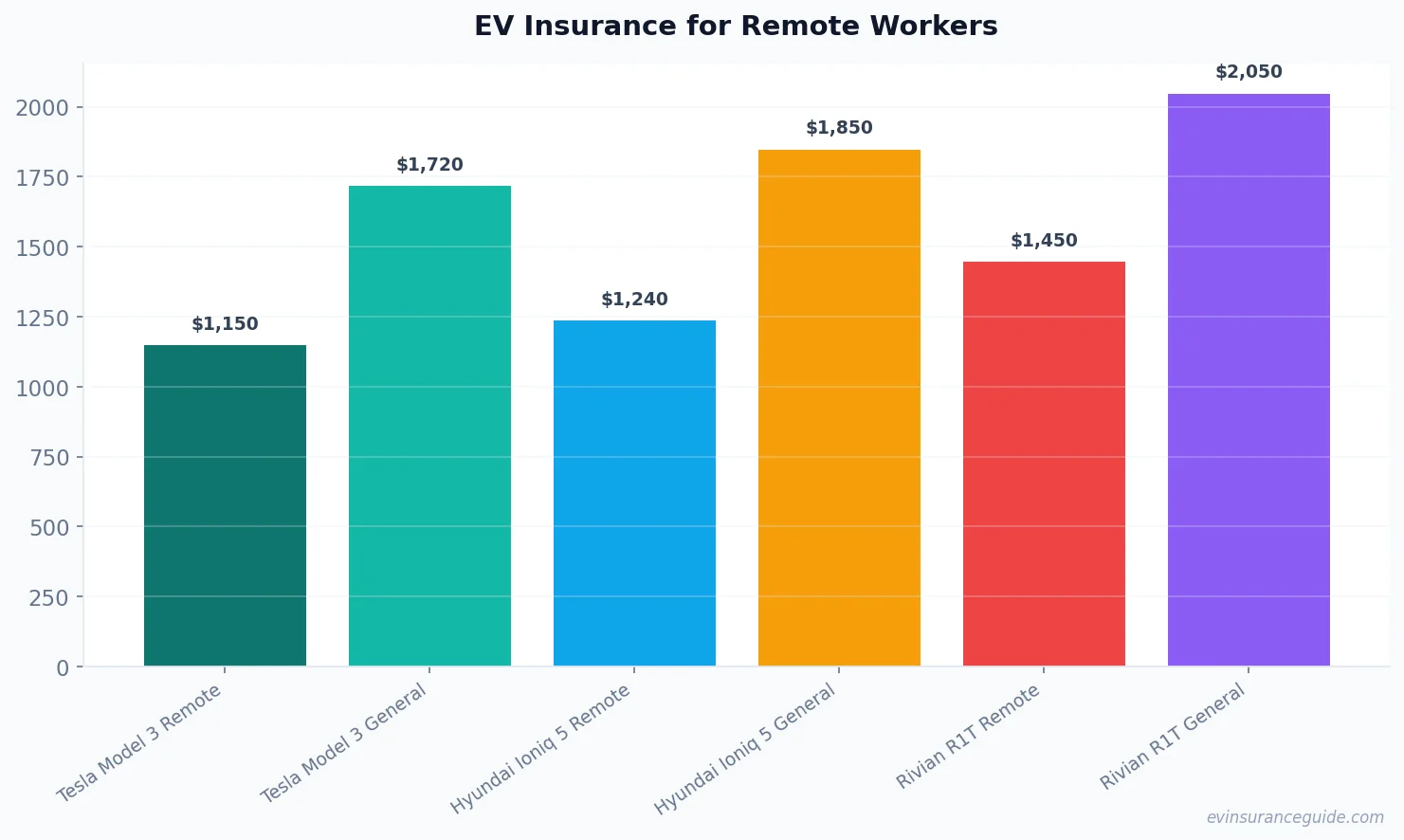

Chart data shows clear gaps between remote and general population rates across models. Remote workers on a Tesla Model Y average $1,210 while the broader group sits at $1,780. Similar spreads appear with the Rivian R1T at $1,450 versus $2,050.

Review your current policy against these patterns. Small adjustments to reporting and driving habits compound fast.

Go get yourself a better quote. You deserve it. — Alex