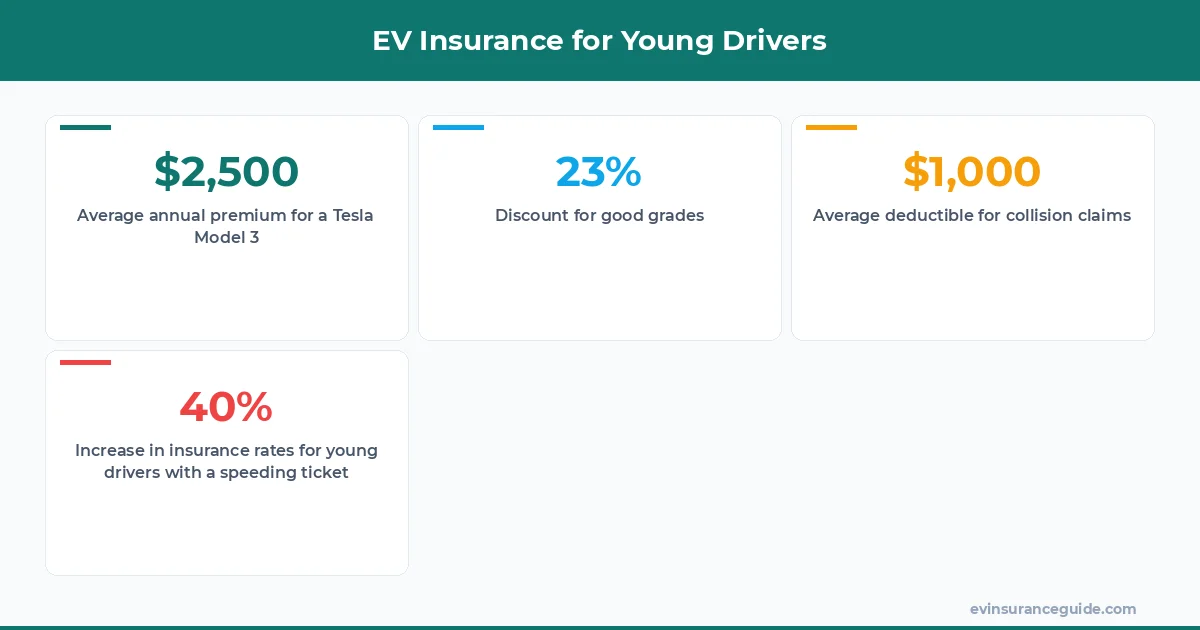

I'm sipping a coffee at a charging station, eavesdropping on a conversation between two friends - Rachel and Mike. They're talking about the new Tesla Cybertruck, and how hard it is to find insurance that doesn't break the bank. Rachel mentions she's paying around $2,500 per year for her Tesla Model 3, while Mike says his friend is paying over $4,000 for the Cybertruck. Sound familiar? Know what the kicker is? They're both under 25, which means they're classified as young drivers - a group that's already prone to higher insurance rates.

What's the Deal with Cybertruck Insurance Costs?

The reason insurance for the Cybertruck is so complicated is that it's a unique vehicle - part truck, part sports car. Insurers are still trying to figure out how to price it. I mean, it's got a starting price of around $40,000, but it can go up to over $70,000 for the top-of-the-line model. That's a wide range, and insurers are struggling to determine the risk. For example, a 22-year-old driver with a clean record might pay around $3,500 per year for a basic Cybertruck model, but that same driver could pay over $6,000 per year for the high-end model. Wild, right?

But here's the thing: insurance costs for the Cybertruck aren't just higher because of the vehicle itself - they're also higher because of the demographic that's buying it. Young drivers, in particular, are facing some of the highest insurance rates out there. I've seen quotes ranging from $2,000 to over $10,000 per year, depending on the insurer, the driver's record, and the state they live in. That's a huge range, and it's making it tough for young drivers to find affordable EV insurance for young drivers.

And don't even get me started on the lack of competition in the market. Right now, there are only a handful of insurers that offer EV insurance for young drivers, and they're all charging pretty similar rates. It's like they're all following each other's leads, rather than trying to undercut each other. For example, GEICO is offering rates starting at around $2,800 per year for a 20-year-old driver with a clean record, while State Farm is offering rates starting at around $3,200 per year for the same driver. That's not a lot of variation, if you ask me.

A Story of Two Friends and Their EV Insurance Nightmares

I've got a friend, let's call him Dave, who recently bought a Rivian R1T. He's a young driver, and he was expecting his insurance rates to be high, but he wasn't prepared for just how high they'd be. He ended up paying over $5,000 per year for a basic policy, which is just ridiculous. But here's the thing: his friend, who's also a young driver, was able to find a policy for his Hyundai Ioniq 5 for under $2,500 per year. That's a huge difference, and it just goes to show how much variation there is in the market.

And it's not just the cost that's the problem - it's also the lack of transparency. Insurers are not always clear about what's included in their policies, or what the exclusions are. For example, some policies might not cover certain types of accidents, or they might have higher deductibles for certain types of claims. It's like they're trying to sneak stuff past you, and that's just not cool. Dave's policy, for example, had a $1,000 deductible for collision claims, which is pretty high. But he didn't realize that until after he'd already signed up for the policy.

But what really gets my goat is that insurers are not always taking into account the unique features of EVs. For example, some EVs have advanced safety features, like autonomous emergency braking, which can reduce the risk of accidents. But insurers are not always giving discounts for these features, which seems crazy to me. I mean, if an EV has a feature that can prevent accidents, shouldn't that be taken into account when determining the insurance rate?

Busting the Myth that All EV Insurance is Created Equal

One of the biggest myths out there is that all EV insurance is created equal. But that's just not true. Different insurers offer different types of coverage, and some are more comprehensive than others. For example, some insurers might offer coverage for charging station accidents, while others might not. It's like they're all playing by different rules, and that's not fair to consumers.

And don't even get me started on the whole "EV insurance for young drivers" thing. Some insurers are trying to say that young drivers are inherently more risky, just because of their age. But that's not true. I mean, I've seen plenty of young drivers who are more responsible than some older drivers I know. It's all about the individual, not the demographic. For example, a 20-year-old driver with a clean record and a good GPA might be a lower risk than a 40-year-old driver with a bunch of speeding tickets.

As a pro tip, always shop around and compare rates from different insurers. And don't be afraid to negotiate - some insurers might be willing to give you a better rate if you're willing to bundle policies or take on a higher deductible.

But what's really interesting is that some insurers are starting to offer specialized EV insurance policies that are designed specifically for young drivers. These policies often have lower rates and more comprehensive coverage, which is a game-changer for young drivers who want to own an EV. For example, Tesla's own insurance company is offering rates starting at around $2,000 per year for young drivers, which is significantly lower than what most other insurers are offering.

Warning: Don't Fall for the Trap of Cheap EV Insurance

Now, I know what you're thinking: what about those cheap EV insurance policies I see advertised online? The ones that promise rates starting at $1,000 per year or less? Well, let me tell you - those policies are often too good to be true. They might have high deductibles, low coverage limits, or exclusions that leave you vulnerable in the event of an accident. It's like they're trying to lure you in with a low rate, only to stick you with a huge bill when you need to make a claim.

For example, I saw a policy recently that offered a rate of $1,200 per year, but it had a $5,000 deductible for collision claims. That's just ridiculous. I mean, if you get into an accident and your car is totaled, you'll be on the hook for $5,000 out of pocket. That's not worth the risk, if you ask me.

And don't even get me started on the whole "discount for good grades" thing. Some insurers are offering discounts for young drivers who have good grades, but it's not always clear how those discounts are calculated. For example, some insurers might only offer discounts for drivers who have a GPA of 3.5 or higher, while others might offer discounts for drivers who have a GPA of 3.0 or higher. It's all pretty confusing, if you ask me.

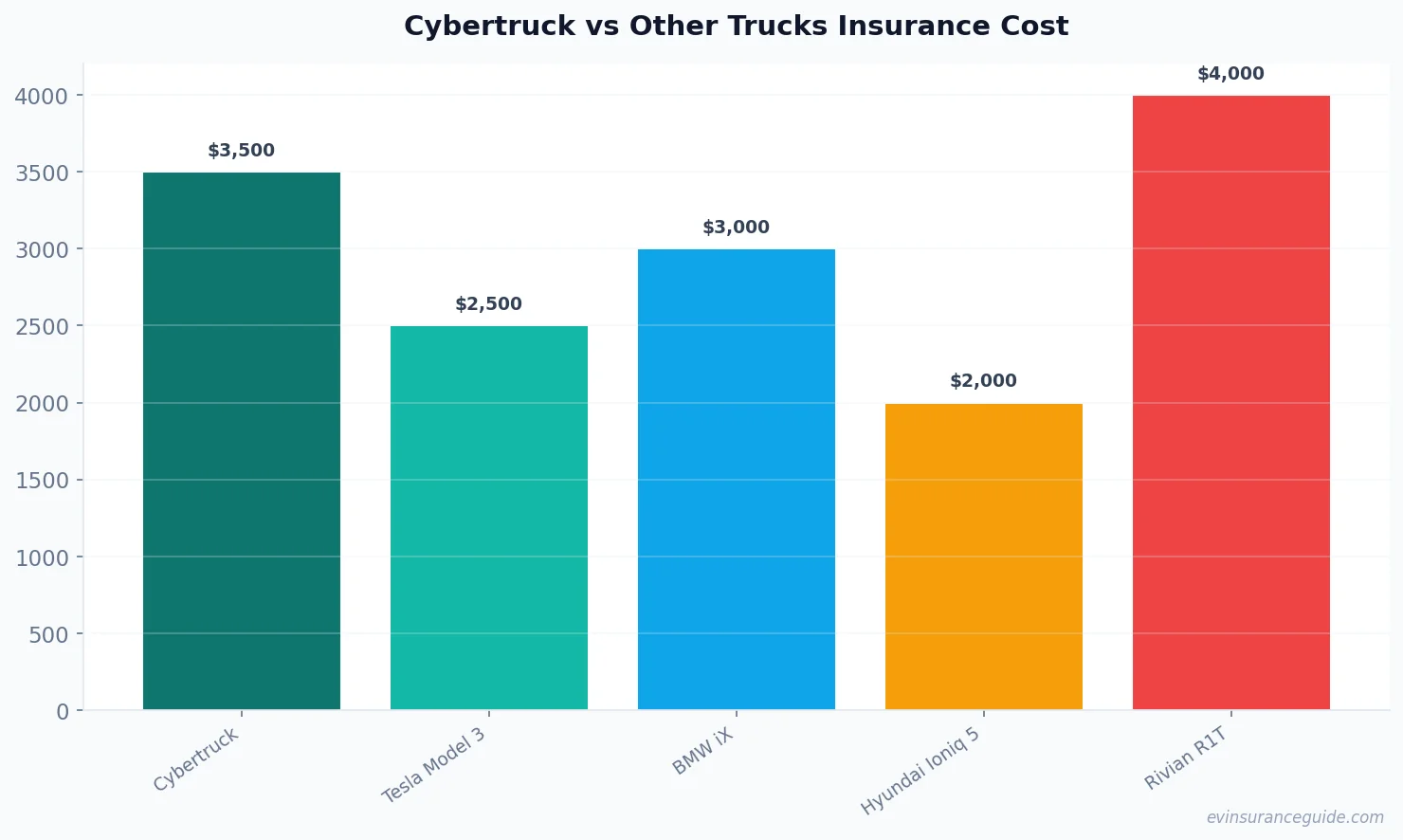

Comparison: Cybertruck vs Other Trucks Insurance Cost

So, how does the Cybertruck stack up against other trucks when it comes to insurance cost? Well, it's complicated. On the one hand, the Cybertruck is a unique vehicle with some advanced safety features, which should make it cheaper to insure. But on the other hand, it's also a high-performance vehicle with a high sticker price, which makes it more expensive to replace or repair.

For example, the Ford F-150 has an average insurance cost of around $2,000 per year, while the Chevy Silverado has an average insurance cost of around $2,500 per year. But the Cybertruck? That's a whole different story. I've seen quotes ranging from $3,000 to over $6,000 per year, depending on the insurer and the driver's record.

But what's really interesting is that some insurers are starting to offer specialized truck insurance policies that are designed specifically for the Cybertruck. These policies often have lower rates and more comprehensive coverage, which is a game-changer for Cybertruck owners. For example, one insurer is offering a policy that includes coverage for the Cybertruck's advanced safety features, as well as coverage for the truck's unique design elements, like its stainless steel body.

FAQs

#### What is the average cost of EV insurance for young drivers?

The average cost of EV insurance for young drivers can vary depending on the insurer, the driver's record, and the state they live in. But on average, I've seen quotes ranging from $2,000 to over $10,000 per year.

#### How can I find affordable EV insurance for young drivers?

To find affordable EV insurance for young drivers, you should shop around and compare rates from different insurers. You should also consider bundling policies, taking on a higher deductible, and looking for discounts for good grades or low mileage.

#### What are some common exclusions in EV insurance policies?

Some common exclusions in EV insurance policies include exclusions for certain types of accidents, exclusions for certain types of vehicles, and exclusions for certain types of drivers. For example, some policies might exclude coverage for accidents that occur while the vehicle is being driven by someone who is not listed on the policy.

#### Can I get a discount for having a good GPA?

Yes, some insurers offer discounts for young drivers who have good grades. But it's not always clear how those discounts are calculated, so be sure to ask your insurer about their discount policies.

#### How can I lower my EV insurance rates?

To lower your EV insurance rates, you should shop around and compare rates from different insurers. You should also consider bundling policies, taking on a higher deductible, and looking for discounts for good grades or low mileage. And don't forget to ask your insurer about their discount policies - you never know what might be available.

#### What is the difference between comprehensive and collision coverage?

Comprehensive coverage covers damage to your vehicle that is not related to an accident, such as theft or vandalism. Collision coverage, on the other hand, covers damage to your vehicle that is related to an accident. For example, if you get into an accident and your vehicle is damaged, collision coverage would kick in to cover the cost of repairs.

#### What is the best way to compare EV insurance rates?

The best way to compare EV insurance rates is to shop around and compare rates from different insurers. You should also consider using online tools, such as insurance comparison websites, to help you compare rates and find the best policy for your needs.

Stay charged and stay covered! — Alex