I'm standing at a charging station, sipping on a coffee, and overhearing a conversation between two EV owners about their insurance experiences. One of them mentions how they're paying over $2,000 a year for their Tesla Model 3, while the other is paying closer to $1,500 for their Hyundai Ioniq 5. Sound familiar? The difference in premium is staggering, and it got me thinking - what factors are at play here? Is it just the vehicle type, or are there other variables that determine your EV insurance score?

Teasing Out the Story

The conversation at the charging station was just the tip of the iceberg. As I started digging deeper, I realized that there are a multitude of factors that can affect your EV insurance premium. From the type of vehicle you drive to your driving history, it's a complex web of variables that can make or break your insurance costs. Know what the kicker is? Most people don't even realize what's going into their premium calculations. They just get a quote, and if it's within their budget, they're good to go. But what if you could save hundreds, even thousands of dollars by understanding the factors that determine your EV insurance score?

The EV lease vs buy insurance debate is a big one, and it's something that I've written about before. But this time, I want to dive deeper into the nitty-gritty of what affects your premiums. Take, for example, the BMW iX - a luxury EV that's sure to come with a higher price tag. But did you know that the insurance premiums for this vehicle can range from $1,800 to over $3,000 per year, depending on the state you live in and your driving history? That's a big difference, and it's not just the vehicle type that's causing it. There are 12 key variables that determine your EV insurance score, and understanding them can help you save big time.

8 Key Factors to Consider

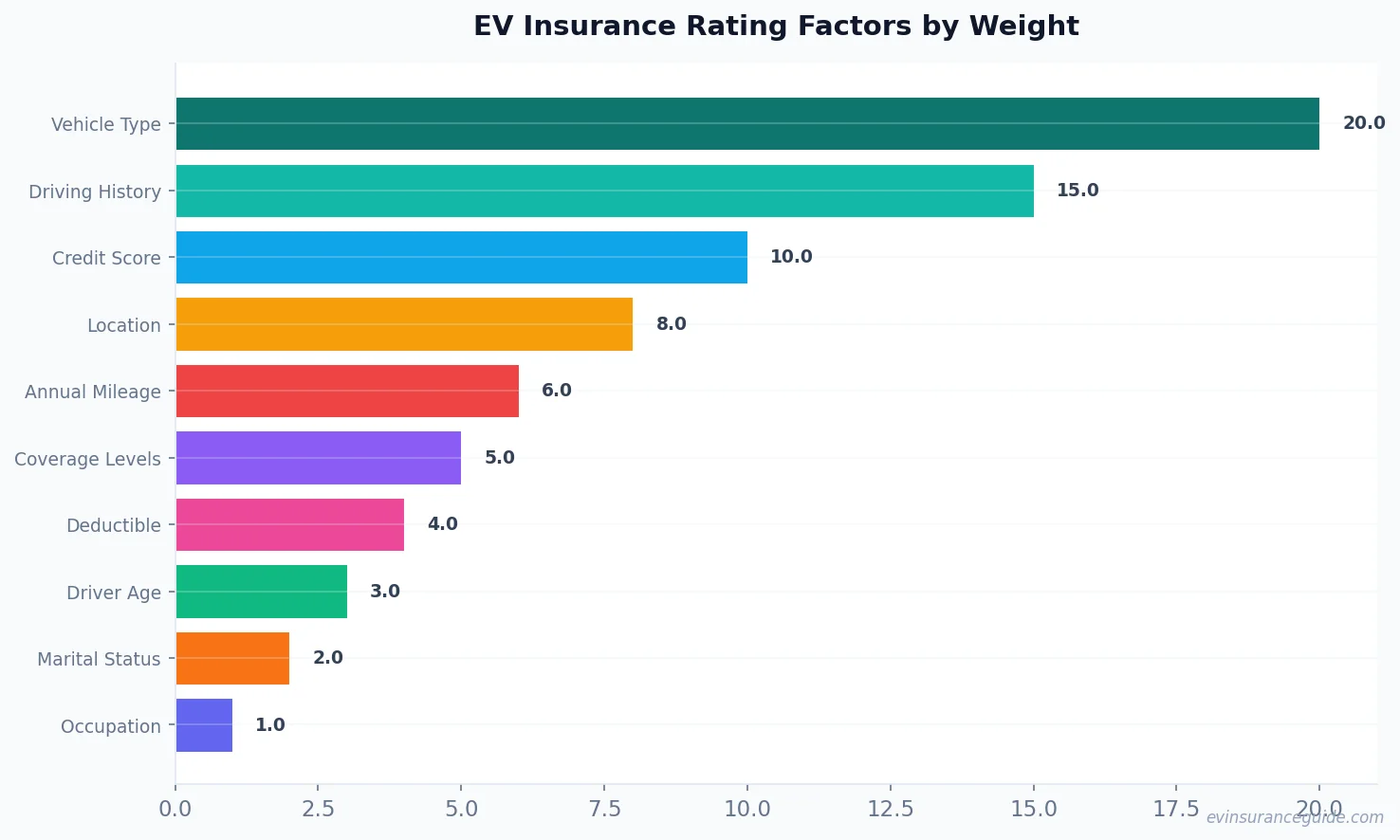

So, what are these 12 variables that I keep talking about? Well, let's break them down. First, there's the vehicle type - as I mentioned earlier, different vehicles come with different price tags, and that affects your insurance premiums. Then there's your driving history - if you've got a clean record, you'll likely pay less than someone with a few accidents under their belt. And don't even get me started on location - if you live in a state with high crime rates, you'll pay more for insurance. The list goes on - credit score, annual mileage, coverage levels, deductible, driver age, and marital status all play a role in determining your EV insurance score.

But here's the thing - not all insurance companies weigh these factors equally. Some might put more emphasis on your driving history, while others might care more about your credit score. And that's where the EV lease vs buy insurance debate comes in. If you're leasing an EV, you might be more likely to have a higher premium, since the insurance company is taking on more risk. But if you buy your EV outright, you might be able to negotiate a better rate. Wild, right? The variables are endless, and it's up to you to do your research and find the best deal.

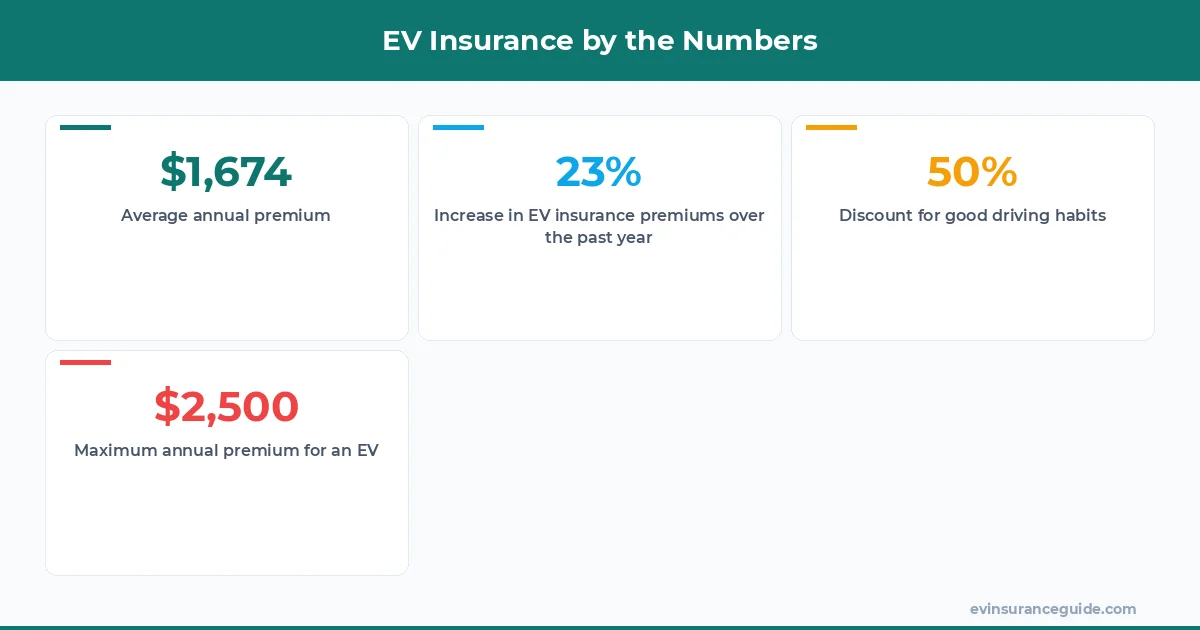

The cost of insurance can add up quickly - a study by the National Association of Insurance Commissioners found that the average annual premium for an EV is around $1,674. But that number can range from $1,200 to over $2,500, depending on the factors I mentioned earlier. And it's not just the upfront cost that you need to worry about - there are also ongoing costs, like maintenance and repairs, that can affect your bottom line. So, how do you navigate this complex landscape and come out on top?

Beware of Hidden Costs

There's a trap that many EV owners fall into - they get so caught up in the excitement of buying or leasing a new vehicle that they don't think about the long-term costs. And that's where the hidden costs come in. Take, for example, the cost of replacing a battery pack - it can range from $5,000 to over $10,000, depending on the type of vehicle you have. And if you're leasing, you might be on the hook for that cost, even if you're not planning on keeping the vehicle for the long haul. That one stung - I've seen people get caught off guard by these kinds of costs, and it's not pretty.

The EV lease vs buy insurance debate is all about weighing these kinds of costs and benefits. If you lease, you might have lower upfront costs, but you'll also have to deal with mileage limits and potential penalties for excessive wear and tear. And if you buy, you'll have more freedom to drive your vehicle as you please, but you'll also be on the hook for maintenance and repairs. It's a trade-off, and it's not always easy to know which way to go. But by understanding the factors that determine your EV insurance score, you can make a more informed decision.

As I was researching this article, I came across a quote from a insurance expert that really stuck with me:

The key to saving money on EV insurance is to understand the variables that determine your premium. By doing your research and shopping around, you can find the best deal for your needs and budget.

It's not always easy, but it's worth it in the end. The cost savings can be significant - I've seen people save up to $500 per year by switching to a different insurance company. And that's not even counting the potential benefits of leasing vs buying - if you lease, you might be able to drive a newer vehicle for less money, which can be a big perk.

My Honest Opinion

The truth is, the EV lease vs buy insurance debate is all about trade-offs. There's no one-size-fits-all solution, and what works for one person might not work for another. But by understanding the factors that determine your EV insurance score, you can make a more informed decision. And my honest opinion is that buying your EV outright is usually the way to go - you'll have more freedom to drive your vehicle as you please, and you won't have to worry about mileage limits or penalties for excessive wear and tear.

That being said, leasing can be a good option for some people. If you're someone who likes to drive a new vehicle every few years, leasing might be the way to go. And if you're not planning on keeping your vehicle for the long haul, leasing can be a good way to avoid the long-term costs of maintenance and repairs. But for most people, buying is the way to go. You'll have more control over your vehicle, and you won't have to worry about the potential pitfalls of leasing.

The cost of insurance is just one part of the equation - you also need to think about the overall cost of ownership. And that's where the EV lease vs buy insurance debate comes in. If you lease, you might have lower upfront costs, but you'll also have to deal with ongoing costs like maintenance and repairs. And if you buy, you'll have more freedom to drive your vehicle as you please, but you'll also be on the hook for those costs. It's a trade-off, and it's not always easy to know which way to go.

What Determines Your EV Insurance Score?

So, what determines your EV insurance score? Is it just the vehicle type, or are there other factors at play? The answer is complicated - it's a combination of both. The type of vehicle you drive is just one part of the equation - your driving history, credit score, and location all play a role in determining your EV insurance score. And it's not just the insurance company that's looking at these factors - lenders and other financial institutions are also taking a close look.

The cost of insurance can vary widely depending on these factors - a study by the Insurance Institute for Highway Safety found that the average annual premium for an EV can range from $1,200 to over $2,500. And it's not just the cost of insurance that you need to worry about - there are also ongoing costs like maintenance and repairs that can affect your bottom line. So, how do you navigate this complex landscape and come out on top?

FAQs

#### What is the average cost of EV insurance?

The average cost of EV insurance is around $1,674 per year, although this can range from $1,200 to over $2,500 depending on the factors I mentioned earlier.

#### How does the EV lease vs buy insurance debate affect my premium?

The EV lease vs buy insurance debate can affect your premium in a big way. If you lease, you might have lower upfront costs, but you'll also have to deal with mileage limits and potential penalties for excessive wear and tear. And if you buy, you'll have more freedom to drive your vehicle as you please, but you'll also be on the hook for maintenance and repairs.

#### What are the 12 key variables that determine my EV insurance score?

The 12 key variables that determine your EV insurance score are: vehicle type, driving history, credit score, location, annual mileage, coverage levels, deductible, driver age, marital status, occupation, education level, and income.

#### How can I save money on EV insurance?

You can save money on EV insurance by understanding the variables that determine your premium and shopping around for the best deal. You can also consider leasing vs buying, and look into discounts for things like good driving habits and low mileage.

#### What are the benefits of buying an EV outright?

The benefits of buying an EV outright include having more freedom to drive your vehicle as you please, and not having to worry about mileage limits or penalties for excessive wear and tear. You'll also have more control over your vehicle, and you won't have to deal with the potential pitfalls of leasing.

#### Can I negotiate a better rate with my insurance company?

Yes, you can negotiate a better rate with your insurance company. By understanding the factors that determine your EV insurance score and doing your research, you can make a strong case for a lower premium. And if you're not happy with the rate you're being offered, you can always shop around and look for a better deal.

The EV lease vs buy insurance debate is complicated, but by understanding the factors that determine your EV insurance score, you can make a more informed decision. And my honest opinion is that buying your EV outright is usually the way to go - you'll have more freedom to drive your vehicle as you please, and you won't have to worry about mileage limits or penalties for excessive wear and tear.

Until next time — Alex