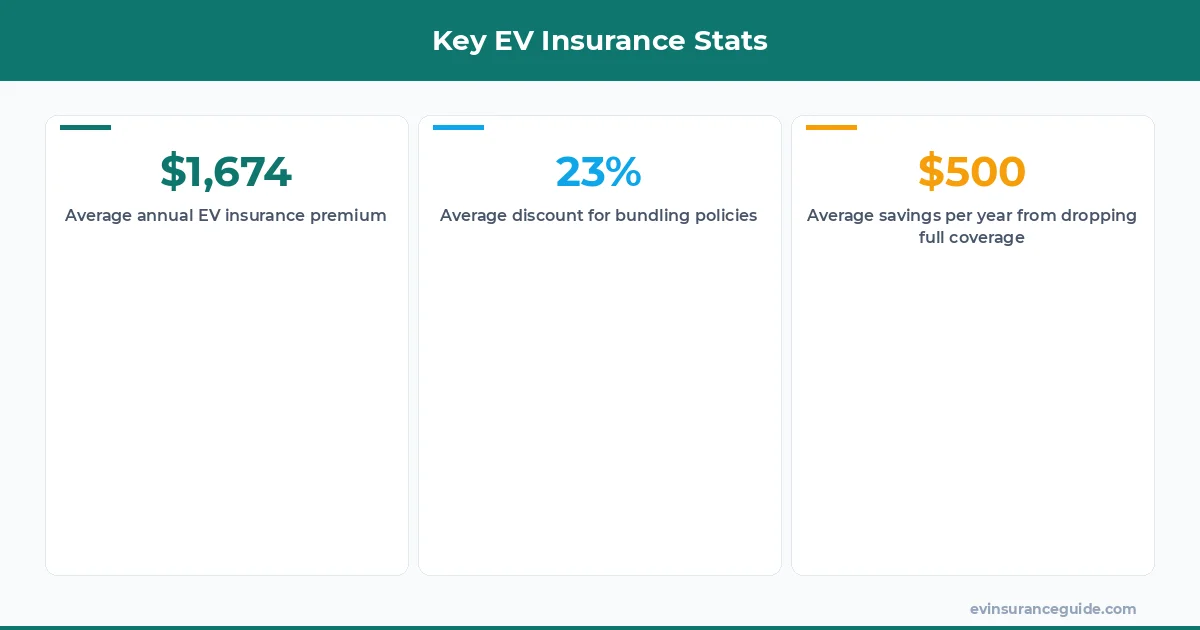

Ugh, the EV insurance world can be a real headache - I'm talking $2,000+ annual premiums for a Tesla Model 3, with some insurers quoting as high as $3,500. Sound familiar? You're not alone. I've seen it time and time again: EV owners getting ripped off by insurance companies that don't understand the tech. Well, actually... it's not just about understanding the tech - it's about finding the right policy. And that's where we come in.

MYTH_BUST — You Don't Need Full Coverage for Your EV

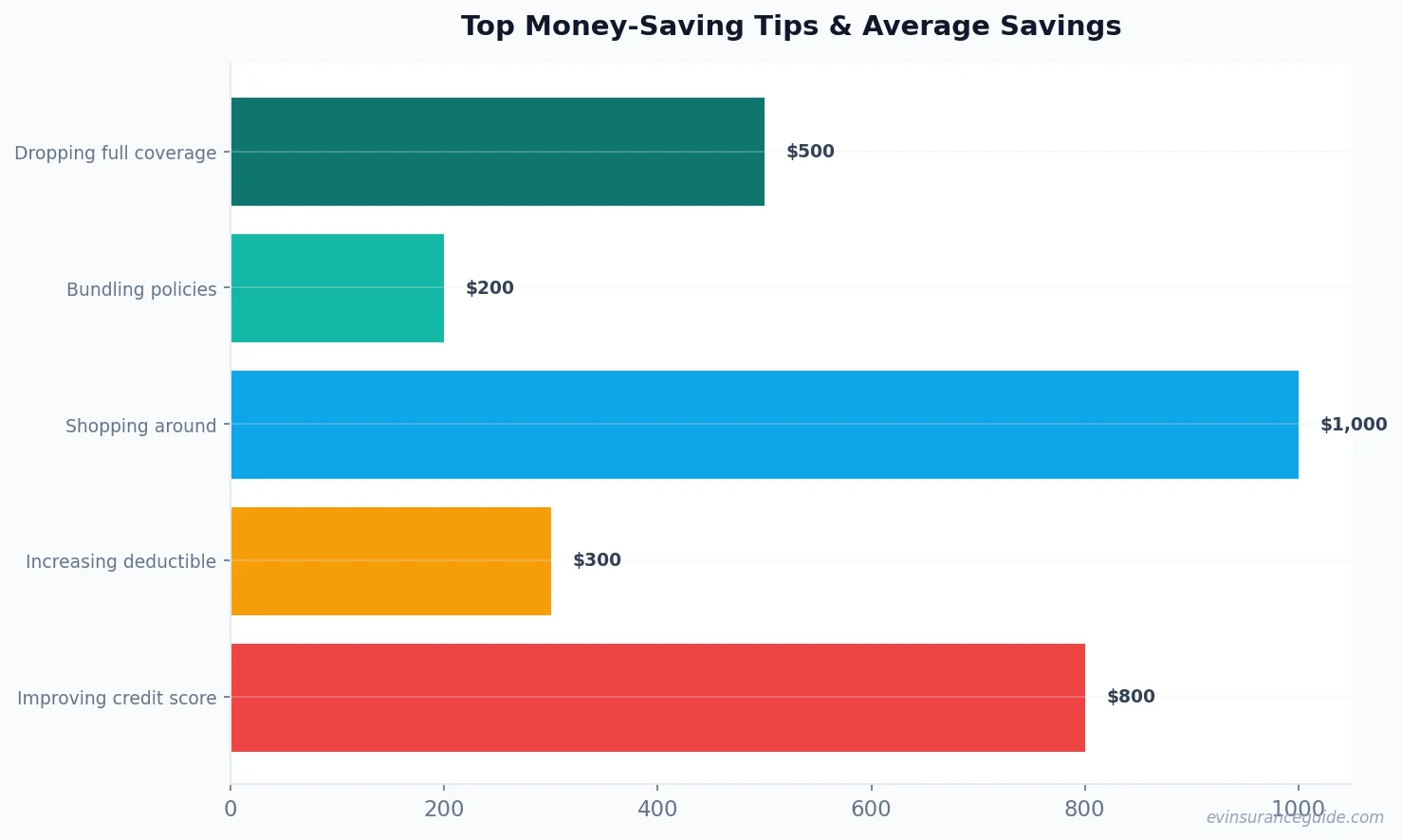

Let's get one thing straight: you don't need full coverage for your EV. I mean, think about it - most EVs depreciate pretty quickly, so comprehensive and collision coverage might not be worth the cost. For example, if you've got a 2020 Hyundai Ioniq 5 with 30,000 miles on it, you might be able to get away with just liability coverage. That could save you around $500-$700 per year, depending on your insurer and location. Know what the kicker is? Some insurers, like Geico, will actually give you a discount for dropping full coverage.

Now, I know what you're thinking: what about if I get into an accident? Won't I be stuck with a huge bill? And to that, I say... not necessarily. If you've got a good emergency fund in place, you might be able to cover the costs of repairs or even a new vehicle. Of course, that's not always the case - but it's definitely worth considering. For instance, if you've got a Rivian with a $10,000 deductible, you might want to think twice about dropping full coverage.

But here's the thing: even if you do need full coverage, there are still ways to lower your premium. One way is to shop around - don't just stick with the first insurer you find. I mean, I've seen people save up to $1,000 per year just by switching to a different insurer. That's crazy, right? Wild, right? Another way is to take advantage of discounts. For example, some insurers offer discounts for EV owners who also own a home or have a good driving record.

WARNING — Don't Fall for the 'Bundle and Save' Trap

OK, so you're probably thinking: what about bundling my EV insurance with my home or life insurance? Doesn't that always save me money? Nope. Not always. In fact, sometimes bundling can actually cost you more in the long run. I've seen it happen to people who own a BMW iX - they bundle their insurance with their home insurer, only to find out they're paying an extra $500 per year for the 'convenience' of having all their policies in one place. That one stung.

Now, I'm not saying bundling never saves you money. Sometimes it does - especially if you've got a lot of policies with the same insurer. But you gotta do the math, you know? Don't just assume that bundling is the way to go. For example, if you've got a Tesla Model Y and you're paying $1,200 per year for insurance, you might want to compare that to the cost of bundling with your home insurer. If the bundled rate is $1,500 per year, then it's probably not worth it.

And hey, while we're on the topic of warnings... be careful of insurers that try to sell you 'add-ons' like roadside assistance or rental car coverage. Those can add up quickly - and they're often not worth the cost. I mean, think about it: if you've got a reliable EV like a Hyundai Kona Electric, you might not need roadside assistance at all. That could save you an extra $100-$200 per year.

CASUAL_DIRECT — OK So Here's the Deal With EV Lease vs Buy Insurance

So, you're probably wondering: what's the deal with ev lease vs buy insurance? Well, here's the thing: leasing an EV can actually save you money on insurance. I know, I know - it sounds counterintuitive. But hear me out. When you lease an EV, you're not actually owning the vehicle - the lessor is. And that means they're often responsible for insuring the vehicle, not you. That can save you around $500-$1,000 per year, depending on the terms of your lease.

For example, if you're leasing a Tesla Model 3 for 3 years, you might not need to pay for comprehensive or collision coverage at all. That's because the lessor will typically cover those costs. And that means you can save even more money on your insurance premium. But, of course, there are some caveats. If you're leasing an EV, you'll often need to pay a higher deductible in the event of an accident. And that can be a real pain - especially if you're not prepared.

HONEST_OPINION — EV Insurance Companies Are Gouging Us

Let's be real: EV insurance companies are gouging us. I mean, think about it: EVs are generally safer than gas-powered vehicles, with features like automatic emergency braking and lane departure warning. And they're also often more expensive to repair - but that's not always the case. So, why are we paying so much for insurance? It doesn't add up.

I've got a friend who owns a Rivian, and he's paying over $2,500 per year for insurance. That's just crazy. And it's not like he's got a bad driving record or anything - he's a perfect driver. So, what's going on here? It's like insurers are just taking advantage of us because we're EV owners. Well, I've got news for them: we're not going to take it lying down.

COMPARISON — EV Lease vs Buy Insurance: Which One Wins?

So, which one is better: ev lease vs buy insurance? Well, it really depends on your situation. If you're someone who likes to drive a new vehicle every few years, then leasing might be the way to go. You'll save money on insurance, and you'll also get to enjoy the latest and greatest EV tech. But, if you're someone who likes to own your vehicle outright, then buying might be the better option.

For example, if you're planning to keep your EV for 10+ years, then buying might make more sense. You'll pay more upfront, but you'll also save money in the long run. And, of course, you'll have the freedom to modify your vehicle however you want - which can be a real perk for some people. On the other hand, if you're leasing an EV, you'll often be subject to mileage limits and other restrictions. So, it's really a trade-off.

FAQs

#### What's the average cost of EV insurance?

The average cost of EV insurance varies widely depending on your location, vehicle, and driving history. But, on average, you can expect to pay around $1,500-$2,500 per year for a Tesla Model 3 or similar vehicle.

#### Can I get a discount for being an EV owner?

Yes, some insurers offer discounts for EV owners. For example, Allstate offers a 10% discount for EV owners who also own a home. And, of course, there are other discounts available for things like good driving records and low mileage.

#### How can I lower my EV insurance premium?

There are lots of ways to lower your EV insurance premium. One way is to shop around and compare rates from different insurers. Another way is to take advantage of discounts - like the ones I mentioned earlier. And, of course, you can also try dropping full coverage or raising your deductible.

#### What's the difference between ev lease vs buy insurance?

The main difference between ev lease vs buy insurance is who's responsible for insuring the vehicle. When you lease an EV, the lessor is typically responsible for insuring the vehicle - which can save you money on your premium. But, when you buy an EV, you're responsible for insuring the vehicle yourself.

#### Can I customize my EV insurance policy?

Yes, you can often customize your EV insurance policy to fit your needs. For example, you might be able to add or remove coverage for things like roadside assistance or rental car coverage. And, of course, you can also adjust your deductible and coverage limits to suit your budget.

#### How do I know if I'm getting a good deal on my EV insurance?

One way to know if you're getting a good deal on your EV insurance is to compare rates from different insurers. You can also try using online tools or consulting with an insurance agent to get a sense of what you should be paying. And, of course, you should always read the fine print and make sure you understand what's covered and what's not.

Pro tip: always review your policy carefully before signing - and make sure you understand what's covered and what's not. You don't want to be stuck with a huge bill because you didn't read the fine print.

And, finally, here's a blockquote with some key stats:

The average EV owner saves around $700 per year by switching to a different insurer. And, by shopping around and comparing rates, you can save even more. So, don't be afraid to do your research and find the best deal for your EV insurance needs.

Yeah I know, another insurance article. But hear me out. The key to saving money on your EV insurance is to be informed - and to shop around. Don't just stick with the first insurer you find - compare rates and coverage options to find the best deal for your needs. And, of course, don't be afraid to negotiate or ask about discounts. With a little bit of effort, you can save hundreds or even thousands of dollars per year on your EV insurance.

Cheers from the EV insurance trenches. — Alex