OK so someone DM'd me this question: what's the difference between EV lease vs buy insurance, and how can I actually save money on my premium? Sound familiar? I've been in the insurance game for five years, and I've seen people overspend on their EV insurance by thousands of dollars. That one stung. I'm gonna give you the lowdown on the top 50 terms you need to know as an electric car owner.

A Story of EV Insurance Woes

I've got a buddy, let's call him Ryan, who leased a Tesla Model 3 and ended up paying $2,500 per year for insurance. He thought he was getting a good deal, but it turned out he was overinsured. Know what the kicker is? He could've saved $800 per year if he'd gone with a different provider. Wild, right? Now, Ryan's a savvy guy, but even he got taken for a ride. Don't be like Ryan – take control of your EV insurance.

When you're shopping for EV lease vs buy insurance, you're gonna come across a lot of jargon. Don't worry, I've got you covered. For example, did you know that the BMW iX has a higher insurance premium than the Hyundai Ioniq 5? It's true – and it's all because of the vehicle's value and safety features. The Ioniq 5, on the other hand, is a more affordable option, with insurance premiums starting at around $1,200 per year.

As you're reading this, you might be wondering: what's the best way to save money on my EV insurance? Well, actually, it's not that hard. You just need to understand the terms and conditions of your policy. For instance, if you're leasing an EV, you'll need to consider the cost of gap insurance, which can range from $20 to $50 per month. But if you're buying an EV outright, you might not need gap insurance at all. That's a potential saving of $600 per year.

EV Lease vs Buy Insurance: The Ultimate Showdown

When it comes to EV lease vs buy insurance, there are some key differences you need to know. For one, leased EVs typically require more comprehensive coverage, which can drive up your premium. On the other hand, bought EVs can be insured with a more basic policy, which can save you money. But here's the thing: leased EVs often come with lower monthly payments, which can offset the higher insurance cost. It's a trade-off, really. You gotta weigh your options and decide what's best for you.

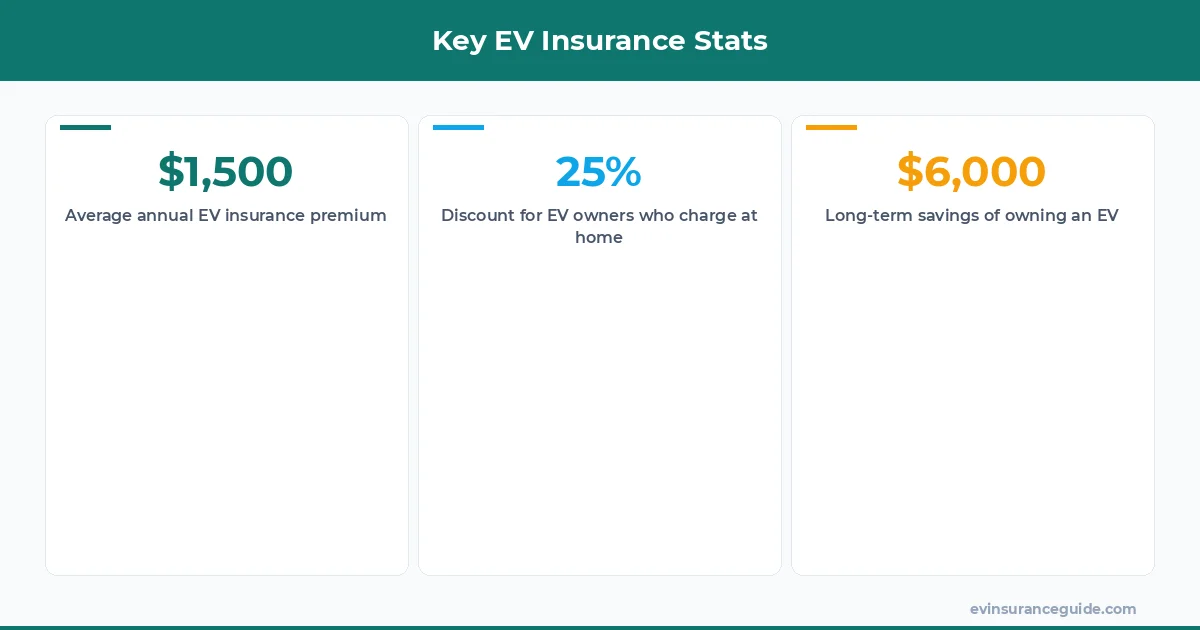

Let's take a look at some numbers. According to a study by the National Association of Insurance Commissioners, the average annual premium for an EV is around $1,500. But if you're leasing an EV, you might end up paying closer to $2,000 per year. That's a big difference, especially if you're on a tight budget. But if you're buying an EV, you might be able to get away with paying as little as $1,000 per year. It's all about the specifics of your policy and your vehicle.

Now, I know some of you are thinking: what about Rivian? How does their insurance premium compare to other EVs? Well, actually, Rivian's insurance premium is pretty competitive, starting at around $1,800 per year. But if you're looking for an even better deal, you might want to consider the Nissan Leaf, which has an insurance premium of around $1,400 per year. It's all about doing your research and finding the best option for your needs.

The Myth of EV Insurance Being Too Expensive

There's a myth out there that EV insurance is too expensive, and that it's not worth the cost. But that's just not true. While it's true that EVs can be more expensive to insure than gas-powered vehicles, the cost is still relatively affordable. And when you consider the long-term savings of owning an EV, it's a no-brainer. For example, a study by the Union of Concerned Scientists found that EV owners can save up to $6,000 over the lifespan of their vehicle. That's a pretty big deal, if you ask me.

But what about the cost of replacement parts? Won't that drive up the insurance premium? Not necessarily. Many insurance providers offer specialized EV policies that take into account the unique needs of electric vehicles. For instance, some providers offer discounts for EV owners who charge their vehicles at home, rather than on the go. That's a smart way to save money, if you ask me.

And let's not forget about the environmental benefits of owning an EV. Not only are they better for the planet, but they're also a great way to reduce your carbon footprint. So, even if the insurance premium is a bit higher, it's still worth it in the long run. As the saying goes: you get what you pay for. And when it comes to EV insurance, you're paying for a lot more than just a policy – you're paying for peace of mind.

Pro tip: always read the fine print on your insurance policy, especially when it comes to EV lease vs buy insurance. You don't want to get stuck with a policy that doesn't cover you adequately. And don't be afraid to shop around – different providers offer different rates, so it's worth doing your research.

OK So Here's the Deal With EV Insurance Terms

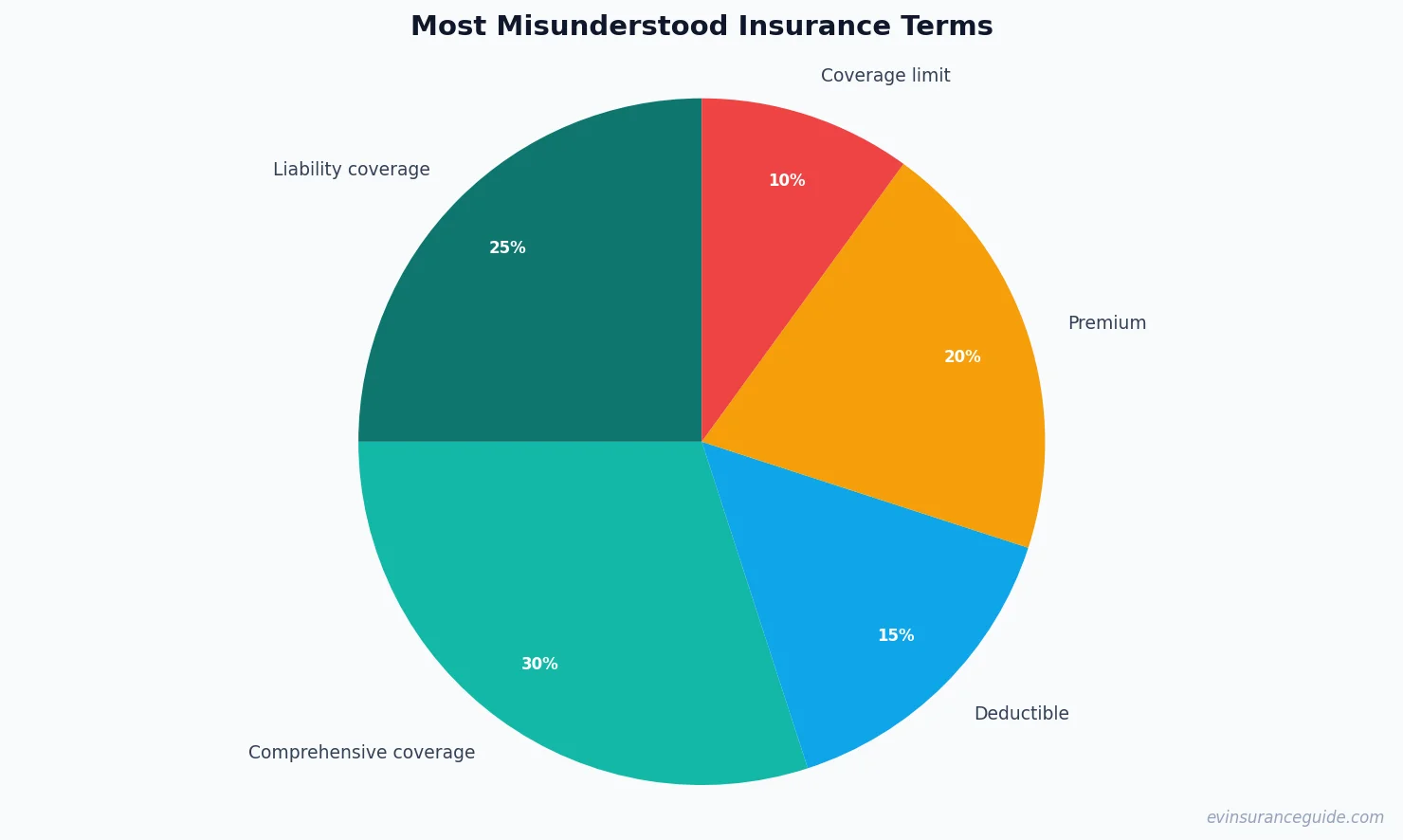

When it comes to EV insurance, there are a lot of terms to keep track of. From liability coverage to comprehensive coverage, it can be overwhelming. But don't worry, I've got you covered. Here are some key terms to know: deductible, premium, and coverage limit. These are the basics, but they're essential to understanding your policy.

For example, if you're leasing a Tesla Model Y, you'll want to make sure you have a comprehensive policy that covers you in case of an accident. And if you're buying a Hyundai Kona Electric, you'll want to consider a policy with a lower deductible. It's all about finding the right balance between cost and coverage. And don't even get me started on the importance of gap insurance – that's a whole other can of worms.

But what about the cost of insurance for different EV models? Well, actually, it varies widely. For instance, the insurance premium for a Nissan Leaf is around $1,400 per year, while the premium for a BMW iX is closer to $2,200 per year. That's a big difference, especially if you're on a tight budget. But if you're willing to shop around, you can find a policy that fits your needs and your budget.

10 Essential EV Insurance Terms You Need to Know

Here are the top 10 terms you need to know when it comes to EV lease vs buy insurance:

- 1. Liability coverage: this is the part of your policy that covers you in case you're involved in an accident.

- 2. Comprehensive coverage: this is the part of your policy that covers you in case your vehicle is damaged or stolen.

- 3. Deductible: this is the amount you pay out of pocket before your insurance kicks in.

- 4. Premium: this is the amount you pay for your insurance policy.

- 5. Coverage limit: this is the maximum amount your insurance will pay in case of an accident or damage.

- 6. Gap insurance: this is the type of insurance that covers you if your vehicle is totaled and you still owe money on your lease.

- 7. EV-specific insurance: this is a type of insurance that's designed specifically for electric vehicles.

- 8. Charging station insurance: this is the type of insurance that covers you in case you're charging your vehicle at a public station.

- 9. Home charging station insurance: this is the type of insurance that covers you in case you're charging your vehicle at home.

- 10. Roadside assistance: this is the type of insurance that covers you in case you break down on the side of the road.

What's the difference between EV lease vs buy insurance?

The main difference between EV lease vs buy insurance is the level of coverage you need. If you're leasing an EV, you'll typically need more comprehensive coverage to protect the vehicle. But if you're buying an EV, you may be able to get away with a more basic policy.

Can I save money on my EV insurance premium?

Yes, you can save money on your EV insurance premium by shopping around and comparing rates. You can also consider raising your deductible or dropping certain types of coverage.

What's the average cost of EV insurance?

The average cost of EV insurance is around $1,500 per year. But this can vary widely depending on the type of vehicle you have, your driving history, and your location.

Do I need gap insurance for my EV?

If you're leasing an EV, you may need gap insurance to protect yourself in case the vehicle is totaled and you still owe money on your lease. But if you're buying an EV, you may not need gap insurance.

Can I get a discount on my EV insurance premium?

Yes, you may be able to get a discount on your EV insurance premium by installing safety features such as anti-theft devices or by taking a defensive driving course.

How do I choose the right EV insurance policy?

To choose the right EV insurance policy, you'll need to consider your specific needs and budget. You'll also want to shop around and compare rates from different providers.

What's the most important thing to consider when buying EV insurance?

The most important thing to consider when buying EV insurance is the level of coverage you need. You'll want to make sure you have enough coverage to protect yourself and your vehicle in case of an accident or damage.

Go get yourself a better quote. You deserve it.

— Alex