I was sipping coffee at a charging station, listening in on a conversation between two EV owners, Rachel and Mike, about their insurance experiences. They were discussing the pros and cons of various add-ons, from roadside assistance to gap insurance. Rachel, a Tesla Model 3 owner, was considering adding a new driver to her policy, while Mike, who drives a BMW iX, was looking to save money by dropping some unnecessary features. Sound familiar? Know what the kicker is? Most EV owners don't fully understand what they're paying for.

OK So Here's the Deal With EV Insurance Add-Ons

EV lease vs buy insurance - it's a crucial distinction, especially when it comes to add-ons. If you're leasing an EV, like a Hyundai Ioniq 5, your insurance needs will differ from those of an owner. For instance, lease agreements often require specific coverage types, such as gap insurance, which can cost between $50 to $200 per year. That one stung, right? On the other hand, owners have more flexibility in choosing their add-ons. A friend, let's call him Alex (nope, not me), recently bought a Rivian and opted for a comprehensive policy with a $500 deductible, which cost him around $1,500 annually.

When comparing EV lease vs buy insurance, consider the total cost of ownership. Leasing often means lower upfront costs, but higher insurance premiums in the long run. For example, a leased Tesla Model Y might have a monthly insurance premium of $150, while an owned Model Y could have a lower premium of $100 per month. Wild, right? This difference can add up over the life of the lease. And, with the rising popularity of EVs, insurance companies are starting to offer more competitive rates for owners. Well, actually, it's all about the data - insurers are using advanced analytics to better understand EV risks and adjust their pricing accordingly.

Busting the Myth: All EV Insurance Add-Ons Are Necessary

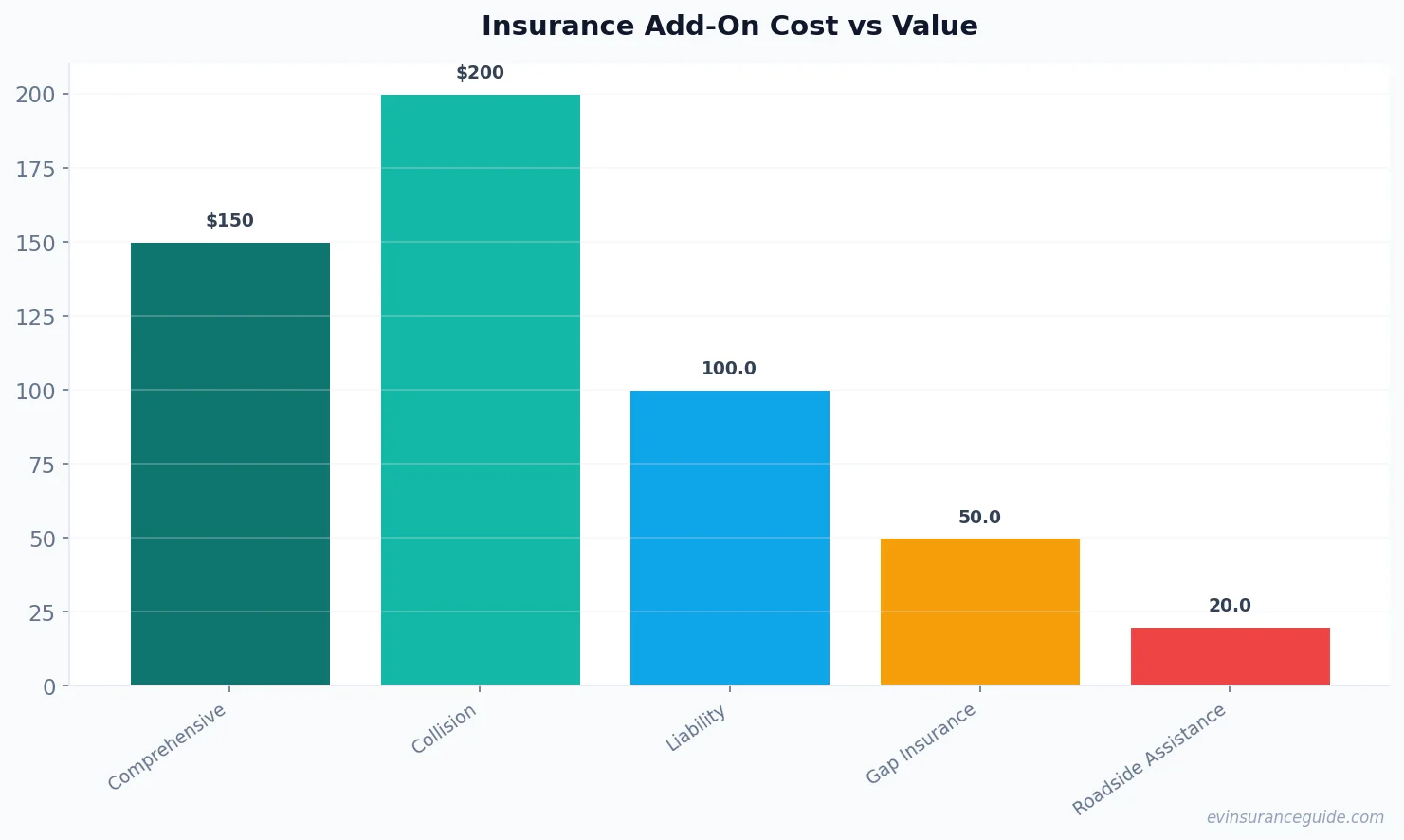

Myth busted: not all add-ons are created equal. Some, like roadside assistance, can be valuable, especially if you drive an EV with limited charging infrastructure, like in rural areas. A roadside assistance package can cost around $20 to $50 per year, depending on the provider. However, others, such as windshield repair, might not be worth the extra cost. For instance, a study by the National Association of Insurance Commissioners found that windshield repair claims average around $500. If your deductible is $500 or higher, it might not make sense to add this coverage. But, hey, if you're driving a luxury EV like a Tesla or BMW, you might want to consider it. Hmm, let me rethink that - what if you're driving an EV with advanced safety features, like a Rivian? In that case, the likelihood of a windshield claim is lower, making this add-on less necessary.

As we... no, scratch that - let's be real, insurance companies often try to sell you more coverage than you need. It's your job to do the research and decide what's essential. For example, if you're leasing an EV, you might not need to add rental car coverage, as your lease agreement might already include this benefit. On the other hand, if you own an EV, you might want to consider adding this coverage to ensure you're not left without a vehicle in case of an accident. Know what I mean?

5 Key Add-Ons to Consider for Your EV Insurance

When it comes to EV lease vs buy insurance, there are certain add-ons that can make a big difference. Here are five key ones to consider:

- gap insurance,

- roadside assistance,

- comprehensive coverage,

- collision coverage, and

- umbrella insurance. Yeah, I know, another insurance article. But hear me out - these add-ons can help you save money in the long run. For instance, gap insurance can cover the difference between the actual cash value of your EV and the amount you owe on your lease or loan. This can be especially important for EVs, which tend to depreciate faster than traditional vehicles.

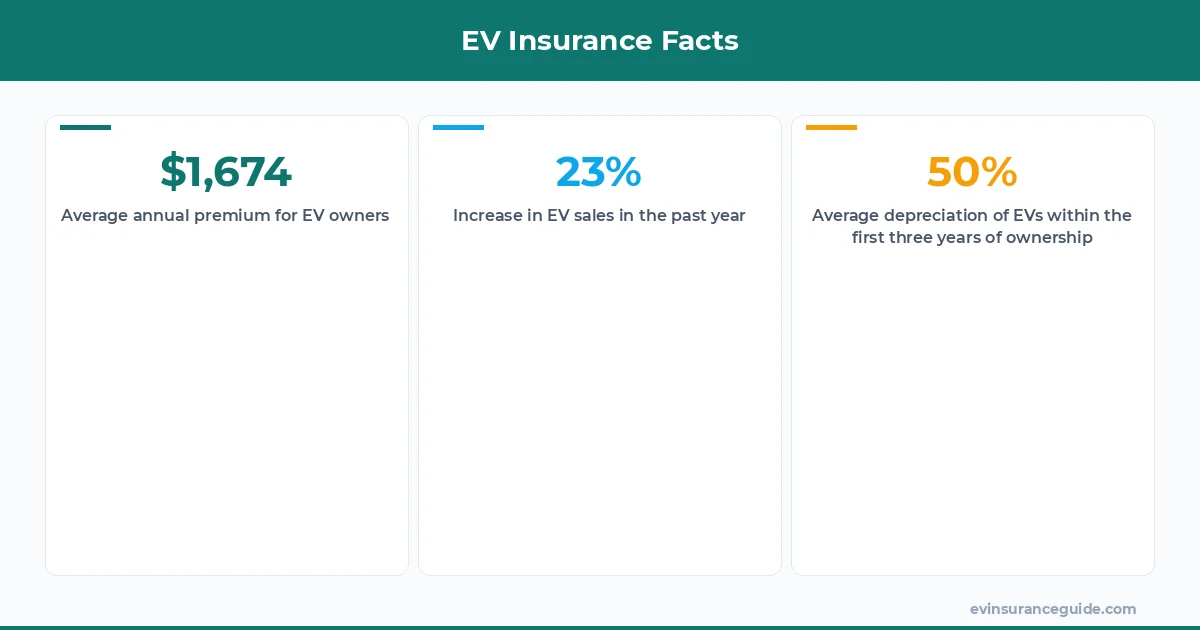

According to a study by Kelley Blue Book, the average EV loses around 50% of its value within the first three years of ownership. Ouch, right? That's why having the right add-ons can help mitigate this risk. For example, a friend of mine, who owns a Tesla Model S, added a comprehensive coverage package to her policy, which included glass repair and replacement. When she accidentally cracked her windshield, she was able to get it replaced for just her deductible, which was $500.

Can You Afford to Skip Certain EV Insurance Add-Ons?

So, which add-ons can you skip? Well, if you're driving an EV with advanced safety features, like lane departure warning or blind spot detection, you might not need to add additional safety features to your policy. For instance, a study by the Insurance Institute for Highway Safety found that EVs with these features tend to have lower accident rates. On the other hand, if you're driving an older EV or one with limited safety features, you might want to consider adding these features to your policy. It's all about weighing the risks and benefits.

But, let's be real - insurance companies often try to upsell you on unnecessary features. That's why it's essential to carefully review your policy and determine what you really need. For example, if you're leasing an EV, you might not need to add maintenance coverage, as your lease agreement might already include this benefit. And, if you're driving an EV with a good safety record, you might not need to add additional collision coverage. It's all about understanding your risks and making informed decisions.

Honestly, Some EV Insurance Add-Ons Are a Waste of Money

Honestly, some add-ons are just not worth the cost. For instance, if you're driving an EV with a low value, like a used Nissan Leaf, you might not need to add comprehensive coverage. The cost of this coverage might outweigh the potential benefits, especially if you have a high deductible. On the other hand, if you're driving a luxury EV, like a Tesla or BMW, you might want to consider adding this coverage to protect your investment.

According to a study by the National Association of Insurance Commissioners, the average cost of comprehensive coverage for an EV is around $200 per year. However, if you have a low-value EV, this cost might not be justified. It's all about doing the math and making informed decisions. For example, if you're driving a used EV with a value of $10,000 or less, you might not need to add comprehensive coverage. But, if you're driving a luxury EV with a value of $50,000 or more, this coverage might be essential.

FAQs

#### What is the average cost of EV insurance?

The average cost of EV insurance varies depending on several factors, including the type of EV, driving history, and location. However, according to a study by the National Association of Insurance Commissioners, the average annual premium for an EV is around $1,500.

#### Do I need to add roadside assistance to my EV insurance policy?

It depends on your specific needs and circumstances. If you drive an EV with limited charging infrastructure, roadside assistance might be a good idea. However, if you have a reliable EV with advanced safety features, you might not need this coverage.

#### Can I customize my EV insurance policy to fit my needs?

Yes, most insurance companies offer customizable policies that allow you to add or remove features as needed. It's essential to carefully review your policy and determine what you really need.

#### How does EV lease vs buy insurance affect my add-on options?

When you lease an EV, your insurance needs will differ from those of an owner. For instance, lease agreements often require specific coverage types, such as gap insurance. On the other hand, owners have more flexibility in choosing their add-ons.

#### What is the difference between comprehensive and collision coverage?

Comprehensive coverage protects against damage to your EV that's not related to an accident, such as theft, vandalism, or natural disasters. Collision coverage, on the other hand, protects against damage to your EV in the event of an accident.

#### Do I need to add umbrella insurance to my EV insurance policy?

It depends on your specific needs and circumstances. If you have significant assets to protect, umbrella insurance might be a good idea. This type of insurance provides additional liability coverage beyond what's included in your standard policy.

#### How can I save money on my EV insurance policy?

There are several ways to save money on your EV insurance policy, including shopping around for quotes, bundling policies, and taking advantage of discounts. For example, some insurance companies offer discounts for EV owners who drive a certain number of miles per year.

Drive safe out there.

— Alex