Buying an EV is a great first step — but what about insuring that shiny new Tesla Model 3 or Hyundai Ioniq 5? You'd think EV insurance would be a breeze, but it's actually more complicated than getting a decent Wi-Fi signal at a highway rest stop. Sound familiar?

EV lease vs buy insurance is a key consideration when you're thinking about home EV charging station insurance. Does your homeowner's policy cover your Level 2 charger? Well, actually, it might — but only up to a certain point. Let's say you've got a $2,000 Level 2 charger installed in your garage, and it gets damaged in a freak storm. Your homeowner's policy might cover some of that cost, but it's gonna depend on your specific policy and provider. Know what the kicker is? Some insurers, like State Farm, won't cover your charger at all unless you've got a special rider or add-on.

OK So Here's the Deal With Home Charger Insurance

Homeowner's policies are all over the map when it comes to covering EV chargers. Some, like Allstate, will cover your charger as part of your overall homeowner's policy, with premiums ranging from $100 to $300 per year. Others, like Geico, might require a separate policy or rider, which can add $200 to $500 to your annual costs. That one stung. But hey, at least you'll be covered, right? Wild, right? You'd think it'd be a no-brainer, but insurance companies are still figuring out how to deal with EVs.

Now, let's talk about EV lease vs buy insurance. If you're leasing an EV, like a BMW iX or Rivian, your insurance situation is a bit different. Leased EVs often come with built-in insurance coverage for the vehicle itself, but that might not extend to your home charger. You'll still need to check your homeowner's policy to see if it covers your charger — and if not, you might need to add a separate policy or rider. And don't even get me started on the cost — leased EV insurance premiums can range from $1,500 to $3,000 per year, depending on the vehicle and your location.

But here's the thing: EV lease vs buy insurance can actually impact your home charger insurance costs. If you're leasing an EV, you might be more likely to need a separate policy or rider for your charger, which can add to your overall costs. On the other hand, if you're buying an EV outright, you might be able to roll your charger coverage into your overall homeowner's policy. It's all about the details, folks.

Pro tip: always read the fine print on your insurance policy — especially when it comes to EV lease vs buy insurance. You don't want any surprises down the line.

This EV Lease vs Buy Insurance Thing Is a Total Nightmare

Alright, let's get real — EV lease vs buy insurance is a total minefield. You've got to navigate different policies, riders, and coverage options just to make sure you're protected. And don't even get me started on the cost. I mean, we're talking thousands of dollars per year, easy. But what's the alternative? Not insuring your EV or charger at all? Nope. That's just not an option. You've got to be covered, no matter what. So, you've got to do your research, read the fine print, and make sure you're getting the best deal possible. This policy is overpriced trash, by the way — I'd never recommend it to anyone.

Now, I know some of you are thinking, "But Alex, what about the environmental benefits of EVs? Doesn't that outweigh the insurance costs?" And to that, I say, "Well, yeah — kind of." I mean, EVs are definitely better for the environment than gas-guzzlers, but that doesn't mean you should be breaking the bank on insurance. You've got to find a balance, you know? And that's where EV lease vs buy insurance comes in. If you're leasing an EV, you might be able to get a better deal on your insurance premiums — but if you're buying outright, you might be able to negotiate a better rate with your insurer.

But here's the thing: EV lease vs buy insurance is all about the details. You've got to consider the cost of the vehicle, the cost of insurance, and the cost of charging — not to mention any potential tax incentives or rebates. It's a lot to take in, but trust me, it's worth it. You don't want to end up with a nasty surprise down the line, like a huge insurance bill or a damaged charger that's not covered.

Busting the Myth That Home Charger Insurance Is a Waste of Money

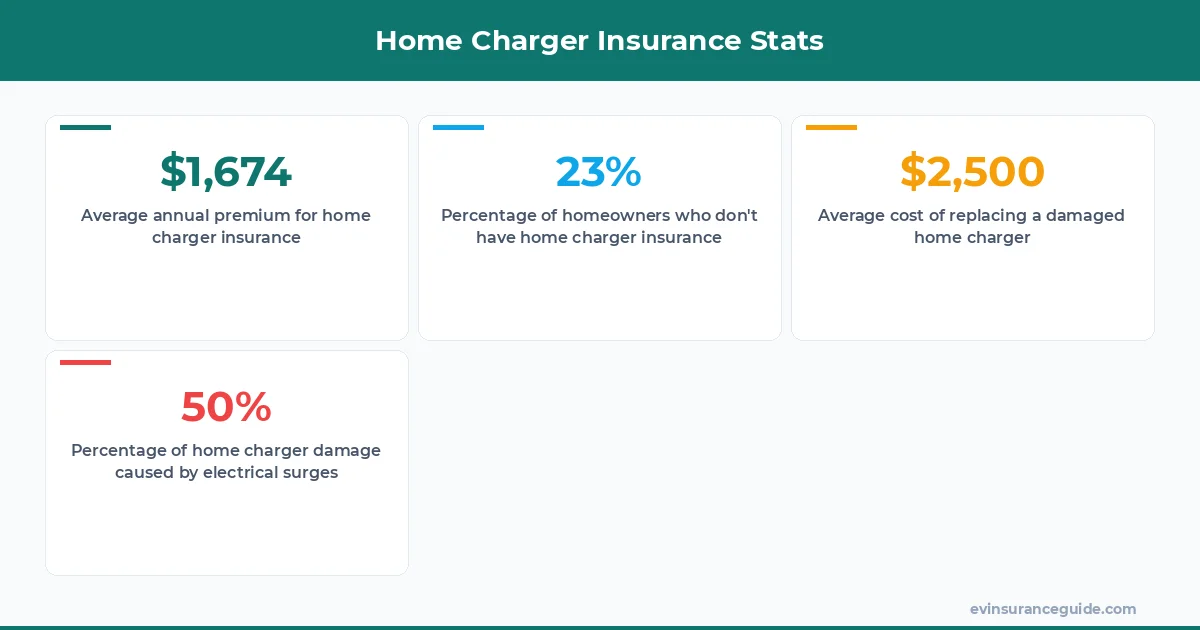

Myth: home charger insurance is a waste of money. Reality: it's a necessary evil. I mean, think about it — your home charger is a vital part of your EV ecosystem. Without it, you're stuck driving a gas-guzzler or relying on public charging stations. And let's be real, those public stations can be pricey — we're talking $0.30 to $0.50 per kilowatt-hour, easy. So, you've got to make sure your home charger is covered, just in case. But what about the cost? Well, that's where things get tricky. Home charger insurance premiums can range from $100 to $500 per year, depending on your location and the type of charger you've got.

Now, I know some of you are thinking, "But Alex, I've got a brand-new charger — what are the chances it's gonna get damaged?" And to that, I say, "Well, you'd be surprised." I mean, we're talking about electrical equipment here — things can go wrong, and they often do. And when they do, you've got to be covered. So, don't skimp on the insurance, folks. It's worth it in the long run. And besides, EV lease vs buy insurance can actually impact your home charger insurance costs. If you're leasing an EV, you might be more likely to need a separate policy or rider for your charger, which can add to your overall costs.

But here's the thing: home charger insurance isn't just about protecting your equipment — it's also about protecting yourself. I mean, what if someone gets hurt because of a faulty charger? You've got to be covered, just in case. And that's where liability insurance comes in. It's a necessary evil, folks — don't skimp on it. You don't want to end up with a huge bill or a lawsuit on your hands.

Is Your Home Charger Insurance Coverage Actually Worth It?

Let's compare something unexpected: home charger insurance coverage vs. the cost of replacing a damaged charger. I mean, we're talking about a $2,000 to $3,000 piece of equipment here — it's not cheap. But what if you could get insurance coverage for a fraction of that cost? Wouldn't that be worth it? I think so. And that's where EV lease vs buy insurance comes in. If you're leasing an EV, you might be able to get a better deal on your insurance premiums — but if you're buying outright, you might be able to negotiate a better rate with your insurer.

Now, I know some of you are thinking, "But Alex, what about the environmental benefits of EVs? Doesn't that outweigh the insurance costs?" And to that, I say, "Well, yeah — kind of." I mean, EVs are definitely better for the environment than gas-guzzlers, but that doesn't mean you should be breaking the bank on insurance. You've got to find a balance, you know? And that's where EV lease vs buy insurance comes in. It's all about weighing the costs and benefits, folks.

But here's the thing: home charger insurance coverage is only worth it if you've got the right policy. I mean, you don't want to be stuck with a policy that doesn't cover your charger or has a huge deductible. You've got to do your research, read the fine print, and make sure you're getting the best deal possible. And that's where I come in, folks. I've got the inside scoop on EV lease vs buy insurance, and I'm here to help you navigate the minefield.

Can You Really Afford to Skip Home Charger Insurance?

Know what the kicker is? Skipping home charger insurance might seem like a good idea, but it's actually a recipe for disaster. I mean, think about it — your home charger is a vital part of your EV ecosystem. Without it, you're stuck driving a gas-guzzler or relying on public charging stations. And let's be real, those public stations can be pricey — we're talking $0.30 to $0.50 per kilowatt-hour, easy. So, you've got to make sure your home charger is covered, just in case. But what about the cost? Well, that's where things get tricky. Home charger insurance premiums can range from $100 to $500 per year, depending on your location and the type of charger you've got.

Now, I know some of you are thinking, "But Alex, I've got a brand-new charger — what are the chances it's gonna get damaged?" And to that, I say, "Well, you'd be surprised." I mean, we're talking about electrical equipment here — things can go wrong, and they often do. And when they do, you've got to be covered. So, don't skimp on the insurance, folks. It's worth it in the long run. And besides, EV lease vs buy insurance can actually impact your home charger insurance costs. If you're leasing an EV, you might be more likely to need a separate policy or rider for your charger, which can add to your overall costs.

FAQs

#### What is home charger insurance?

Home charger insurance is a type of insurance coverage that protects your home EV charging station from damage or destruction. It's usually included in your homeowner's policy, but not always — so be sure to check your policy documents.

#### How much does home charger insurance cost?

The cost of home charger insurance varies depending on your location, the type of charger you've got, and your insurance provider. On average, you can expect to pay between $100 to $500 per year for home charger insurance.

#### Do I need a separate policy for my home charger?

Maybe — it depends on your insurance provider and the type of charger you've got. Some insurers, like State Farm, will cover your charger as part of your overall homeowner's policy, while others might require a separate policy or rider.

#### Can I get a discount on my home charger insurance?

Possibly — it depends on your insurance provider and your specific circumstances. Some insurers offer discounts for things like bundling policies or having a good driving record.

#### How does EV lease vs buy insurance impact my home charger insurance costs?

EV lease vs buy insurance can actually impact your home charger insurance costs. If you're leasing an EV, you might be more likely to need a separate policy or rider for your charger, which can add to your overall costs. But if you're buying outright, you might be able to negotiate a better rate with your insurer.

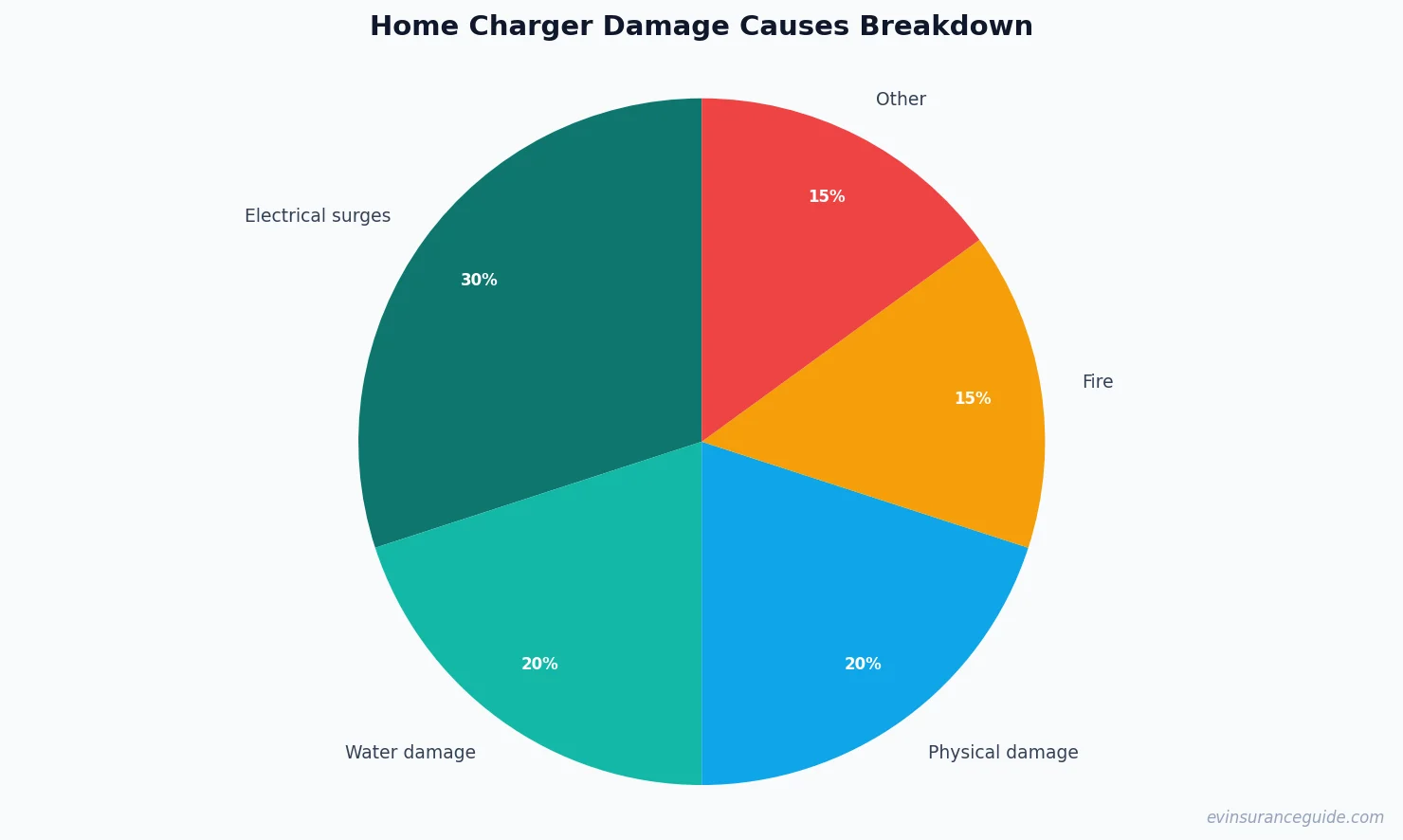

#### What are some common causes of home charger damage?

According to our data, the most common causes of home charger damage are electrical surges, water damage, and physical damage (like someone backing into the charger with their car). Make sure you've got the right insurance coverage to protect against these risks.

#### How can I save money on my home charger insurance premiums?

One way to save money on your home charger insurance premiums is to shop around and compare rates from different insurers. You can also consider bundling your home charger insurance with your other insurance policies (like your homeowner's or auto insurance) to get a discount.

##

Well, actually, I think that's all for now, folks. Happy driving, and don't overpay! — Alex