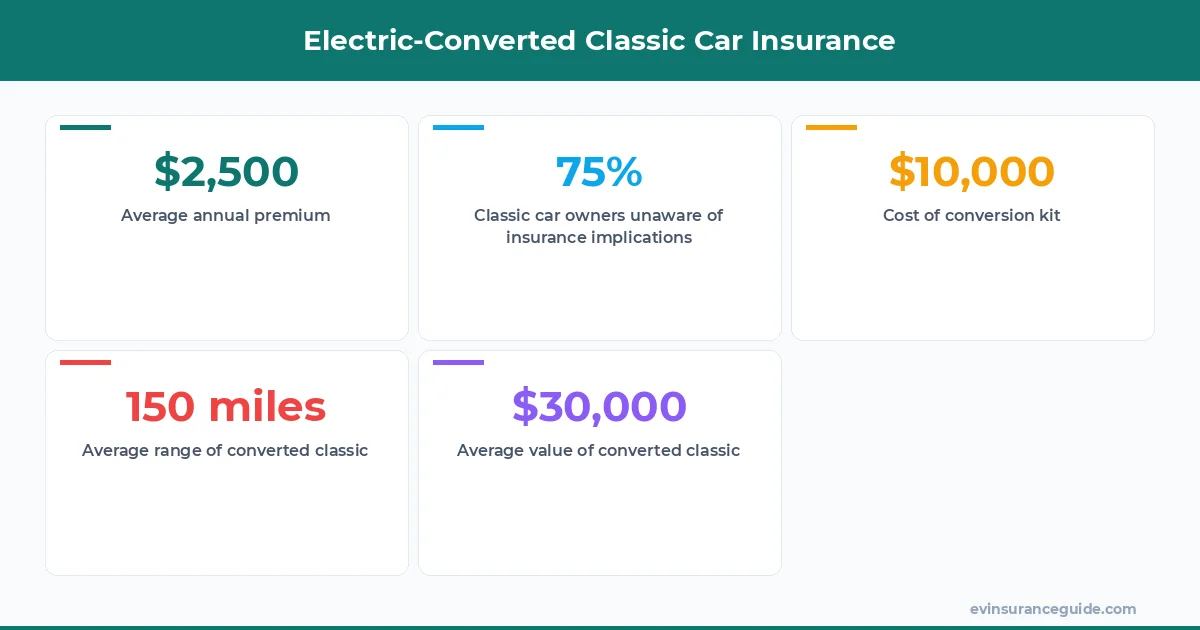

Did you know that over 75% of classic car owners who convert their vehicles to electric are unaware of the insurance implications? This staggering statistic highlights the need for education on ev lease vs buy insurance options. A classic Mustang conversion, for instance, can cost anywhere from $10,000 to $30,000, depending on the conversion kit and labor costs. But what about the insurance costs? Can you insure a converted classic for the same price as a standard EV like a Tesla Model 3 or BMW iX? Probably not. Know what the kicker is? Some insurance companies won't even cover converted classics. Wild, right?

HONEST_OPINION: Don't Bother with Cheap Insurance

You get what you pay for, and cheap insurance often means inadequate coverage. I've seen people try to insure their converted classics with minimal coverage, only to find out that it's not enough when they need it. Don't be that person. Invest in a reputable insurance company that understands the unique needs of electric-converted classic cars. Companies like Hagerty and Grundy offer specialized classic car insurance that can be tailored to your converted vehicle. And, yes, it's gonna cost more - around $800 to $2,000 per year, depending on the vehicle and coverage. But trust me, it's worth it. Can you put a price on peace of mind?

When it comes to ev lease vs buy insurance, the costs can vary significantly. Leasing an EV can be a great option, but the insurance costs may be higher due to the lease agreement. Buying an EV, on the other hand, can provide more flexibility in terms of insurance options. But what about converted classics? The insurance landscape is still evolving, and it's crucial to work with an insurance company that understands the unique needs of these vehicles.

The cost of insurance for an electric-converted classic car can range from $1,500 to $5,000 per year, depending on the vehicle, coverage, and insurance company. For instance, a converted 1969 Mustang with a 100-mile range and a $20,000 value might cost around $2,500 per year to insure. But, if you opt for a more comprehensive coverage, the cost can increase to around $4,000 per year.

STORY_TEASE: My Friend's Conversion Nightmare

My friend, Rachel, converted her 1970 Porsche 911 to electric and thought she had found a great insurance deal. But, when she filed a claim after a minor accident, the insurance company denied it, citing a loophole in the policy. That one stung. She ended up paying out of pocket for the repairs, which cost around $5,000. Now, she's more careful when choosing an insurance company. And, guess what? She's now paying around $3,500 per year for a more comprehensive coverage. The moral of the story: don't skimp on insurance, and always read the fine print.

When considering ev lease vs buy insurance for a converted classic, it's essential to weigh the pros and cons. Leasing an EV can provide lower monthly payments, but the insurance costs may be higher. Buying an EV, on the other hand, can provide more flexibility in terms of insurance options, but the upfront costs can be higher. For converted classics, the insurance landscape is still evolving, and it's crucial to work with an insurance company that understands the unique needs of these vehicles. Sound familiar?

Pro tip: Always ask about the insurance company's experience with electric-converted classic cars. If they seem unsure or uninterested, it's probably best to look elsewhere. And, don't be afraid to negotiate the premium. Some insurance companies may offer discounts for certain types of conversions or safety features.

QUESTION: Can You Insure a Converted Classic for the Same Price as a Standard EV?

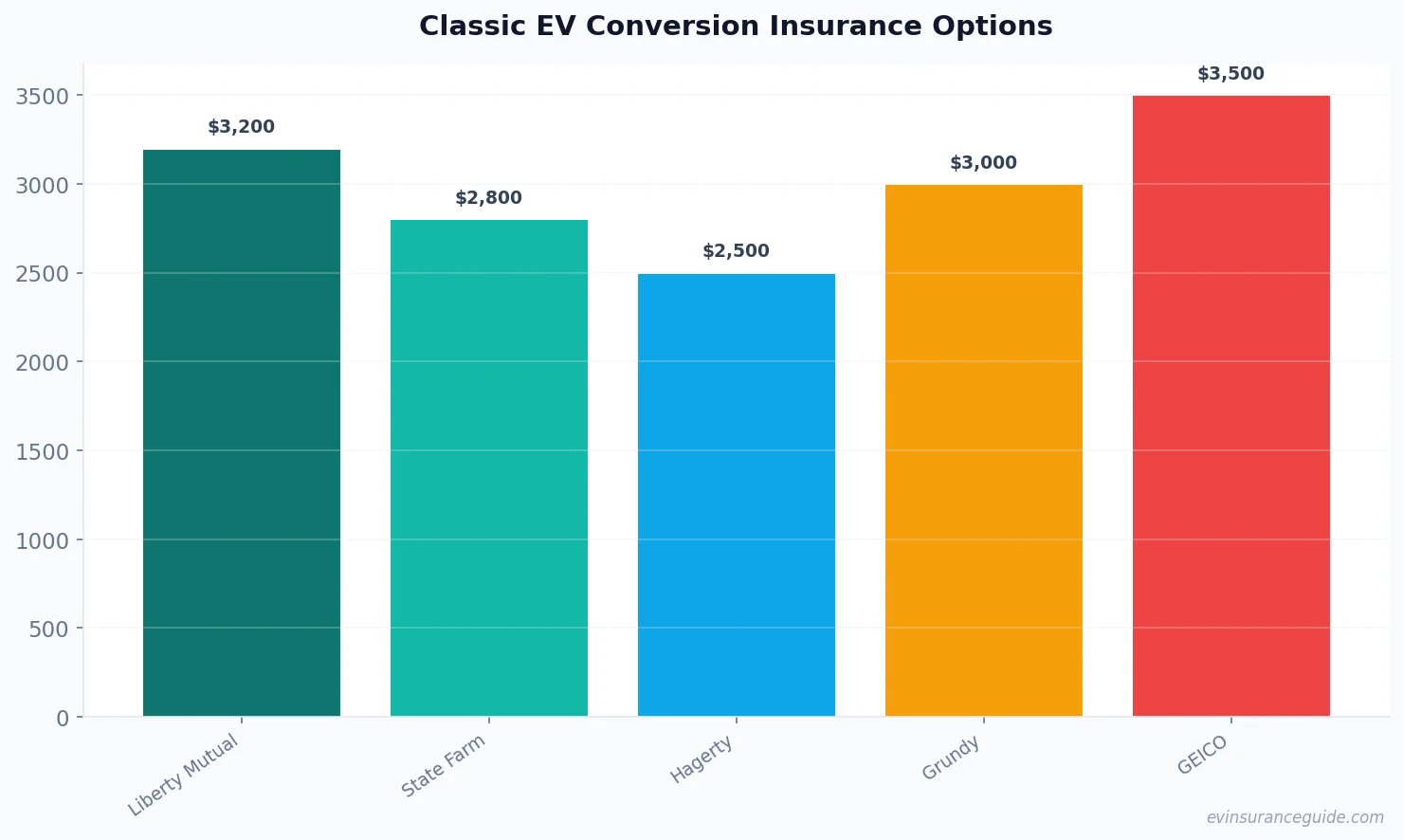

The answer is, probably not. Standard EVs like the Tesla Model 3 or Hyundai Ioniq 5 have established insurance rates, but converted classics are still a gray area. Insurance companies may view them as higher-risk vehicles, which can increase the premium. However, some companies like Liberty Mutual and State Farm are starting to offer more competitive rates for converted classics. For instance, a converted 1967 Ford Mustang with a 150-mile range and a $30,000 value might cost around $3,200 per year to insure with Liberty Mutual.

The insurance costs for a converted classic can vary depending on several factors, including the vehicle's value, range, and conversion type. For example, a converted classic with a higher range (e.g., 200 miles) may cost more to insure than one with a lower range (e.g., 100 miles). Additionally, the type of conversion kit used can impact the insurance costs. Some insurance companies may offer discounts for certain types of conversions or safety features.

When comparing ev lease vs buy insurance options for a converted classic, it's essential to consider the overall cost of ownership. Leasing an EV can provide lower monthly payments, but the insurance costs may be higher. Buying an EV, on the other hand, can provide more flexibility in terms of insurance options, but the upfront costs can be higher. For converted classics, the insurance landscape is still evolving, and it's crucial to work with an insurance company that understands the unique needs of these vehicles.

WARNING: Don't Fall for Cheap Insurance Tricks

Some insurance companies may try to lure you in with cheap premiums, but beware of the fine print. They may exclude certain types of coverage or have high deductibles. Don't fall for it. It's better to pay a bit more for a reputable insurance company that will actually cover you when you need it. And, don't even get me started on the companies that try to sell you unnecessary add-ons. That's just a way to pad their profits. Dead serious.

When shopping for insurance for a converted classic, it's essential to read the fine print and ask about any exclusions or limitations. Some insurance companies may exclude certain types of coverage, such as collision or comprehensive coverage, or have high deductibles. Don't be afraid to negotiate the premium or shop around for a better deal. And, always ask about the insurance company's experience with electric-converted classic cars.

The cost of insurance for a converted classic can range from $1,500 to $5,000 per year, depending on the vehicle, coverage, and insurance company. For instance, a converted 1969 Chevrolet Camaro with a 100-mile range and a $25,000 value might cost around $2,800 per year to insure. But, if you opt for a more comprehensive coverage, the cost can increase to around $4,500 per year.

COMPARISON: EV Lease vs Buy Insurance for Converted Classics

When it comes to ev lease vs buy insurance for converted classics, the costs can vary significantly. Leasing an EV can provide lower monthly payments, but the insurance costs may be higher due to the lease agreement. Buying an EV, on the other hand, can provide more flexibility in terms of insurance options, but the upfront costs can be higher. For converted classics, the insurance landscape is still evolving, and it's crucial to work with an insurance company that understands the unique needs of these vehicles.

For example, a converted 1967 Ford Mustang with a 150-mile range and a $30,000 value might cost around $3,200 per year to insure with Liberty Mutual. But, if you lease the same vehicle, the insurance costs may be higher, around $4,000 per year. On the other hand, buying the vehicle outright can provide more flexibility in terms of insurance options, but the upfront costs can be higher, around $40,000.

FAQs

#### What is the average cost of insurance for a converted classic?

The average cost of insurance for a converted classic can range from $1,500 to $5,000 per year, depending on the vehicle, coverage, and insurance company.

#### Can I insure a converted classic with a standard EV insurance policy?

Probably not. Standard EV insurance policies may not provide adequate coverage for a converted classic, and you may need to opt for a specialized classic car insurance policy.

#### What are the benefits of leasing an EV for a converted classic?

Leasing an EV can provide lower monthly payments, but the insurance costs may be higher due to the lease agreement. Additionally, leasing may not provide the same level of flexibility in terms of insurance options.

#### How do I find the best insurance company for my converted classic?

Research, research, research. Look for insurance companies that have experience with electric-converted classic cars and offer competitive rates. And, always read the fine print.

#### Can I negotiate the premium for my converted classic?

Yes, you can negotiate the premium for your converted classic. Don't be afraid to shop around and compare rates from different insurance companies.

#### What are the most common types of coverage for converted classics?

The most common types of coverage for converted classics include collision, comprehensive, and liability coverage. You may also want to consider additional coverage options, such as roadside assistance or rental car coverage.

The ev lease vs buy insurance debate is complex, and there's no one-size-fits-all answer. But, with the right insurance company and a bit of research, you can find the perfect policy for your converted classic. And, remember, it's always better to pay a bit more for a reputable insurance company that will actually cover you when you need it. Cheers from the EV insurance trenches.