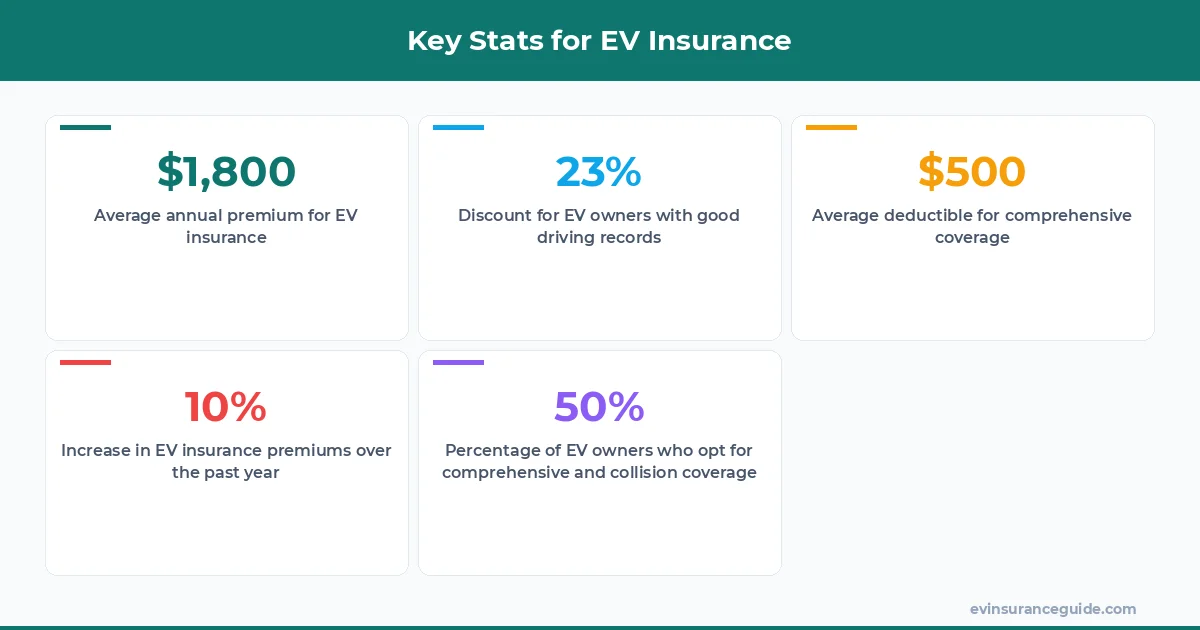

Meet Jane, a proud owner of a Tesla Model 3. Before switching to her current insurance policy, she was paying around $2,500 per year for a policy that barely covered her vehicle. She had a $1,000 deductible for comprehensive coverage and a $500 deductible for collision coverage. But after doing some research and reading reviews from other EV owners, she decided to switch to a new insurer that offered a more comprehensive policy with lower deductibles. Now, she's paying around $1,800 per year for a policy that includes $0 deductible for comprehensive coverage and $200 deductible for collision coverage. That's a savings of $700 per year, which is a significant amount for anyone. Sound familiar?

MYTH_BUST — Comprehensive Coverage is Not Just for Accidents

One of the biggest myths surrounding comprehensive coverage is that it's only necessary for accidents. But that's not true. Comprehensive coverage can help protect your vehicle from a variety of non-accident related damages, such as theft, vandalism, and natural disasters. For example, if you live in an area prone to hurricanes, comprehensive coverage can help you replace your vehicle if it's damaged or destroyed by a storm. And, if you're leasing an EV, you'll likely need to have comprehensive coverage as part of your lease agreement. Know what the kicker is? Some insurers, like Geico, offer comprehensive coverage with a deductible as low as $100. That's a great deal, especially when you consider that the average cost of comprehensive coverage for an EV is around $300 per year.

But, what about collision coverage? Do you really need it? Well, actually, collision coverage is a must-have for any vehicle owner, regardless of whether you're leasing or buying. It helps cover the cost of repairs or replacement if your vehicle is damaged in an accident. And, if you're financing your EV, your lender will likely require you to have collision coverage. For example, if you're financing a BMW iX, your lender may require you to have a collision coverage policy with a deductible of $500 or less. That way, if you're involved in an accident, you can get your vehicle repaired or replaced without having to pay out of pocket.

QUESTION — Do You Need Both Comprehensive and Collision Coverage for Your EV?

So, do you need both comprehensive and collision coverage for your EV? The answer is, it depends. If you're leasing an EV, you'll likely need to have both comprehensive and collision coverage as part of your lease agreement. But, if you're buying an EV outright, you may not need both. For example, if you're buying a used Hyundai Ioniq 5, you may be able to get away with just comprehensive coverage, especially if you're not financing the vehicle. On the other hand, if you're buying a brand new Rivian, you may want to consider getting both comprehensive and collision coverage, especially if you're financing the vehicle. Wild, right?

But, here's the thing: even if you're not required to have both comprehensive and collision coverage, it's still a good idea to get them. That's because, without them, you could be left with a significant financial burden if your vehicle is damaged or stolen. For example, if your Tesla Model Y is stolen and you don't have comprehensive coverage, you could be left with a bill of $50,000 or more to replace the vehicle. And, if you're involved in an accident and don't have collision coverage, you could be left with a bill of $10,000 or more to repair or replace your vehicle. Nope, that's not a risk worth taking.

Pro tip: When shopping for insurance, make sure to read the fine print and understand what's covered and what's not. It's also a good idea to get quotes from multiple insurers to compare prices and coverage options.

WARNING — Don't Get Caught Off Guard by Hidden Costs

One thing to watch out for when shopping for insurance is hidden costs. Some insurers may offer low premiums, but then hit you with high deductibles or other fees. For example, some insurers may charge a fee of $200 or more per year for roadside assistance, even if you don't use it. And, some insurers may charge a fee of $100 or more per year for glass repair, even if you don't need it. That one stung. So, make sure to read the fine print and understand what you're getting into before signing up for a policy.

But, what about the cost of insurance for EVs? Is it really that much more expensive than insurance for gas-powered vehicles? The answer is, it depends. Some insurers, like Progressive, offer discounts for EV owners, which can help lower the cost of insurance. For example, if you own a Tesla Model 3, you may be eligible for a discount of $200 or more per year on your insurance premium. And, some insurers, like State Farm, offer specialized EV insurance policies that can help lower the cost of insurance. For example, if you own a BMW iX, you may be eligible for a specialized EV insurance policy that includes features like roadside assistance and glass repair.

OK So Here's the Deal With EV Lease vs Buy Insurance

So, what's the deal with ev lease vs buy insurance? Well, it's pretty simple. If you're leasing an EV, you'll likely need to have comprehensive and collision coverage as part of your lease agreement. But, if you're buying an EV outright, you may not need both. For example, if you're buying a used Hyundai Ioniq 5, you may be able to get away with just comprehensive coverage, especially if you're not financing the vehicle. On the other hand, if you're buying a brand new Rivian, you may want to consider getting both comprehensive and collision coverage, especially if you're financing the vehicle.

But, here's the thing: even if you're not required to have both comprehensive and collision coverage, it's still a good idea to get them. That's because, without them, you could be left with a significant financial burden if your vehicle is damaged or stolen. For example, if your Tesla Model Y is stolen and you don't have comprehensive coverage, you could be left with a bill of $50,000 or more to replace the vehicle. And, if you're involved in an accident and don't have collision coverage, you could be left with a bill of $10,000 or more to repair or replace your vehicle. Dead serious.

HONEST_OPINION — Some Insurance Policies are Overpriced Trash

Some insurance policies are overpriced trash, plain and simple. For example, some insurers may charge $3,000 or more per year for a policy that barely covers your vehicle. That's not a good deal, especially when you consider that the average cost of insurance for an EV is around $2,000 per year. But, on the other hand, some insurers offer great deals on insurance policies. For example, some insurers may offer a policy with comprehensive coverage, collision coverage, and roadside assistance for $1,500 or less per year. That's a great deal, especially when you consider that the average cost of insurance for an EV is around $2,000 per year.

FAQs

#### What is comprehensive coverage?

Comprehensive coverage helps protect your vehicle from non-accident related damages, such as theft, vandalism, and natural disasters. For example, if you live in an area prone to hurricanes, comprehensive coverage can help you replace your vehicle if it's damaged or destroyed by a storm.

#### What is collision coverage?

Collision coverage helps cover the cost of repairs or replacement if your vehicle is damaged in an accident. For example, if you're involved in an accident and your vehicle is damaged, collision coverage can help you pay for the repairs or replacement of your vehicle.

#### Do I need both comprehensive and collision coverage for my EV?

It depends. If you're leasing an EV, you'll likely need to have both comprehensive and collision coverage as part of your lease agreement. But, if you're buying an EV outright, you may not need both. For example, if you're buying a used Hyundai Ioniq 5, you may be able to get away with just comprehensive coverage, especially if you're not financing the vehicle.

#### How much does insurance for an EV cost?

The cost of insurance for an EV can vary depending on a variety of factors, such as the type of vehicle, your location, and your driving record. On average, the cost of insurance for an EV is around $2,000 per year. However, some insurers may charge more or less, depending on the specifics of your policy.

#### Can I get a discount on my insurance premium?

Yes, some insurers offer discounts for EV owners, which can help lower the cost of insurance. For example, if you own a Tesla Model 3, you may be eligible for a discount of $200 or more per year on your insurance premium.

#### What is the difference between ev lease vs buy insurance?

The main difference between ev lease vs buy insurance is that leasing an EV typically requires you to have comprehensive and collision coverage as part of your lease agreement. On the other hand, buying an EV outright may not require you to have both comprehensive and collision coverage.

Well, actually, let me rethink that. The difference between ev lease vs buy insurance is more complex than that. When you lease an EV, you're essentially renting the vehicle for a set period of time, usually 2-3 years. During that time, you'll need to have comprehensive and collision coverage to protect the vehicle from damage or loss. But, when you buy an EV outright, you own the vehicle and can choose whether or not to have comprehensive and collision coverage. It's a big decision, and one that requires careful consideration.

Cheers from the EV insurance trenches.