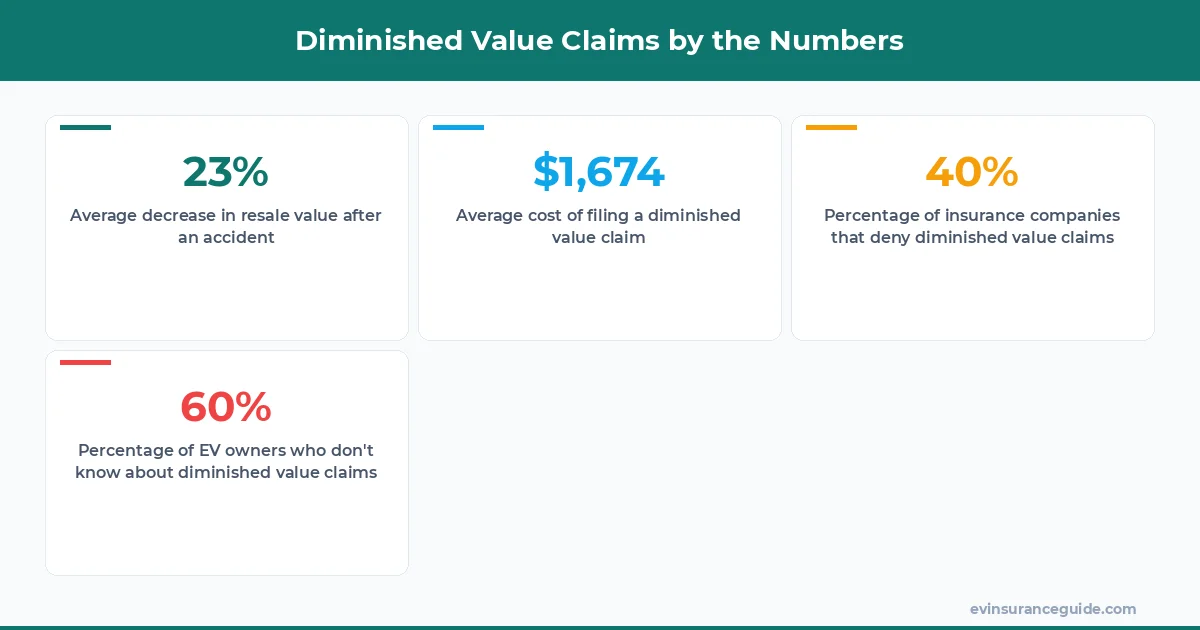

Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. He'd been in a fender bender, and now his insurance company was treating his car like it was damaged goods. Sound familiar? That's because diminished value claims are a real pain point for EV owners. Know what the kicker is? Most people don't even know they can file a claim for the lost resale value of their car. Wild, right?

Comparing Apples and oranges: EVs vs Gas Guzzlers

When it comes to diminished value claims, EVs are in a whole different ball game compared to their gas-guzzling counterparts. For one, EVs tend to hold their value better, but that also means that any loss in resale value can be more significant. Take the Tesla Model 3, for example. It's one of the most popular EVs on the market, and its resale value is incredibly high. But if you get into an accident, that value can drop like a stone. And what about the BMW iX? That's a $100,000+ car we're talking about. You don't want to lose out on tens of thousands of dollars just because your insurance company doesn't want to play ball. That one stung.

But here's the thing: insurance companies don't always make it easy to file a diminished value claim. They might try to lowball you, or worse, deny your claim outright. That's why it's essential to know your rights and understand the process. For instance, did you know that some states have laws that require insurance companies to pay out diminished value claims? Yeah, it's a thing. And it's not just limited to EVs, either. Any car can be eligible, as long as it's been in an accident.

And let's not forget about the pros and cons of EV lease vs buy insurance. If you lease your EV, you might not be eligible for a diminished value claim, since you don't actually own the car. But if you buy, you're on the hook for the full value of the car, which can be a significant financial burden. So, what's the best option? Well, actually, it depends on your specific situation. If you're planning to keep your EV for a long time, buying might be the way to go. But if you want flexibility and don't want to worry about resale value, leasing could be the better choice.

Warning: Don't Get Caught in the Diminished Value Trap

So, you've been in an accident, and you're trying to file a diminished value claim. But wait, your insurance company is telling you that you're not eligible. What gives? Well, it turns out that some insurance companies have a sneaky little clause in their policies that excludes diminished value claims for certain types of accidents. Know what the trap is? It's called the "pre-existing condition" clause, and it can leave you high and dry. For example, let's say you have a Rivian R1T, and you get into a fender bender. If your insurance company can prove that the damage was pre-existing, they might deny your claim. That's why it's crucial to read your policy carefully and understand what's covered and what's not.

And don't even get me started on the cost. Filing a diminished value claim can be expensive, especially if you have to hire a lawyer to fight your case. We're talking thousands of dollars, easy. And what if you lose? You're out of pocket, and you still don't have the compensation you deserve. It's a risk, no doubt about it. But if you're willing to take that risk, the rewards can be significant. I mean, we're talking tens of thousands of dollars in some cases. So, is it worth it? Dead serious, it depends on your situation.

But here's a pro tip:

When filing a diminished value claim, make sure to get an independent appraisal of your car's value before and after the accident. This can help prove that the accident did, in fact, cause a significant loss in resale value. And don't be afraid to negotiate with your insurance company – they might be willing to settle for a lower amount than you think.

What's the Real Cost of Diminished Value Claims?

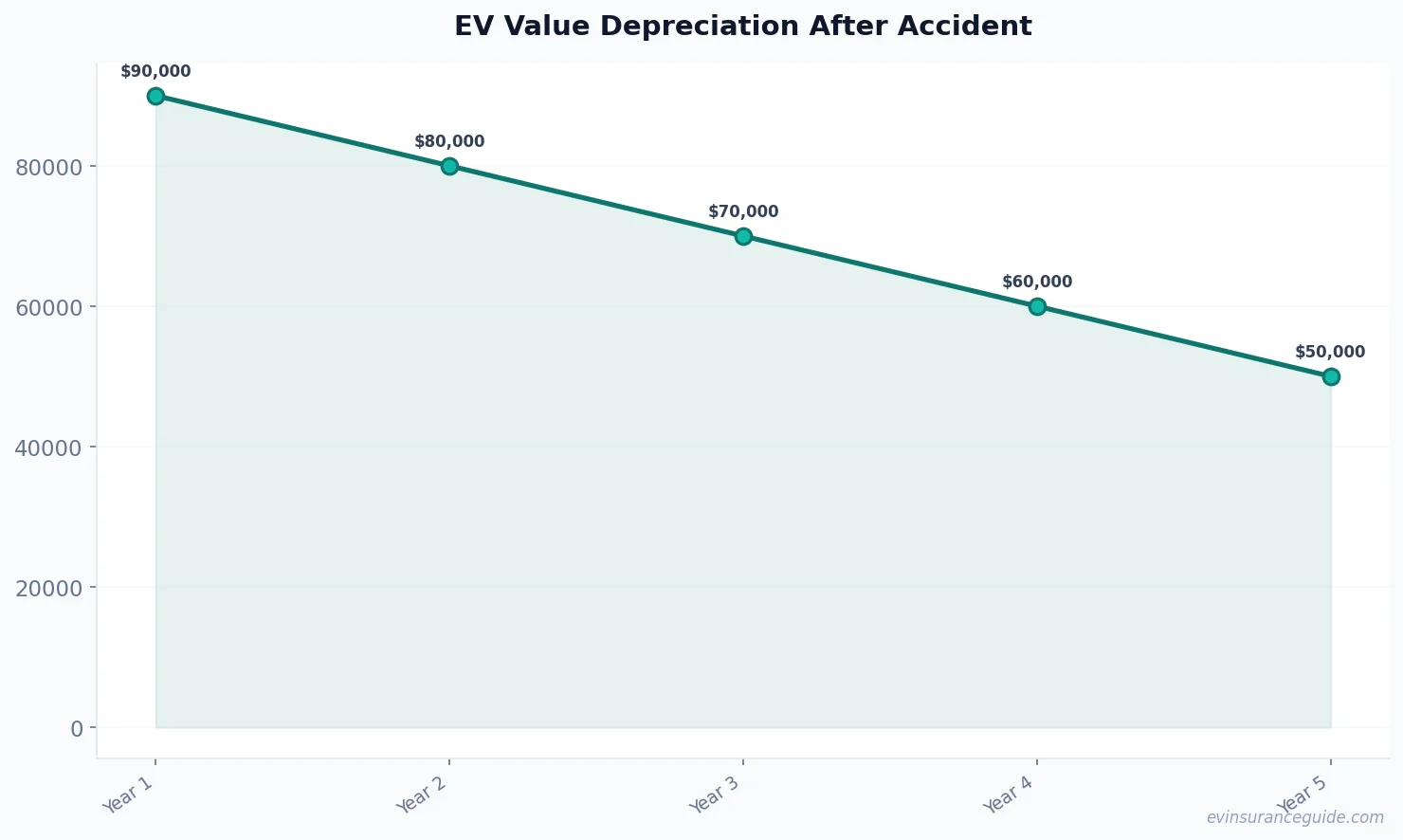

So, you're thinking about filing a diminished value claim, but you're not sure what to expect. Well, let me tell you, it's not always easy. The process can be long and arduous, and the cost can be significant. For instance, did you know that the average cost of filing a diminished value claim is around $2,000 to $5,000? And that's not even including the cost of hiring a lawyer, which can add up quickly. But what's the real cost? Is it worth it to pursue a diminished value claim, or are you better off just eating the loss? Know what the kicker is? It depends on the specific circumstances of your case.

For example, let's say you have a Hyundai Ioniq 5, and you get into a minor accident. The damage is minimal, but the resale value of your car takes a hit. In that case, it might not be worth pursuing a diminished value claim, since the cost of filing the claim could outweigh the potential reward. But if you have a high-end EV like a Tesla Model S, the situation is different. The resale value of that car is incredibly high, so even a minor accident could result in a significant loss of value. In that case, it might be worth pursuing a diminished value claim, even if it's expensive.

And let's not forget about the impact of EV lease vs buy insurance on diminished value claims. If you lease your EV, you might not have to worry about the long-term resale value of the car, since you'll be returning it to the dealer at the end of the lease. But if you buy, you're on the hook for the full value of the car, which can be a significant financial burden. So, what's the best option? Well, it depends on your specific situation. If you're planning to keep your EV for a long time, buying might be the way to go. But if you want flexibility and don't want to worry about resale value, leasing could be the better choice.

Can You Really Get Compensated for Diminished Value?

So, you're wondering if you can really get compensated for the diminished value of your EV. The answer is, it depends. If you have a good insurance policy and a solid case, you might be able to get a significant payout. But if your insurance company is being stubborn, you might be out of luck. Know what the problem is? Insurance companies don't always play by the rules. They might try to lowball you or deny your claim outright. That's why it's essential to have a good lawyer on your side, someone who knows the ins and outs of diminished value claims.

For instance, let's say you have a Tesla Model Y, and you get into an accident. The damage is significant, and the resale value of your car takes a hit. In that case, you might be eligible for a diminished value claim, but your insurance company might try to deny it. That's where a good lawyer comes in – they can help you navigate the process and get the compensation you deserve. And what about the cost? Well, it's not cheap, but it might be worth it in the long run. I mean, we're talking tens of thousands of dollars in some cases. So, is it worth it? Dead serious, it depends on your situation.

But here's the thing: diminished value claims are not just limited to EVs. Any car can be eligible, as long as it's been in an accident. So, what's the best way to protect yourself? Well, it's simple: make sure you have a good insurance policy, and know your rights. Don't be afraid to stand up to your insurance company and fight for what's yours. And if all else fails, consider hiring a lawyer to help you navigate the process.

Busting the Myth: Diminished Value Claims are Only for Totaled Cars

So, you think that diminished value claims are only for cars that have been totaled. Well, think again. The truth is, any car can be eligible for a diminished value claim, as long as it's been in an accident. Know what the myth is? It's that diminished value claims are only for cars that are beyond repair. But that's just not true. Even if your car is still driveable, you might be eligible for a diminished value claim if the accident has affected its resale value.

For example, let's say you have a Rivian R1T, and you get into a minor accident. The damage is minimal, but the resale value of your car takes a hit. In that case, you might be eligible for a diminished value claim, even though your car is still driveable. And what about the cost? Well, it's not cheap, but it might be worth it in the long run. I mean, we're talking tens of thousands of dollars in some cases. So, is it worth it? Dead serious, it depends on your situation.

But here's the thing: insurance companies don't always make it easy to file a diminished value claim. They might try to lowball you or deny your claim outright. That's why it's essential to have a good lawyer on your side, someone who knows the ins and outs of diminished value claims. And don't be afraid to stand up to your insurance company and fight for what's yours. You have the right to pursue a diminished value claim, and you shouldn't let anyone take that away from you.

My Honest Opinion: EV Lease vs Buy Insurance is a No-Brainer

So, you're wondering whether to lease or buy your EV. Well, let me tell you, it's a no-brainer. If you're planning to keep your EV for a long time, buying is the way to go. But if you want flexibility and don't want to worry about resale value, leasing is the better choice. Know what the problem is? Insurance companies don't always make it easy to understand the pros and cons of EV lease vs buy insurance. They might try to confuse you with complex policies and hidden fees. That's why it's essential to do your research and understand the terms of your policy.

For instance, let's say you lease a Tesla Model 3, and you get into an accident. The damage is significant, and the resale value of your car takes a hit. In that case, you might not be eligible for a diminished value claim, since you don't actually own the car. But if you buy, you're on the hook for the full value of the car, which can be a significant financial burden. So, what's the best option? Well, it depends on your specific situation. If you're planning to keep your EV for a long time, buying might be the way to go. But if you want flexibility and don't want to worry about resale value, leasing could be the better choice.

And let's not forget about the impact of EV lease vs buy insurance on diminished value claims. If you lease your EV, you might not have to worry about the long-term resale value of the car, since you'll be returning it to the dealer at the end of the lease. But if you buy, you're on the hook for the full value of the car, which can be a significant financial burden. So, what's the best option? Well, it depends on your specific situation. If you're planning to keep your EV for a long time, buying might be the way to go. But if you want flexibility and don't want to worry about resale value, leasing could be the better choice.

FAQs

#### What is a diminished value claim?

A diminished value claim is a type of insurance claim that compensates you for the lost resale value of your car after an accident. It's not just limited to EVs, either – any car can be eligible, as long as it's been in an accident.

#### How do I file a diminished value claim?

To file a diminished value claim, you'll need to contact your insurance company and provide documentation of the accident and the damage to your car. You may also need to get an independent appraisal of your car's value before and after the accident.

#### Can I file a diminished value claim if I lease my EV?

It depends on the terms of your lease. If you lease your EV, you might not be eligible for a diminished value claim, since you don't actually own the car. But if you buy, you're on the hook for the full value of the car, which can be a significant financial burden.

#### How much does it cost to file a diminished value claim?

The cost of filing a diminished value claim can vary, but it's typically in the range of $2,000 to $5,000. And that's not even including the cost of hiring a lawyer, which can add up quickly.

#### Is it worth pursuing a diminished value claim?

It depends on your situation. If you have a good insurance policy and a solid case, you might be able to get a significant payout. But if your insurance company is being stubborn, you might be out of luck.

#### What's the best way to protect myself from diminished value claims?

The best way to protect yourself is to have a good insurance policy and know your rights. Don't be afraid to stand up to your insurance company and fight for what's yours. And if all else fails, consider hiring a lawyer to help you navigate the process.

And that's a wrap, folks. Keep those batteries topped up and those premiums low. — Alex