Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. He'd just moved to a flood-prone area, and his insurer was factoring in the risk of water damage. Sound familiar? I told him it's not just about the location – it's about understanding what comprehensive insurance actually covers. Dead serious: if you don't know the difference between collision and comprehensive, you're gonna get burned.

Honestly, Flood Damage is a Real Concern

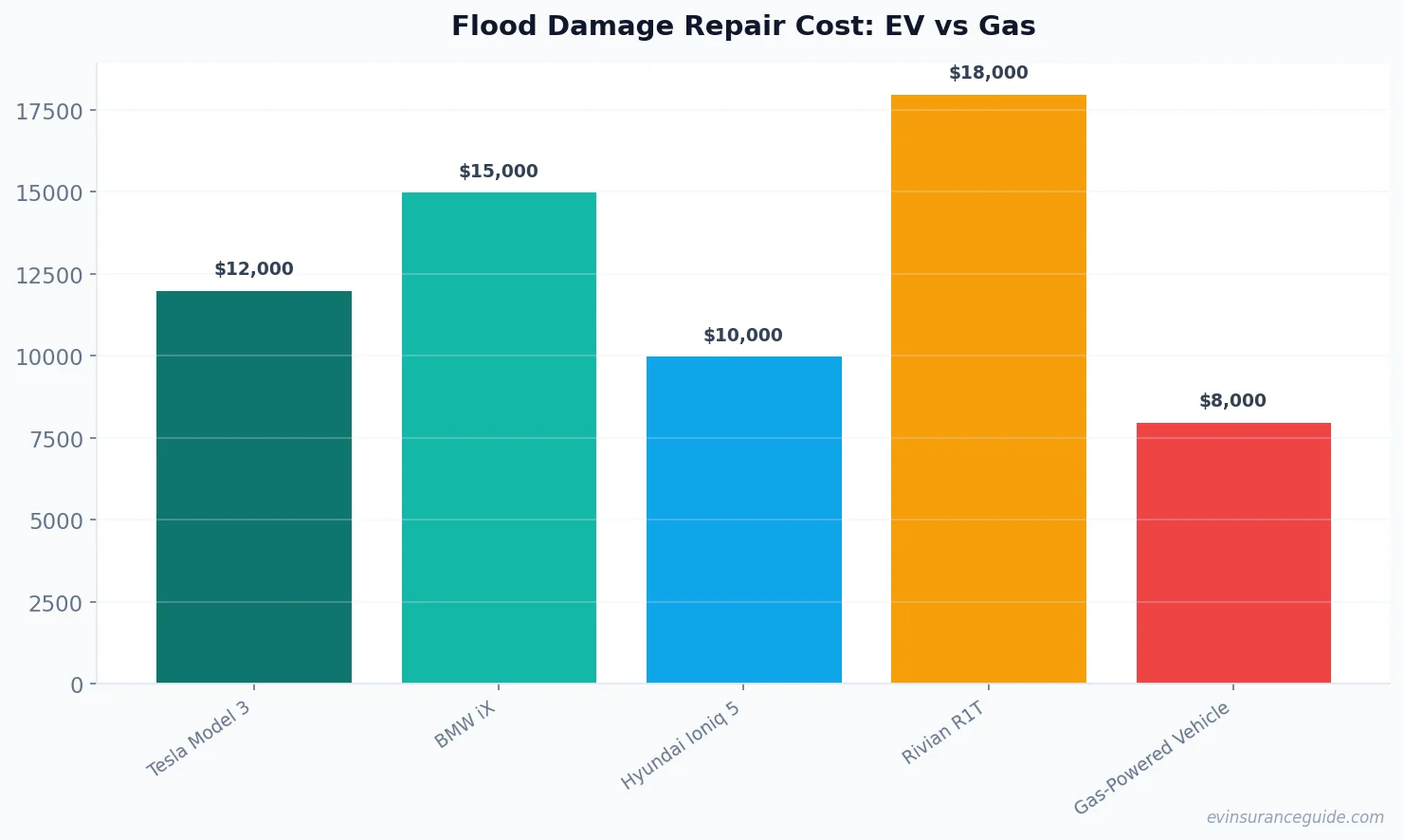

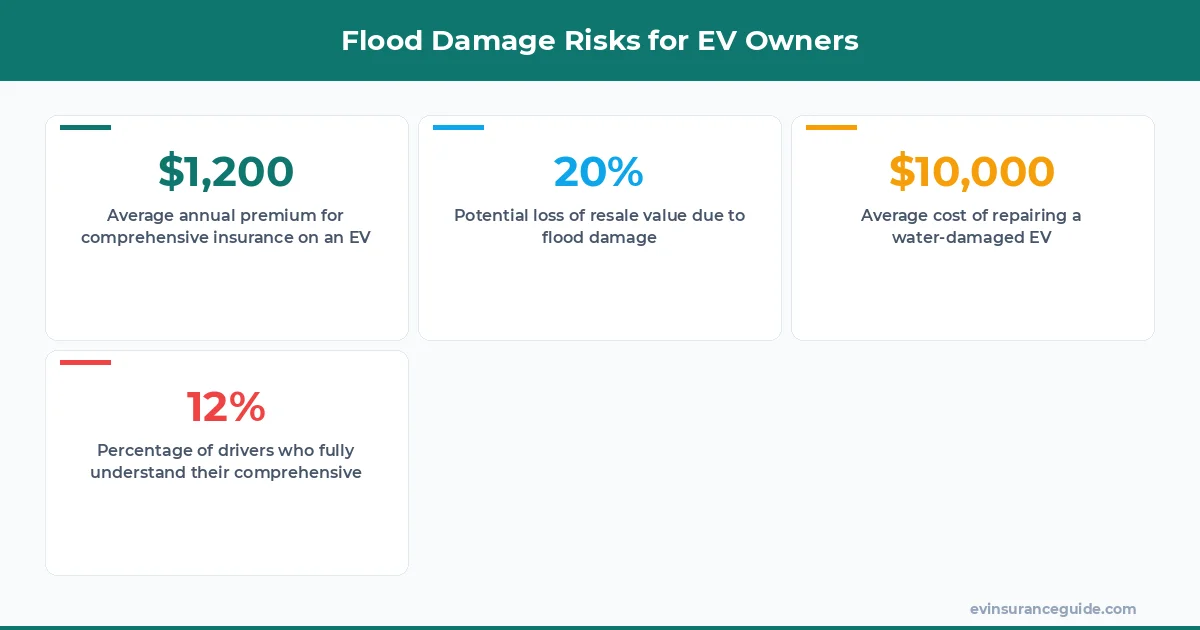

Comprehensive insurance is designed to cover damages that aren't related to collisions – think theft, vandalism, or natural disasters like floods. But here's the thing: not all comprehensive policies are created equal. Some insurers, like Geico, offer more generous coverage for flood damage, while others, like State Farm, might have more restrictive policies. Know what the kicker is? The cost of repairing a water-damaged EV can be astronomical – we're talking upwards of $10,000 to $20,000 or more, depending on the make and model. For example, a Tesla Model 3 with extensive water damage might require a new battery pack, which can cost around $15,000.

But what about the ev lease vs buy insurance implications? Well, if you're leasing an EV, you might not have a choice – the lessor will likely require comprehensive insurance. And if you're buying, you'll still want to consider comprehensive insurance to protect your investment. That's where the ev lease vs buy insurance debate comes in: which option offers better protection against flood damage? According to a study by the National Insurance Crime Bureau, the average annual premium for comprehensive insurance on an EV is around $1,200.

And let's not forget about the impact of flood damage on resale value. A water-damaged EV can lose up to 20% of its value, according to a report by Kelley Blue Book. That's a significant hit, especially if you're planning to sell your vehicle in the future. So, when it comes to ev lease vs buy insurance, you'll want to consider the potential risks and costs associated with flood damage.

Does Your EV Lease vs Buy Insurance Policy Cover Flood Damage?

So, does your insurance policy cover flood damage? The answer is: it depends. If you've got a comprehensive policy from a reputable insurer like Allstate, you're probably covered. But if you've opted for a bare-bones policy from a cut-rate insurer, you might be out of luck. Wild, right? You'd think that comprehensive insurance would, well, cover everything – but that's not always the case. For example, a study by the Insurance Information Institute found that only 12% of drivers fully understand what their comprehensive insurance policy covers.

To give you a better idea, let's look at some specific EV models and their comprehensive insurance costs. A BMW iX, for instance, might cost around $1,500 per year to insure, while a Hyundai Ioniq 5 might cost around $1,200 per year. And if you're leasing an EV, your insurance costs might be even higher – up to $2,000 per year or more, depending on the terms of your lease.

But what about the ev lease vs buy insurance implications? If you're leasing an EV, you'll want to make sure your insurance policy covers flood damage, since you'll be responsible for any damages that occur during the lease term. And if you're buying, you'll want to consider the long-term costs of owning an EV, including the potential risks of flood damage.

Pro tip: always read the fine print on your insurance policy. If you're not sure what's covered, ask your insurer – or better yet, get a second opinion from a reputable insurance expert.

7 Key Factors to Consider When Choosing EV Lease vs Buy Insurance

So, what are the key factors to consider when choosing an insurance policy for your EV? Here are 7 things to keep in mind:

- 1. Comprehensive coverage: Make sure your policy includes comprehensive coverage, which will protect you against flood damage and other non-collision-related damages.

- 2. Deductible: Choose a policy with a reasonable deductible – you don't want to be stuck paying thousands of dollars out of pocket if your EV is damaged in a flood.

- 3. Coverage limits: Make sure your policy has sufficient coverage limits to cover the cost of repairing or replacing your EV.

- 4. Insurer reputation: Research the insurer's reputation and financial stability – you want to make sure they'll be around to pay out claims if needed.

- 5. EV-specific coverage: Some insurers offer EV-specific coverage, which can include perks like battery protection and charging station coverage.

- 6. Lease vs buy: Consider the ev lease vs buy insurance implications, including the potential risks and costs associated with flood damage.

- 7. Cost: Finally, consider the cost of the policy – you don't want to break the bank, but you also don't want to skimp on coverage.

And let's not forget about the impact of flood damage on the environment. A study by the National Oceanic and Atmospheric Administration found that flooding can contaminate soil and water with toxic chemicals, which can harm local ecosystems. So, when it comes to ev lease vs buy insurance, you'll want to consider the potential environmental risks associated with flood damage.

The Shocking Story of a Water-Damaged Tesla Model Y

I've got a friend, let's call her Rachel, who owns a Tesla Model Y. She parked it in her garage during a heavy storm, and woke up to find that the garage had flooded – and her car was underwater. The damage was extensive: the battery pack was ruined, and the electronics were shot. The repair bill? A whopping $18,000. But here's the thing: Rachel's insurer, Progressive, covered the entire cost – she only had to pay her deductible. That's what I call good insurance.

And here's a data point to illustrate the risk: according to a report by the Federal Emergency Management Agency, the average cost of flood damage to a vehicle is around $3,000. But for EVs, the cost can be much higher – up to $10,000 or more, depending on the make and model.

Warning: Don't Assume Your EV Lease vs Buy Insurance Policy Covers Everything

Don't assume that your insurance policy covers everything – because it probably doesn't. For example, some policies might not cover damage from flooding caused by a storm surge, or damage to the vehicle's electrical system. And if you're leasing an EV, you might be on the hook for any damages that occur during the lease term – even if they're not your fault. So, it's essential to read the fine print and understand what's covered – and what's not. For instance, a policy from Liberty Mutual might cover flood damage, but only up to a certain amount – say, $10,000. If the damage exceeds that amount, you'll be responsible for the rest.

And let's not forget about the potential hidden costs associated with flood damage. A study by the Insurance Information Institute found that many drivers underestimate the cost of flood damage, and end up paying more out of pocket than they expected. So, when it comes to ev lease vs buy insurance, you'll want to consider the potential hidden costs associated with flood damage.

FAQs

#### What is comprehensive insurance, and how does it cover flood damage?

Comprehensive insurance is designed to cover damages that aren't related to collisions – think theft, vandalism, or natural disasters like floods. It typically covers flood damage, but the extent of the coverage depends on the policy and the insurer. For example, a policy from USAA might cover flood damage up to $15,000, while a policy from Geico might cover up to $20,000.

#### How much does comprehensive insurance cost for an EV?

The cost of comprehensive insurance for an EV can vary widely, depending on the make and model of the vehicle, the location, and the insurer. On average, comprehensive insurance for an EV can cost between $1,000 and $2,000 per year. For example, a Tesla Model 3 might cost around $1,200 per year to insure, while a Rivian R1T might cost around $1,800 per year.

#### What are the ev lease vs buy insurance implications for flood damage?

If you're leasing an EV, you'll want to make sure your insurance policy covers flood damage, since you'll be responsible for any damages that occur during the lease term. And if you're buying, you'll want to consider the long-term costs of owning an EV, including the potential risks of flood damage.

#### Can I get EV-specific coverage for my vehicle?

Yes, some insurers offer EV-specific coverage, which can include perks like battery protection and charging station coverage. For example, a policy from Tesla might include coverage for the vehicle's battery pack, as well as coverage for charging stations and other EV-specific components.

#### How can I reduce my risk of flood damage to my EV?

To reduce your risk of flood damage to your EV, make sure to park your vehicle in a safe location, away from flood-prone areas. You should also consider investing in a flood protection system, such as a waterproof cover or a flood-resistant parking garage.

#### What are the potential environmental risks associated with flood damage to EVs?

Flood damage to EVs can contaminate soil and water with toxic chemicals, which can harm local ecosystems. A study by the National Oceanic and Atmospheric Administration found that flooding can release toxic chemicals from vehicles, including heavy metals and petroleum products.

#### Are there any discounts available for EV owners who invest in flood protection systems?

Yes, some insurers offer discounts for EV owners who invest in flood protection systems, such as waterproof covers or flood-resistant parking garages. For example, a policy from Allstate might offer a 10% discount for EV owners who invest in a flood protection system.

Until next time — Alex