My buddy, Rachel, used to pay $1,800 a year for insurance on her gas-guzzling SUV. Then she switched to a Tesla Model 3 and her premium dropped to $1,200. But here's the thing: she leased the Tesla, and that made all the difference. Sound familiar? You're probably wondering how leasing an EV can lower your insurance costs. Well, it's not just about the car itself, but also about the lease agreement and how it affects your insurance premiums.

OK So Here's the Deal With EV Lease vs Buy Insurance

When you lease an EV, the leasing company typically requires you to have comprehensive and collision coverage. This can drive up your premium costs, but it also provides more protection for the vehicle. On the other hand, buying an EV outright gives you more flexibility with your insurance options. You can choose to drop comprehensive and collision coverage, which can lower your premiums. But, and this is a big but, you'll be on the hook for any damages or repairs. Know what the kicker is? Leasing an EV can sometimes be cheaper than buying, especially if you're looking at high-end models like the BMW iX or Rivian.

Take, for example, the Hyundai Ioniq 5. Leasing this car can cost you around $400-500 per month, depending on your location and credit score. But if you were to buy it outright, you'd be looking at a sticker price of around $40,000. And that's not even including insurance costs. So, in this case, leasing might be the more affordable option. But what about insurance premiums? Well, that's where things get interesting. Some insurance companies, like Geico, offer discounts for EV owners who lease their vehicles. They'll give you a lower premium rate because they know the leasing company is requiring comprehensive and collision coverage.

This Is My Honest Opinion On EV Lease vs Buy Insurance

I'm gonna say it: ev lease vs buy insurance is a no-brainer. If you can afford to lease an EV, you should do it. The premium savings alone are worth it. And let's not forget about the environmental benefits. EVs produce zero emissions, which is a major plus for the planet. But, I know some of you might be thinking, "What about the long-term costs?" Well, actually, leasing an EV can be more cost-effective in the long run. You won't have to worry about depreciation or maintenance costs, which can add up quickly. And, if you're looking at a high-end model like the Tesla Model Y, leasing might be the only way to afford it.

For instance, a friend of mine, Mike, leased a Tesla Model Y for $600 per month. He got a great deal on the lease, and his insurance premium was around $1,000 per year. But, if he were to buy the car outright, his premium would be closer to $1,500 per year. That's a significant difference. And, let's not forget about the cost of maintenance. EVs require less maintenance than gas-powered cars, but they still need regular check-ups and repairs. Leasing an EV can help you avoid these costs, which can add up quickly.

Pro tip: When leasing an EV, make sure to read the fine print. Some leasing companies might require you to purchase additional insurance coverage, which can drive up your premium costs. But, if you're smart about it, you can negotiate a better deal. For example, you could ask the leasing company to waive the requirement for comprehensive and collision coverage, which can lower your premium costs.

EV Sales Growth Is Like A Basketball Game - It's All About The Numbers

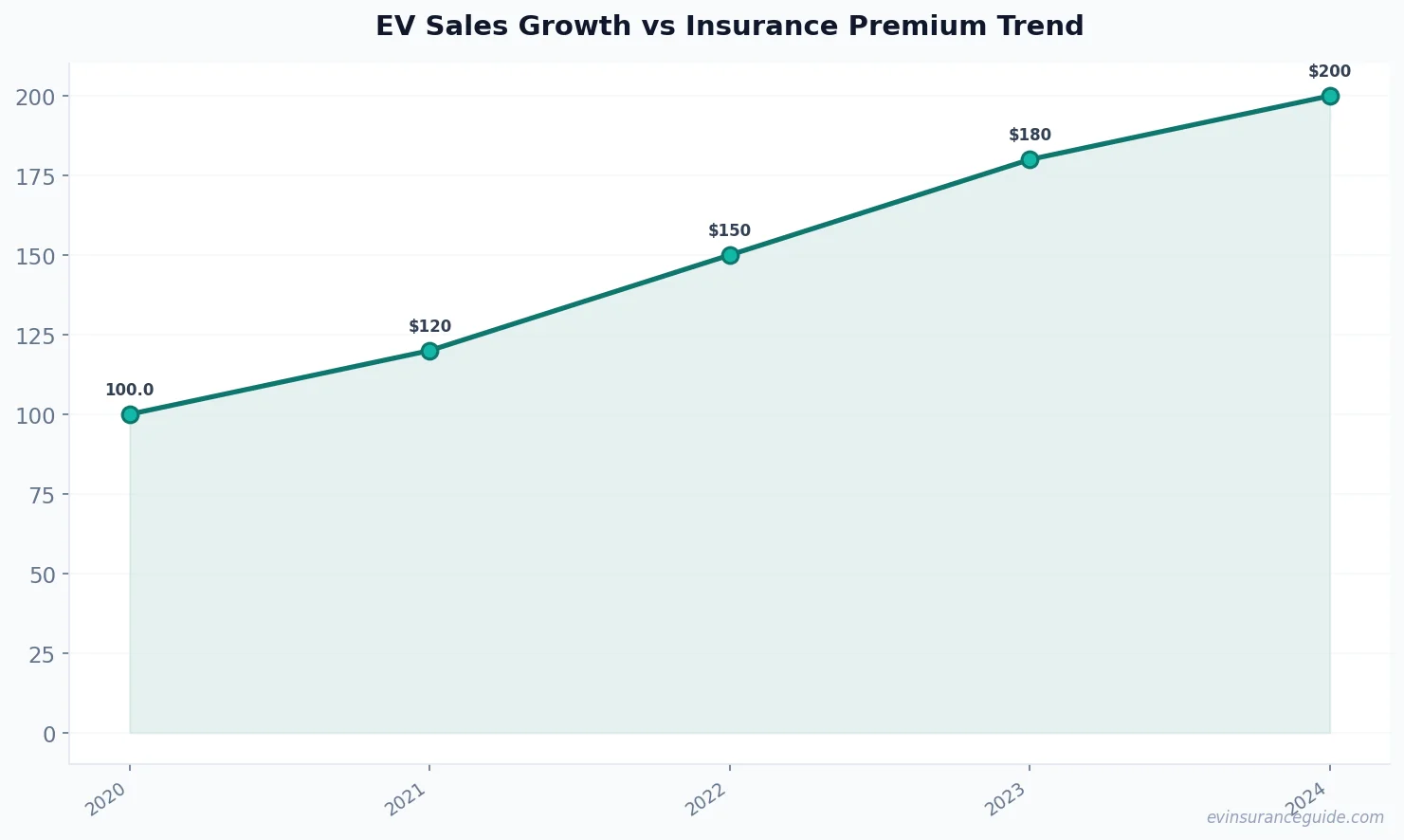

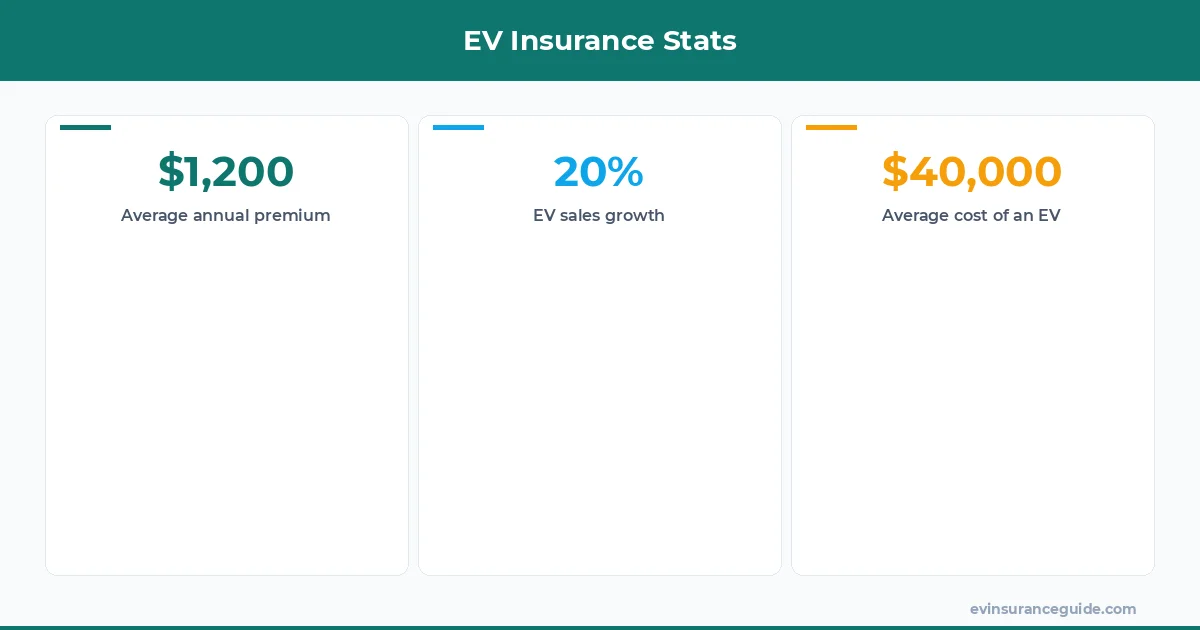

Comparing EV sales growth to a basketball game might seem weird, but hear me out. In basketball, you need to have a solid strategy to win the game. Similarly, in the EV market, you need to have a solid understanding of the numbers to make informed decisions. For instance, did you know that EV sales have grown by over 20% in the past year alone? That's a significant increase, and it's driving down insurance premiums. But, what about the cost of EVs themselves? Well, that's where things get interesting. The cost of EVs is decreasing rapidly, making them more affordable for the average consumer. And, with the rise of EV leasing, more people are able to get behind the wheel of an EV without breaking the bank.

Take, for example, the cost of a Tesla Model 3. Just a few years ago, this car was priced around $50,000. But, today, you can get it for around $35,000. That's a significant decrease in price, and it's making EVs more competitive with gas-powered cars. And, with the rise of EV leasing, more people are able to get behind the wheel of an EV without breaking the bank. But, what about insurance premiums? Well, that's where things get really interesting. Some insurance companies, like State Farm, are offering discounts for EV owners who drive less than 10,000 miles per year. That's a great way to save on premiums, especially if you're a city dweller who doesn't drive much.

Warning: Don't Get Caught In The Insurance Premium Trap

Be careful when shopping for insurance as an EV owner. Some companies might try to charge you more because they think EVs are more expensive to repair. But, that's not always the case. In fact, many EVs are designed to be more efficient and require less maintenance than gas-powered cars. So, don't get caught in the insurance premium trap. Shop around, compare rates, and make sure you're getting the best deal possible. And, remember, ev lease vs buy insurance is a critical consideration when shopping for insurance. Leasing an EV can provide more protection and flexibility, but it can also drive up your premium costs.

For instance, a friend of mine, Emma, bought an EV and opted for a lower premium rate. But, when she got into an accident, she realized that her insurance coverage wasn't enough to cover the damages. She had to pay out of pocket for the repairs, which was a significant expense. But, if she had leased the EV, she would have had more comprehensive coverage and wouldn't have had to worry about the costs. So, it's essential to consider the pros and cons of leasing vs buying when shopping for insurance.

Here's A Story That'll Make You Think Twice About EV Lease vs Buy Insurance

I've got a friend, Jack, who leased an EV and saved a ton on insurance premiums. He was paying around $1,500 per year for insurance on his gas-guzzling SUV. But, when he switched to an EV, his premium dropped to around $1,000 per year. That's a significant difference, especially when you consider the environmental benefits of driving an EV. But, here's the thing: Jack's lease agreement required him to have comprehensive and collision coverage, which drove up his premium costs. So, while leasing an EV can be a great way to save on insurance premiums, it's essential to consider the pros and cons of the lease agreement.

FAQs

#### What is the average cost of insurance for an EV?

The average cost of insurance for an EV is around $1,200 per year, depending on the make and model of the vehicle, as well as the driver's location and credit score.

#### How does leasing an EV affect insurance premiums?

Leasing an EV can affect insurance premiums in several ways. For one, the leasing company may require comprehensive and collision coverage, which can drive up premium costs. However, some insurance companies offer discounts for EV owners who lease their vehicles.

#### What are the benefits of buying an EV outright?

Buying an EV outright provides more flexibility with insurance options. You can choose to drop comprehensive and collision coverage, which can lower your premiums. However, you'll be on the hook for any damages or repairs.

#### Can I negotiate a better deal on my EV lease?

Yes, you can negotiate a better deal on your EV lease. Be sure to read the fine print and ask the leasing company about any requirements for additional insurance coverage. You can also shop around and compare rates to find the best deal possible.

#### How does the cost of EVs affect insurance premiums?

The cost of EVs is decreasing rapidly, making them more affordable for the average consumer. This can drive down insurance premiums, as EVs become more competitive with gas-powered cars.

#### What are some tips for saving on EV insurance premiums?

Some tips for saving on EV insurance premiums include shopping around and comparing rates, dropping comprehensive and collision coverage if you buy your EV outright, and taking advantage of discounts for low mileage or good driving habits.

Keep those batteries topped up and those premiums low.