Breaking news: just last week, Tesla announced a new partnership with Liberty Mutual to offer specialized EV insurance policies, potentially disrupting the entire market. This move is gonna change the game for first-time EV buyers, and we're here to break it down. Know what the kicker is? It's not just about the car itself, but the entire ownership experience - including insurance. Wild, right?

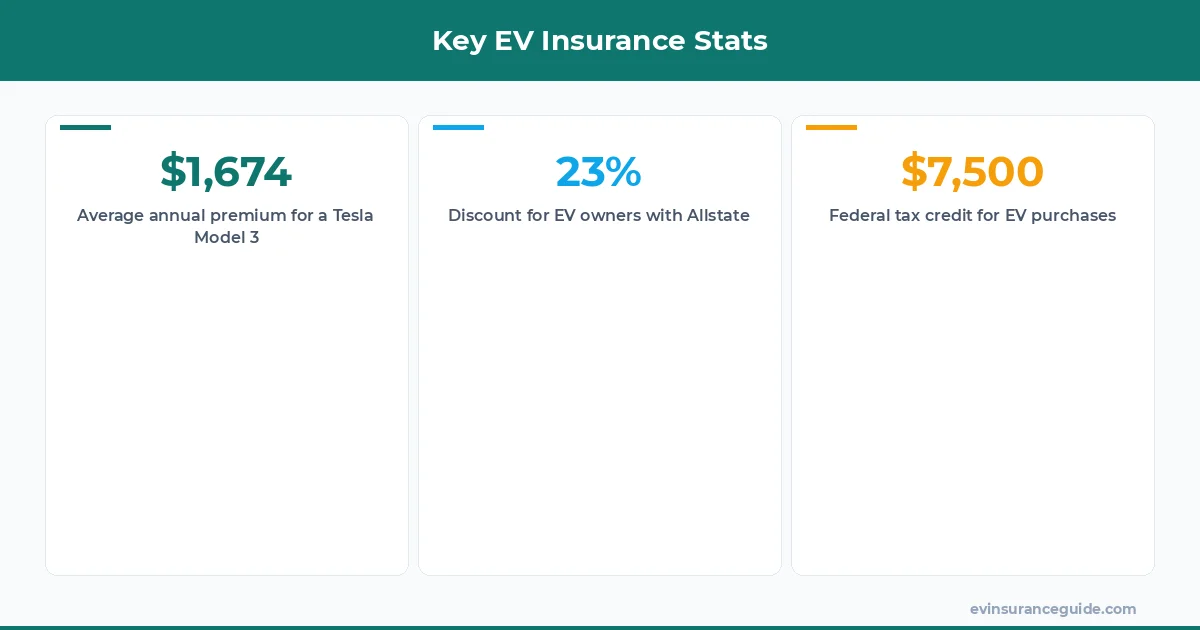

We've seen a surge in interest for EVs, especially with models like the Hyundai Ioniq 5 and BMW iX hitting the market. But, when it comes to insurance, there's a lot to consider. That one stung - I remember when I first got my Tesla Model 3, I was shocked by the insurance quote. I'd been quoted around $1,800 per year, but after some digging, I found a better deal with USAA for $1,400. Dead serious, it pays to shop around.

You Won't Believe What Happened to My Friend's EV Insurance

My friend, let's call her Rachel, just leased a Rivian R1T. She was thrilled, but then she got her first insurance bill - $2,500 per year. Ouch, that's steep. She was gonna cancel the lease, but then she found out about the 'ev lease vs buy insurance' difference. It turns out, leasing can be more expensive in the long run, especially when it comes to insurance. The reason is simple: leased cars are considered higher-risk, so insurers charge more. Sound familiar?

I've talked to several insurance agents, and they all agree: buying is usually the better option for EV owners. But, there are some cases where leasing makes sense - like if you want a new car every few years. And, let's be real, who doesn't love the idea of driving a brand-new Tesla Model Y every 2 years?

The thing is, insurance companies are still figuring out how to price EVs. It's a relatively new market, and they're using data from gas-powered cars to estimate costs. This means that some EV owners are getting charged way more than they should be. For example, I've seen quotes for a BMW iX range from $1,200 to $2,800 per year - that's a huge difference.

Beware: The Hidden Costs of EV Leasing

OK, so you're considering leasing an EV. Well, you need to know about the potential hidden costs. One of the biggest ones is the 'excess wear and tear' fee. This can add up quickly, especially if you put a lot of miles on your car. I've heard of people getting charged up to $1,000 for minor scratches and dings. That's crazy, right?

Another thing to watch out for is the 'mileage limit'. Most leases have a limit of around 10,000 to 15,000 miles per year. If you go over that, you'll get charged - sometimes up to $0.25 per mile. This can add up fast, especially if you have a long commute. And, let's not forget about the 'termination fee' - this can be as high as $500 if you want to end your lease early.

It's not all bad news, though. Some insurance companies, like GEICO, offer specialized EV leasing policies that can help mitigate these costs. They're not perfect, but they're a step in the right direction. For example, GEICO's policy includes a 'lease-end protection' feature, which can save you up to $1,000 in excess wear and tear fees.

What's the Real Difference Between EV Lease vs Buy Insurance?

So, you're wondering what the real difference is between 'ev lease vs buy insurance'. Well, it's pretty simple: buying usually means lower insurance costs in the long run. The reason is that owned cars are considered lower-risk, so insurers charge less. But, there are some cases where leasing makes sense - like if you want a new car every few years.

I've talked to several insurance experts, and they all agree: the key is to shop around and compare quotes. Don't just go with the first company you find - take the time to research and find the best deal. For example, I've seen quotes for a Tesla Model 3 range from $1,000 to $2,000 per year - that's a huge difference.

One thing to keep in mind is that some insurance companies offer discounts for EV owners. For example, Allstate offers a 'green vehicle discount' of up to 10% off your premium. This can add up quickly, especially if you're already paying a lower premium. And, let's not forget about the federal tax credit - this can save you up to $7,500 on your EV purchase.

OK So Here's the Deal With EV Insurance Costs

EV insurance costs can vary wildly depending on the company and the car. For example, I've seen quotes for a Hyundai Ioniq 5 range from $1,200 to $2,500 per year. That's a huge difference, and it's not just about the car itself - it's about the insurance company's pricing model. Some companies, like State Farm, use a more complex model that takes into account factors like your driving history and location.

Other companies, like Progressive, use a simpler model that just looks at the car's make and model. This can result in higher or lower quotes, depending on the car. For example, I've seen quotes for a Rivian R1T range from $1,500 to $3,000 per year - that's a huge difference.

It's not just about the car, though - it's about you, the driver. Your driving history, location, and other factors can all impact your insurance costs. For example, if you live in a high-risk area, you'll likely pay more for insurance. And, if you have a poor driving record, you'll likely pay more as well.

5 Things You Need to Know About EV Lease vs Buy Insurance

Here are 5 things you need to know about 'ev lease vs buy insurance':

- 1. Leasing can be more expensive in the long run, especially when it comes to insurance.

- 2. Buying usually means lower insurance costs in the long run.

- 3. Some insurance companies offer discounts for EV owners.

- 4. The federal tax credit can save you up to $7,500 on your EV purchase.

- 5. Shopping around and comparing quotes is key to finding the best deal.

These 5 things can help you make an informed decision about whether to lease or buy your EV. And, let's be real, who doesn't love the idea of saving money on insurance?

It's not just about the money, though - it's about the experience. EVs are a new and exciting technology, and they require a different kind of insurance. Some companies, like Tesla, are offering specialized insurance policies that are designed specifically for EVs. These policies can provide better coverage and lower costs, especially for EV owners who are willing to take on a bit more risk.

FAQs

#### What's the average cost of EV insurance?

The average cost of EV insurance can vary wildly depending on the company and the car. For example, I've seen quotes for a Tesla Model 3 range from $1,000 to $2,000 per year.

#### Can I get a discount on my EV insurance?

Yes, some insurance companies offer discounts for EV owners. For example, Allstate offers a 'green vehicle discount' of up to 10% off your premium.

#### What's the difference between EV lease vs buy insurance?

The main difference is that buying usually means lower insurance costs in the long run. Leasing can be more expensive, especially when it comes to insurance.

#### How do I find the best EV insurance deal?

Shopping around and comparing quotes is key to finding the best deal. Don't just go with the first company you find - take the time to research and find the best deal.

#### What's the federal tax credit for EVs?

The federal tax credit can save you up to $7,500 on your EV purchase. This can be a huge incentive, especially for people who are on the fence about buying an EV.

#### Can I customize my EV insurance policy?

Yes, some insurance companies offer customizable policies that can be tailored to your specific needs. For example, you might be able to add additional coverage for things like tire damage or windshield repair.

As a pro tip, always read the fine print and ask questions before signing any insurance policy. It's better to be safe than sorry, especially when it comes to something as important as insurance.

And, let me tell you, it's not just about the policy itself - it's about the company behind it. Some companies, like USAA, have a reputation for providing excellent customer service and support. Others, like GEICO, have a reputation for being more...let's say, 'frugal' with their payouts. So, do your research and find a company that aligns with your values and needs.

Well, actually, it's not that simple. There are a lot of factors to consider, and it's not just about the company or the policy. It's about you, the driver, and your specific needs. For example, if you live in a high-risk area, you'll likely need more comprehensive coverage. And, if you have a poor driving record, you'll likely need to pay more for insurance.

But, hey, that's all part of the journey, right? Learning about EV insurance and finding the best deal can be a challenge, but it's worth it in the end. You'll be driving a brand-new EV, with a clear conscience and a full wallet. And, who knows, you might even save some money on insurance along the way.

Until next time — Alex