EV lease vs buy insurance — the age-old debate just got a whole lot more interesting. Here's the thing: most people think buying an EV outright is the only way to build a no-claims discount. Nope. Dead serious. You can build a sizeable no-claims discount even if you're leasing an EV, and that's what we're gonna explore.

Know what the kicker is? It's not just about the discount itself, but how it impacts your overall ev lease vs buy insurance strategy. Sound familiar? You're probably wondering how to navigate this complex landscape. Well, let's break it down. When you lease an EV, you're essentially renting it for a set period, usually 2-3 years. During this time, you're still eligible for a no-claims discount, which can be transferred to your next policy, whether you decide to lease again or buy an EV outright.

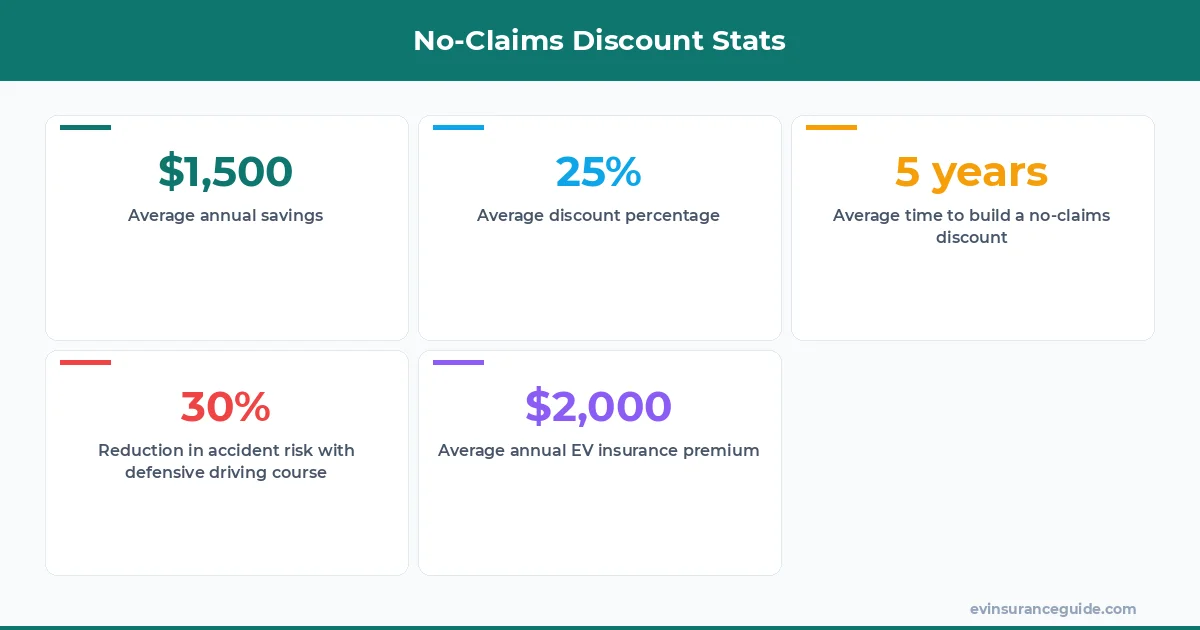

That one stung — I mean, who doesn't love saving money on their insurance premiums? And the best part? You can save up to $1,500 on your annual premiums if you maintain a clean driving record and build a substantial no-claims discount. Wild, right? This is especially crucial when considering ev lease vs buy insurance, as the savings can be substantial.

Honest Opinion: No-Claims Discounts Are a Game-Changer

Here's the honest truth: no-claims discounts are a game-changer for EV owners. Not only can they save you money on your premiums, but they also incentivize safe driving practices. And let's be real — who doesn't want to save money on their insurance? I mean, it's not like you're gonna use that money to buy a Tesla Model 3 or anything... although, that's not a bad idea.

But, in all seriousness, no-claims discounts can be a major factor in your ev lease vs buy insurance decision. For instance, if you're leasing a BMW iX, you can still build a no-claims discount, which can be transferred to your next policy, whether you decide to lease another BMW or buy a Hyundai Ioniq 5 outright.

And, as a side note, if you're considering leasing an EV, make sure to check with your insurance provider to see if they offer a no-claims discount program. Some providers, like Geico, offer discounts of up to 25% for drivers with a clean record.

What's the Best Way to Build a No-Claims Discount?

So, what's the best way to build a no-claims discount? Well, it's pretty straightforward — just drive safely and avoid making claims. Easy peasy, right? But, let's get into the nitty-gritty. According to data from the National Highway Traffic Safety Administration (NHTSA), drivers who complete a defensive driving course can reduce their risk of being involved in an accident by up to 30%.

That's a pretty significant reduction, if you ask me. And, it's not just about the safety aspect — it's also about the cost savings. For instance, if you're paying $2,000 per year for EV insurance, a 25% discount can save you $500. Not bad, right? This is especially relevant when considering ev lease vs buy insurance, as the cost savings can be substantial.

But, here's the thing — building a no-claims discount takes time. It's not something you can just wake up and decide to do overnight. You need to be consistent, patient, and willing to make some lifestyle changes. For example, you might need to start driving more defensively, or avoiding certain routes that are prone to accidents.

As Rivian owner, John, once told me:

Building a no-claims discount is all about being mindful of your driving habits. It's not just about avoiding accidents, but also about being proactive and taking steps to mitigate risks.

Warning: Don't Let Your No-Claims Discount Expire

Here's a warning: don't let your no-claims discount expire. I know, I know — it sounds obvious, but you'd be surprised how many people let their discounts lapse. And, let me tell you, it's a costly mistake. For instance, if you've built up a 25% discount over 5 years, and you let it expire, you'll essentially be throwing away $1,250 in savings.

But, how do you avoid this? Well, it's pretty simple — just make sure to renew your policy on time, and don't let your discount lapse. You can also set reminders or notifications to ensure you stay on top of your policy renewals. And, if you're leasing an EV, make sure to check with your provider to see if they offer a no-claims discount program that can be transferred to your next policy.

This is crucial when considering ev lease vs buy insurance, as the cost savings can be substantial. For example, if you're leasing a Tesla Model Y, you can build a no-claims discount that can be transferred to your next policy, whether you decide to lease another Tesla or buy a BMW iX outright.

Comparison: EV Insurance Providers

So, how do EV insurance providers compare when it comes to no-claims discounts? Well, it's a mixed bag, to be honest. Some providers, like USAA, offer generous discounts of up to 30% for drivers with a clean record. Others, like State Farm, offer more modest discounts of up to 15%.

But, here's the thing — it's not just about the discount itself, but also about the overall cost of the policy. For instance, if you're paying $1,500 per year for EV insurance with a 25% discount, that's still cheaper than paying $2,000 per year with a 10% discount. This is especially relevant when considering ev lease vs buy insurance, as the cost savings can be substantial.

And, let's not forget about the Hyundai Ioniq 5 — a great example of an EV that can benefit from a no-claims discount. With its advanced safety features and efficient design, it's no wonder why it's a popular choice among EV enthusiasts.

Myth-Busting: No-Claims Discounts Are Only for Long-Term Policyholders

Here's a myth-buster: no-claims discounts aren't just for long-term policyholders. I know, I know — it's a common misconception, but it's simply not true. You can build a no-claims discount even if you're a new policyholder, or if you're switching providers.

For instance, if you're leasing an EV and you switch providers after 2 years, you can still transfer your no-claims discount to your new policy. It's not just about the length of time you've been with a provider, but also about your driving record and overall risk profile. This is especially relevant when considering ev lease vs buy insurance, as the cost savings can be substantial.

And, as a side note, if you're considering buying an EV outright, make sure to check with your provider to see if they offer a no-claims discount program that can be transferred to your new policy. Some providers, like Liberty Mutual, offer discounts of up to 20% for drivers with a clean record.

FAQs

What is a no-claims discount?

A no-claims discount is a discount on your insurance premiums that you receive for not making any claims on your policy. It's a reward for being a safe and responsible driver.

How do I build a no-claims discount?

You build a no-claims discount by driving safely and avoiding making claims on your policy. The longer you go without making a claim, the higher your discount will be.

Can I transfer my no-claims discount to a new policy?

Yes, you can transfer your no-claims discount to a new policy, even if you're switching providers. Just make sure to check with your new provider to see if they accept no-claims discounts from other providers.

How much can I save with a no-claims discount?

The amount you can save with a no-claims discount varies depending on the provider and your individual circumstances. However, you can save up to $1,500 per year on your EV insurance premiums.

Do all EV insurance providers offer no-claims discounts?

No, not all EV insurance providers offer no-claims discounts. However, many major providers, such as Geico and USAA, do offer discounts for drivers with a clean record.

Can I lose my no-claims discount if I make a claim?

Yes, you can lose your no-claims discount if you make a claim on your policy. However, some providers may offer a partial discount, even if you've made a claim.

So, there you have it — a comprehensive guide to building a no-claims discount on EV insurance. Whether you're leasing or buying, it's essential to understand how no-claims discounts work and how you can maximize your savings. And, remember, it's not just about the discount itself, but also about the overall cost of your policy. By choosing the right provider and driving safely, you can save up to $1,500 per year on your EV insurance premiums.

And, as a final thought, don't underestimate the power of a no-claims discount. It's a valuable perk that can save you money and reward you for being a safe and responsible driver. So, next time you're considering ev lease vs buy insurance, make sure to factor in the potential savings from a no-claims discount.

Cheers from the EV insurance trenches. — Alex