I'm standing at a charging station, watching a Tesla Model 3 charge up, when I overhear a conversation between two guys about ev lease vs buy insurance. One of them mentions how he got burned on his last lease because the resale value of his car tanked. The other guy nods in agreement, saying he's had similar issues with his BMW iX. That's when it hits me - resale value plays a huge role in ev lease vs buy insurance. Sound familiar? You're not alone.

Know what the kicker is? Insurers care about resale value too, and it affects your premiums. Wild, right? I mean, think about it - if your car holds its value, you're less likely to be upside down on your loan or lease, which means less risk for the insurer. That's why it's crucial to consider resale value when deciding between ev lease vs buy insurance.

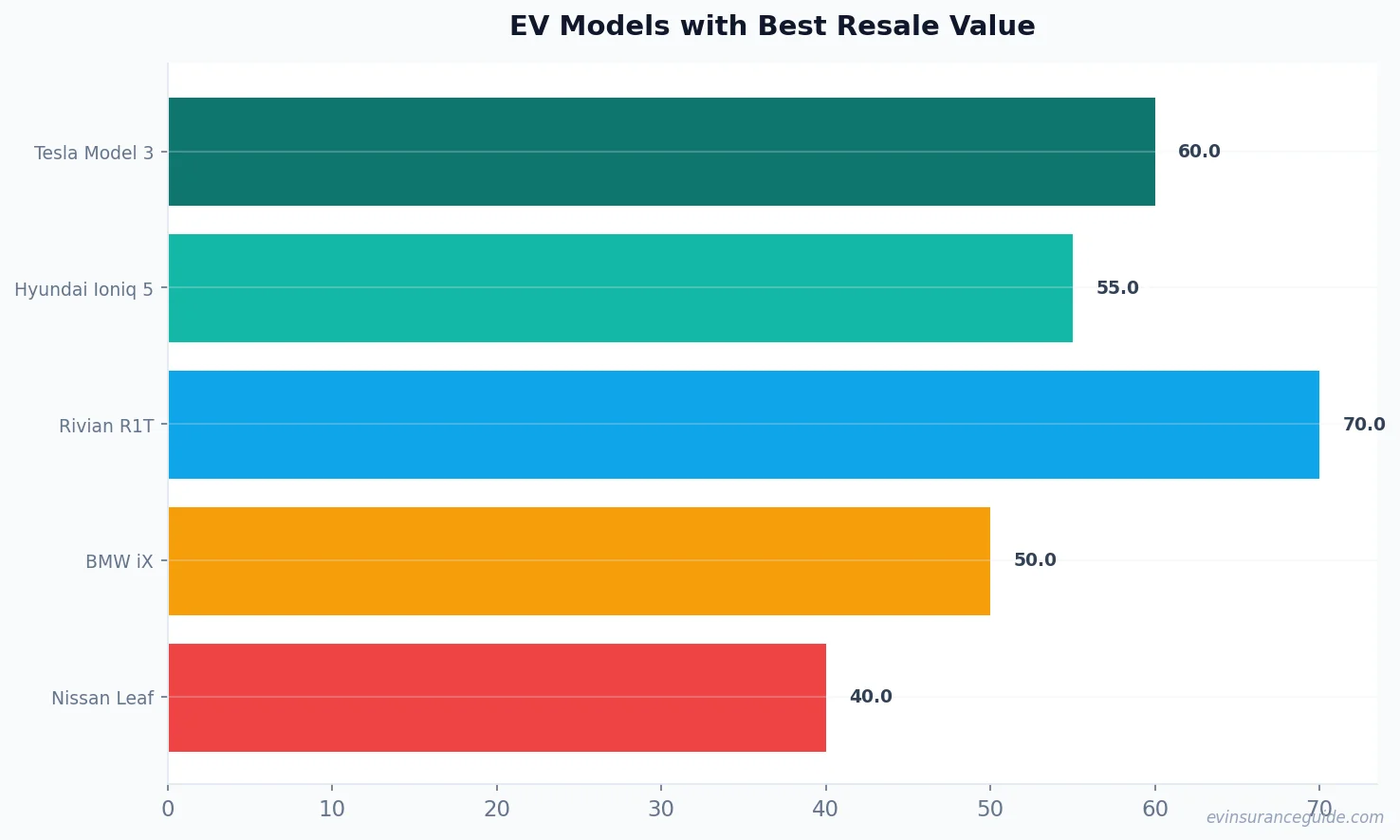

OK, so let's look at some numbers. According to data from Kelley Blue Book, the Tesla Model 3 retains around 60% of its value after 3 years, while the Hyundai Ioniq 5 retains around 55%. The Rivian R1T, on the other hand, retains a whopping 70% of its value after 3 years. That's a significant difference, and it can impact your ev lease vs buy insurance costs. For example, if you lease a Tesla Model 3 for 3 years, you can expect to pay around $500-700 per month, depending on your location and driving habits. But if you buy the same car, your insurance premiums could be higher due to the lower resale value.

OK So Here's the Deal With EV Lease vs Buy Insurance

When it comes to ev lease vs buy insurance, you gotta consider the resale value of your car. I mean, it's not just about the monthly payments or the overall cost of the vehicle. You gotta think about how much your car will be worth in 3-5 years, and how that will affect your insurance premiums. For instance, if you lease a car with a high resale value, like the Tesla Model Y, your insurance premiums might be lower because the insurer knows they can sell the car for a good price if you total it. On the other hand, if you buy a car with a low resale value, like the Nissan Leaf, your insurance premiums might be higher because the insurer knows they'll take a hit if they have to sell the car.

But here's the thing - not all EVs are created equal when it comes to resale value. Some cars, like the Tesla Model 3, hold their value incredibly well, while others, like the Fiat 500e, don't do so great. And that's why it's crucial to do your research before deciding between ev lease vs buy insurance. You gotta look at the data, talk to other owners, and consider the overall cost of ownership. For example, a study by iSeeCars found that the top 5 EVs with the best resale value are: Tesla Model 3, Tesla Model Y, Hyundai Ioniq 5, Rivian R1T, and BMW iX. These cars retain around 50-70% of their value after 3 years, which is significantly higher than the average EV.

And let's not forget about the impact of technology on resale value. I mean, think about it - if your car has outdated tech, it's gonna be worth less in a few years. But if your car has the latest and greatest tech, it's gonna hold its value better. For instance, the Tesla Model 3 has a massive touchscreen display and Autopilot capabilities, which makes it a more desirable car. On the other hand, the Nissan Leaf has a more basic infotainment system, which might make it less desirable to buyers.

This Is the Honest Truth About EV Lease vs Buy Insurance

Look, I'm gonna give it to you straight - ev lease vs buy insurance is a complex topic, and there's no one-size-fits-all answer. But here's what I do know: if you're considering leasing an EV, you gotta think about the resale value of the car. I mean, it's not just about the monthly payments or the overall cost of the vehicle. You gotta think about how much the car will be worth in 3-5 years, and how that will affect your insurance premiums. For example, if you lease a Tesla Model 3 for 3 years, your insurance premiums might be around $1,500-2,000 per year, depending on your location and driving habits. But if you buy the same car, your insurance premiums could be higher, around $2,500-3,500 per year.

But what really gets my goat is when insurers try to sneak in extra fees or charges. I mean, come on - if you're leasing an EV, you shouldn't have to pay extra for things like maintenance or wear and tear. That's just not right. And that's why I always recommend shopping around for insurance quotes and reading the fine print carefully. For instance, some insurers might offer a "lease-only" policy that includes maintenance and wear and tear coverage, which could save you around $500-1,000 per year.

And don't even get me started on the so-called "experts" who claim that leasing an EV is always the best option. I mean, that's just not true. Sure, leasing can be a great way to get into a new car every few years, but it's not for everyone. Some people might prefer to buy their cars outright, or they might have specific needs that leasing can't meet. For example, if you drive a lot for work, you might be better off buying a car that can handle high mileage.

What's the Real Question When It Comes to EV Lease vs Buy Insurance?

Can you really afford to lease an EV, or are you better off buying? I mean, it's a tough question, and there's no easy answer. But here's what I do know: if you're considering leasing an EV, you gotta think about the long-term costs. I mean, it's not just about the monthly payments or the overall cost of the vehicle. You gotta think about the insurance premiums, the maintenance costs, and the potential risks. For instance, if you lease a car for 3 years, you might have to pay around $10,000-15,000 in total costs, including insurance and maintenance. But if you buy the same car, you might have to pay around $30,000-40,000 upfront, plus insurance and maintenance costs.

And what about the environmental impact? I mean, think about it - if you're leasing an EV, you're not really reducing your carbon footprint, are you? I mean, the car is still being manufactured, and it's still being driven around. But if you buy an EV, you're making a real commitment to reducing your environmental impact. For example, a study by the Union of Concerned Scientists found that EVs produce less than half the emissions of gasoline-powered cars over their lifetimes.

But here's the thing - not all EVs are created equal when it comes to environmental impact. Some cars, like the Tesla Model 3, have a much lower carbon footprint than others. And that's why it's crucial to do your research before deciding between ev lease vs buy insurance. You gotta look at the data, talk to other owners, and consider the overall cost of ownership. For instance, the Tesla Model 3 has a carbon footprint of around 150-200 grams per mile, while the Nissan Leaf has a carbon footprint of around 200-250 grams per mile.

Let Me Tell You a Story About EV Lease vs Buy Insurance

I knew a guy who leased a BMW iX for 3 years, and he thought he was getting a great deal. I mean, the monthly payments were low, and the car was brand new. But when the lease was up, he got slammed with extra fees and charges. I mean, it was like they were trying to squeeze every last penny out of him. And that's when it hit him - he should have just bought the car outright. I mean, it would have cost him more upfront, but he would have avoided all those extra fees and charges.

And that's why I always recommend buying an EV if you can afford it. I mean, it's not just about the cost - it's about the freedom and flexibility that comes with owning a car. You can drive it as much or as little as you want, and you don't have to worry about extra fees or charges. For example, if you buy a Tesla Model 3, you can drive it for 10 years or more without having to worry about lease restrictions.

But what about the maintenance costs? I mean, EVs are supposed to be low-maintenance, right? Well, it's true - EVs have fewer moving parts than gasoline-powered cars, which means they require less maintenance. But that doesn't mean they're maintenance-free. I mean, you still have to replace the brakes, the tires, and the batteries every so often. For instance, the Tesla Model 3 has a battery warranty of 8 years or 120,000 miles, which is one of the best in the industry.

7 Things You Need to Know About EV Lease vs Buy Insurance

The first thing you need to know is that ev lease vs buy insurance is a complex topic, and there's no one-size-fits-all answer. The second thing you need to know is that resale value plays a huge role in your insurance premiums. The third thing you need to know is that not all EVs are created equal when it comes to resale value. The fourth thing you need to know is that technology can impact resale value. The fifth thing you need to know is that insurers care about resale value too. The sixth thing you need to know is that you gotta think about the long-term costs. The seventh thing you need to know is that buying an EV can be a great option if you can afford it.

And here's a pro tip:

When shopping for insurance quotes, make sure to ask about the insurer's policy on EVs. Some insurers might have specific requirements or restrictions for EVs, so it's crucial to do your research before signing up.

For example, some insurers might require you to install a home charging station or to drive a certain number of miles per year.

And don't forget to consider the overall cost of ownership. I mean, it's not just about the monthly payments or the insurance premiums. You gotta think about the maintenance costs, the fuel costs, and the potential risks. For instance, if you buy a Tesla Model 3, you might have to pay around $30,000-40,000 upfront, plus insurance and maintenance costs. But if you lease the same car, you might have to pay around $10,000-15,000 in total costs, including insurance and maintenance.

What's the Best EV to Lease?

The best EV to lease is probably the Tesla Model 3. I mean, it's a great car, and it holds its value incredibly well. Plus, Tesla has a fantastic leasing program that includes maintenance and wear and tear coverage. For example, if you lease a Tesla Model 3 for 3 years, your monthly payments might be around $500-700, depending on your location and driving habits.

What's the Best EV to Buy?

The best EV to buy is probably the Hyundai Ioniq 5. I mean, it's a great car, and it's priced to sell. Plus, Hyundai has a fantastic warranty program that includes 8 years or 100,000 miles of battery coverage. For instance, if you buy a Hyundai Ioniq 5, you might have to pay around $35,000-45,000 upfront, depending on the trim level and options.

How Much Does EV Insurance Cost?

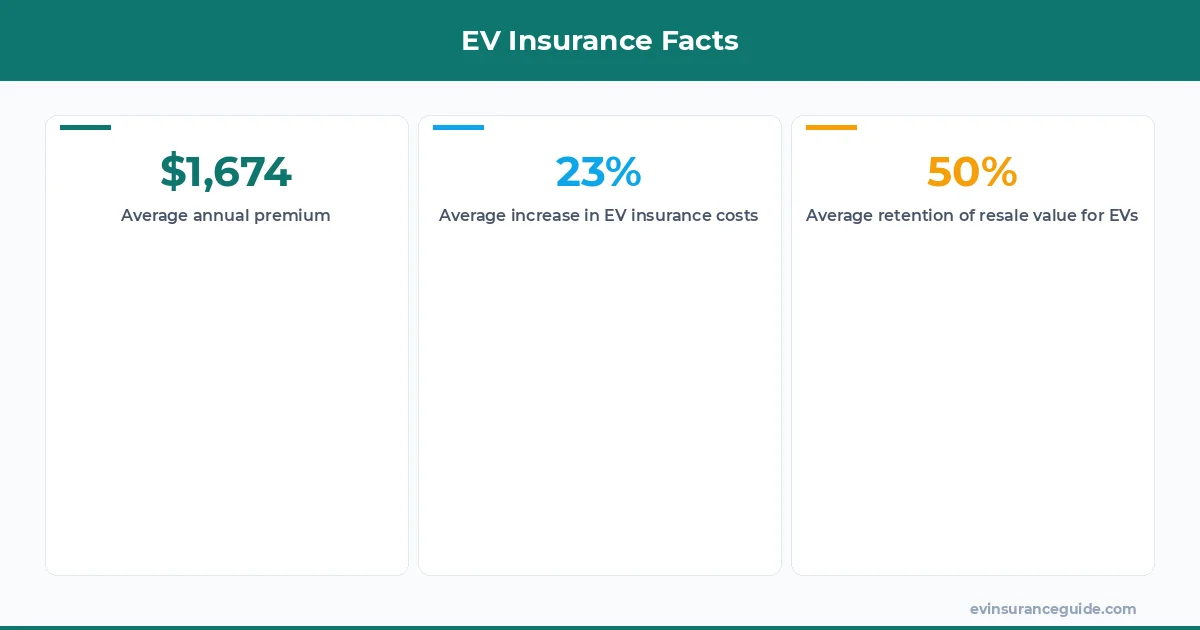

The cost of EV insurance varies depending on the car, the location, and the driving habits. But on average, you can expect to pay around $1,500-3,000 per year for insurance premiums. For example, if you own a Tesla Model 3, your insurance premiums might be around $2,000-3,000 per year, depending on your location and driving habits.

What's the Difference Between EV Lease and EV Buy Insurance?

The main difference between EV lease and EV buy insurance is the level of coverage. I mean, if you lease an EV, you'll typically have a lower level of coverage, since the car is still owned by the lessor. But if you buy an EV, you'll typically have a higher level of coverage, since you own the car outright. For instance, if you lease a Tesla Model 3, you might have a $1,000 deductible, while if you buy the same car, you might have a $500 deductible.

Can I Customize My EV Insurance Policy?

Yes, you can customize your EV insurance policy to fit your needs. I mean, most insurers offer a range of coverage options, from basic liability to comprehensive coverage. For example, if you own a Tesla Model 3, you might be able to add a rider for your home charging station or for your EV-specific accessories.

How Do I Get the Best EV Insurance Quote?

To get the best EV insurance quote, you should shop around and compare rates from different insurers. I mean, it's not just about the price - it's about the level of coverage and the quality of service. For instance, you might want to consider an insurer that specializes in EVs, like Liberty Mutual or USAA.

Go get yourself a better quote. You deserve it.

— Alex