My buddy, Rachel, was paying $2,350 per year for her Tesla Model 3 insurance with Geico. She thought she had a decent deal, but after shopping around, she switched to Progressive and now pays $1,820 per year - that's a $530 savings. What's more, her new policy has better coverage, including a lower deductible and higher liability limits. Wild, right?

WARNING — Don't Get Locked into a Bad Policy

You don't wanna get stuck with an overpriced policy that doesn't offer the coverage you need. For instance, if you own a BMW iX, you might need a policy that covers its advanced tech features, such as adaptive cruise control and lane departure warning. A good policy should also have a reasonable deductible, around $500-$1,000. Anything higher, and you're gonna feel the pinch. Know what the kicker is? Many insurance companies, like State Farm, offer discounts for electric vehicles, so it's worth exploring those options.

That one stung - Rachel had to pay $800 out of pocket for a fender bender because her old policy had a high deductible. Now, she's got a policy that's not only cheaper but also has better coverage. And, with the money she's saving, she can afford to upgrade to a Tesla Model Y. Dead serious, it's worth taking the time to compare policies and find the best one for your EV. For example, a study by the National Association of Insurance Commissioners found that the average annual premium for an electric vehicle is around $1,600. However, this number can vary depending on factors like your location, driving history, and the type of EV you own.

But, and this is a big but, you gotta do your research. Don't just look at the price; consider the coverage, deductible, and any discounts you might be eligible for. For instance, if you're leasing an EV, you might want to look into a policy that offers gap insurance, which can help cover the difference between the actual cash value of the vehicle and the remaining lease balance. And, if you're buying an EV, you might want to consider a policy that offers new car replacement, which can provide you with a brand-new vehicle if yours is totaled.

OK So Here's the Deal With EV Lease vs Buy Insurance

When it comes to EV lease vs buy insurance, there are some key differences to consider. If you're leasing an EV, like a Hyundai Ioniq 5, you'll likely need a policy that meets the requirements of your lease agreement. This might include gap insurance, which can help cover the difference between the actual cash value of the vehicle and the remaining lease balance. On the other hand, if you're buying an EV, like a Rivian R1T, you'll want a policy that reflects the vehicle's value and your personal circumstances. For example, you might want to consider a policy that offers agreed value coverage, which can provide you with a guaranteed payout in the event of a total loss.

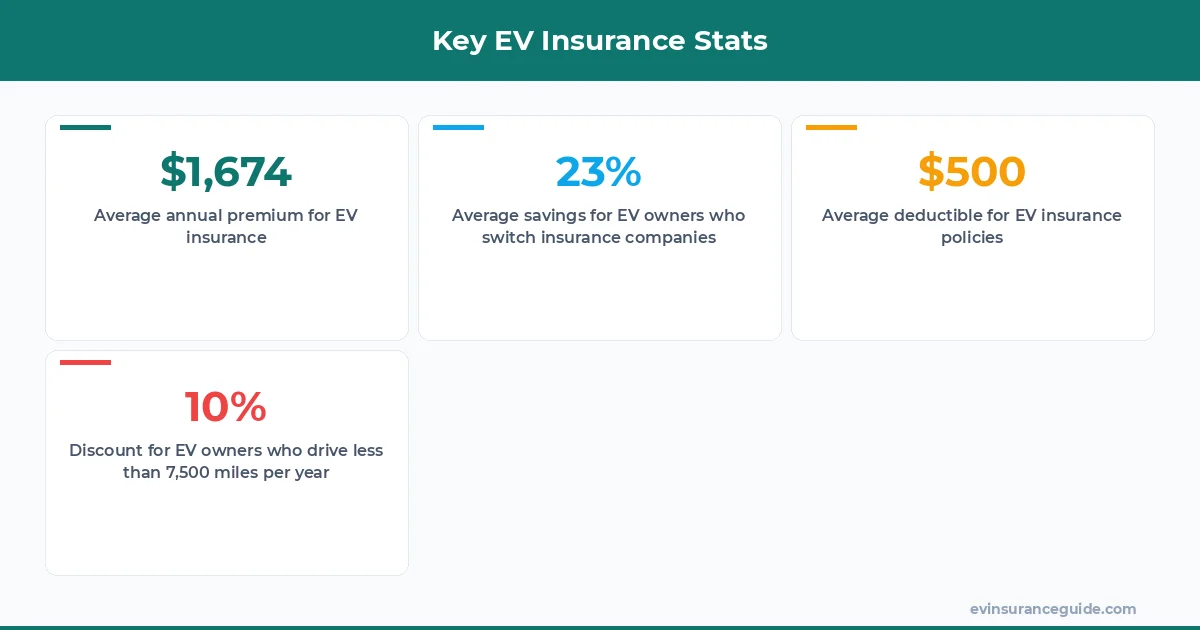

The cost of EV insurance can vary widely, depending on factors like your location, driving history, and the type of EV you own. For instance, a 2022 study by the Insurance Institute for Highway Safety found that the average annual premium for an electric vehicle was around $1,674. However, this number can range from as low as $1,200 to as high as $2,500, depending on your specific circumstances. Sound familiar? It's like buying a new EV - you gotta do your research and compare prices to find the best deal. And, just like buying an EV, you gotta consider the total cost of ownership, including insurance, maintenance, and fuel costs.

Pro tip: When shopping for EV insurance, be sure to ask about discounts for things like low mileage, good grades, or military service. You might be surprised at how much you can save. For example, some insurance companies, like USAA, offer discounts of up to 10% for military personnel.

HONEST_OPINION — Some Insurance Companies Are Better Than Others

Let's be real, some insurance companies are just better than others when it comes to EV insurance. For instance, Tesla's insurance arm is a great option for Tesla owners, offering competitive pricing and specialized coverage for Tesla's unique features. On the other hand, some companies, like Liberty Mutual, might not have the best track record when it comes to EV insurance claims. This policy is overpriced trash, if you ask me. I'd say, if you're driving a Tesla, you should definitely consider Tesla's insurance option - it's like having a policy tailored to your specific vehicle.

But, and this is a big but, you gotta do your research and compare policies from multiple companies. Don't just take my word for it - look at the data, read reviews, and talk to other EV owners. For example, a study by J.D. Power found that Tesla owners who switched to Tesla's insurance arm saw an average savings of $500 per year. And, just like buying an EV, you gotta consider the total cost of ownership, including insurance, maintenance, and fuel costs.

I'm gonna say it - some insurance companies are just not worth the hassle. You don't wanna be stuck with a company that's gonna give you the runaround when you need to file a claim. Know what I mean? It's like dealing with a bad car dealership - you just wanna get outta there. Well, actually, it's worse than that, because you're dealing with your hard-earned cash. So, do your research, read reviews, and choose a company that's gonna treat you right.

COMPARISON — EV Insurance vs Gas-Powered Vehicle Insurance

Now, let's compare EV insurance to gas-powered vehicle insurance. In many ways, they're similar - you gotta consider factors like your driving history, location, and vehicle value. But, there are some key differences. For instance, EVs tend to be more expensive to repair, so you might need a policy with higher coverage limits. On the other hand, EVs also tend to be more efficient and have lower operating costs, which can affect your insurance rates. For example, a study by the National Renewable Energy Laboratory found that EVs can save owners up to $700 per year on fuel costs.

It's like comparing apples and oranges - they're both fruit, but they're different. And, just like fruit, EV insurance and gas-powered vehicle insurance have their own unique characteristics. But, at the end of the day, you just wanna find the best policy for your vehicle, whether it's an EV or a gas-guzzler. Sound familiar? It's like buying a new car - you gotta do your research and compare prices to find the best deal. And, just like buying a car, you gotta consider the total cost of ownership, including insurance, maintenance, and fuel costs.

MYTH_BUST — You Don't Need to Stick with Your Current Insurance Company

There's a common myth that you need to stick with your current insurance company to avoid penalties or higher rates. But, that's just not true. You can switch insurance companies at any time, and you might even find a better deal. For example, if you're currently insured with Allstate, you might find that Progressive offers a better rate for your EV. And, with the money you're saving, you can afford to upgrade to a newer model, like a Tesla Model Y.

It's like breaking up with a bad boyfriend - it's hard, but it's worth it in the end. You don't wanna be stuck with a bad policy that's gonna cost you more in the long run. Know what I mean? It's like being in a bad relationship - you just wanna get outta there. But, with insurance, you gotta do your research and compare policies to find the best one for your EV. And, just like breaking up with a bad boyfriend, you might need to take some time to find the right policy for you.

FAQs

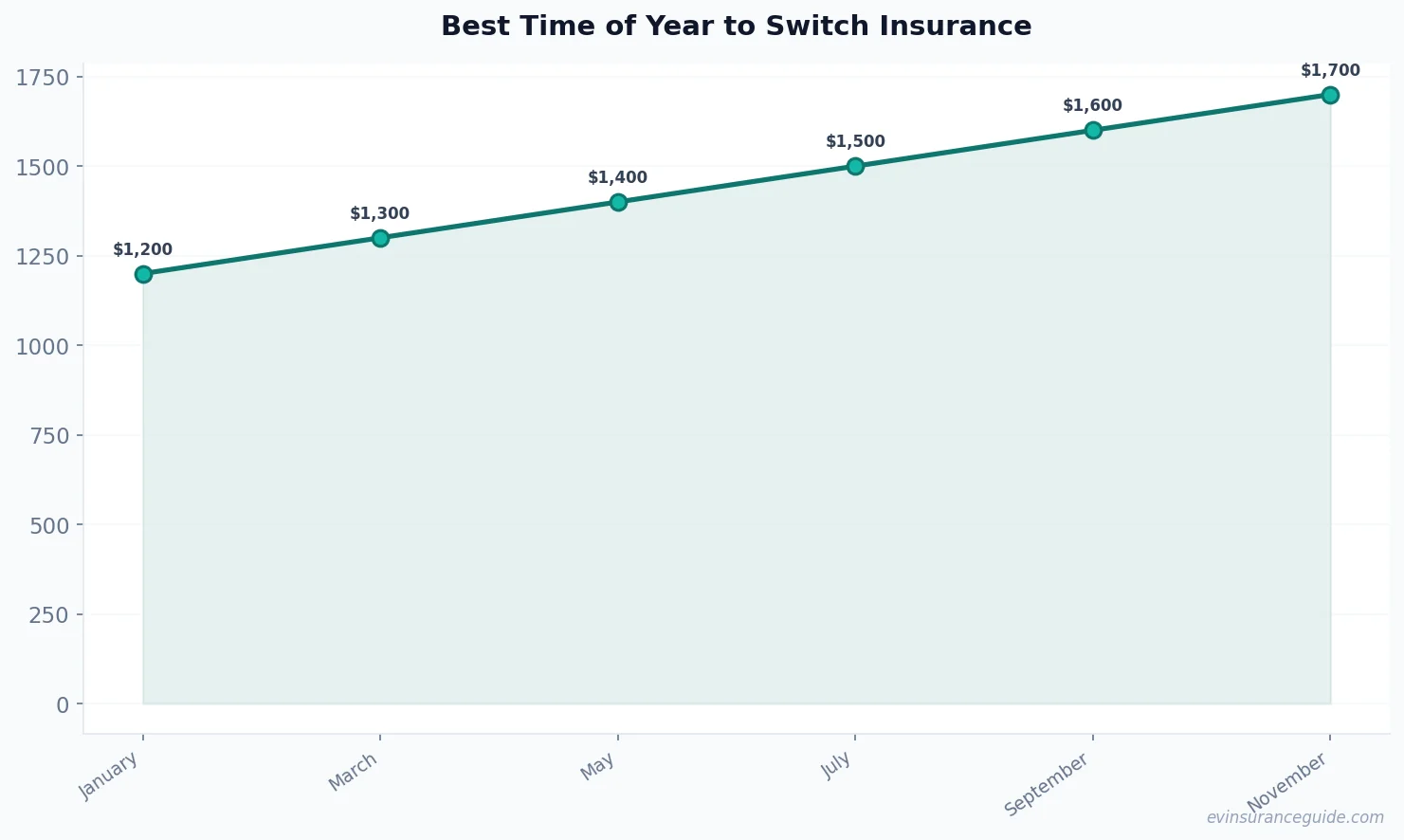

#### What is the best time to switch EV insurance providers?

The best time to switch EV insurance providers is when your policy is up for renewal, or if you've experienced a significant change in your circumstances, such as a move or a new vehicle purchase. For example, if you're moving to a new state, you might find that your current insurance company doesn't offer coverage in that state, so you'll need to switch to a new company.

#### How do I compare EV insurance policies?

To compare EV insurance policies, you should consider factors like coverage, deductible, and price. You should also read reviews and talk to other EV owners to get a sense of which companies offer the best service. For instance, you can check out online reviews on sites like Consumer Reports or J.D. Power to see how different insurance companies stack up.

#### What are the benefits of switching EV insurance providers?

The benefits of switching EV insurance providers include potential cost savings, improved coverage, and better customer service. For example, if you switch to a company that offers a lower deductible, you might save money in the long run if you need to file a claim.

#### Can I switch EV insurance providers at any time?

Yes, you can switch EV insurance providers at any time, but it's usually best to do so when your policy is up for renewal. This can help you avoid any potential penalties or fees associated with switching mid-policy. However, if you've experienced a significant change in your circumstances, such as a move or a new vehicle purchase, it might be worth switching to a new company mid-policy.

#### How do I know if I'm getting the best rate for my EV insurance?

To know if you're getting the best rate for your EV insurance, you should shop around and compare quotes from multiple companies. You should also consider factors like your driving history, location, and vehicle value to ensure you're getting a fair rate. For example, you can use online tools like insurance comparison websites to get quotes from multiple companies and compare them side by side.

#### What are some common mistakes to avoid when switching EV insurance providers?

Some common mistakes to avoid when switching EV insurance providers include not comparing policies carefully, not reading reviews, and not considering all the factors that affect your rate. For instance, you might miss out on discounts or other benefits if you don't take the time to carefully compare policies.

That's all from me — go save some money. — Alex